Bob Moriarty, founder of 321gold, is not one to be shy about what he thinks. In this month’s conversation Bob lays out why he thinks global equity indices are on the verge of rolling over after reaching a bullish sentiment extreme. We also delve into the Miramont mess of a couple weeks ago and why he is still a shareholder despite being very unhappy with Miramont CEO Bill Pincus. Bob also delves into why many self-proclaimed gurus make investment information and analysis more complicated than it needs to be. Without further ado here is Energy & Gold’s April 2019 conversation with Bob Moriarty…

Goldfinger: A lot has happened since the last time we spoke. Gold has dipped about $50, palladium dropped about $200, meanwhile the stock market has continued cruising higher and the S&P 500 is now at its highest levels since last October. In your estimation what is the most interesting thing happening out there right now?

Bob Moriarty: We are at an extreme of emotion right now in global stock markets. Sentiment has once again become overheated and I expect that a large decline will begin in the next few weeks. I also expect gold to rise as stock market indexes fall.

Goldfinger: There sure are a lot of bulls out there suddenly and the Barron’s cover story (“This Bull Market Has No Expiration Date”) over the weekend helped to illustrate just how optimistic market participants seem to have become. Can sentiment get even more extreme?

Bob Moriarty: That’s a really good question and one that I should cover. I wrote a piece on January 26th, 2018 where I pointed out that nearly a dozen commodities and stock indexes (including the S&P 500) had reached an extreme of emotions and were about to turn lower. In fact, they began to turn that day and entered into a sharp correction that lasted for a couple of weeks. On December 24th of 2018 I wrote another piece titled “Sentiment Says Turn, Turn, Turn” and I think there were 9 different futures markets that I talked about including the S&P 500, T-Bonds, crude oil, and gasoline. The Daily Sentiment Index (DSI) for all of the markets mentioned in the article had reached extremes in the prior week and on the 24th things were ready for a big turn. Markets were closed on the 25th for Christmas Day but when they reopened on the 26th we saw major bottoms in the S&P, copper, crude oil, etc.

As of Friday’s close the sentiment (DSI) for the S&P and Nasdaq is at 91 and the DSI for the Nikkei is 93. Now those are not turning points but they’re very high readings that tells me a turning point is coming shortly. If the DSI for the S&P or Nasdaq hit 95 shortly I would say “ok, this is it. Time to sell!” – if you’re a contrarian you probably want to see a big rise in stocks this week that will create a sentiment extreme which will likely be followed by a sharp correction or even a crash.

Why is Trump telling the Fed to lower interest rates? First of all it’s not the business of the President to do that and he’s an idiot economically so I don’t know why anyone would listen to him. If Powell listens to him it will be the spark that will ignite gold.

Goldfinger: It seems absurd to me that Trump is trying to appoint guys like Stephen Moore to the Federal Reserve, who wants to cut the Fed Funds Rate 50 basis points even as the unemployment rate is below 4% and the stock market is near all-time highs. Seems like a great recipe for creating high inflation and an even bigger stock market bubble.

Bob Moriarty: We have this giant dichotomy between what is really happening in the economy to the little guy and with all these economic indicators and the stock market. The working guy is struggling to make his car payments (7 million americans are 90 days or more late on their car payments) while the stock market keeps going higher.

Donald Trump is not an economist, he was handed his fortune by his father, and although he is the President of the United States he should not be the one making decisions on interest rates and monetary policy.

Goldfinger: So you’re thinking there’s going to be a big stock market downturn, a crash, in 2019? Will this be as severe as 2008?

Bob Moriarty: It will be more severe. We had two corrections in 2018, one at the beginning of the year and one at the end of the year. What we’ve gotten since December is a dead-cat bounce and I expect that the bounce is about to come to an end.

Goldfinger: Won’t the Fed just come in and save everything by cutting rates further and reimplementing QE?

Bob Moriarty: They didn’t even save it last time. They had a corpse and they pumped a bunch of helium into it to try to reinflate a body. At some point that corpse is going to pop from all the gas that’s been pumped into it.

Goldfinger: In December Powell reaffirmed that the Fed was going to stay the course with quantitative-tightening (QT) and rate hikes, then two weeks later Powell made a U-turn and said the Fed was going to pause rate hikes and would consider ending its balance sheet normalization (QT) program before year end. The Fed Funds Futures market is now pricing in a 75% chance of a rate cut by January 2020 in yet another sign that the Fed is more likely to ease than it is to tighten further.

Bob Moriarty: The scary part is that the Fed and Trump are likely to get whipsawed by the stock market and the stock market is only one part of the entire global financial system. If they cut rates they’re about to pull the pin on a nuclear hand grenade and that’s a really bad idea.

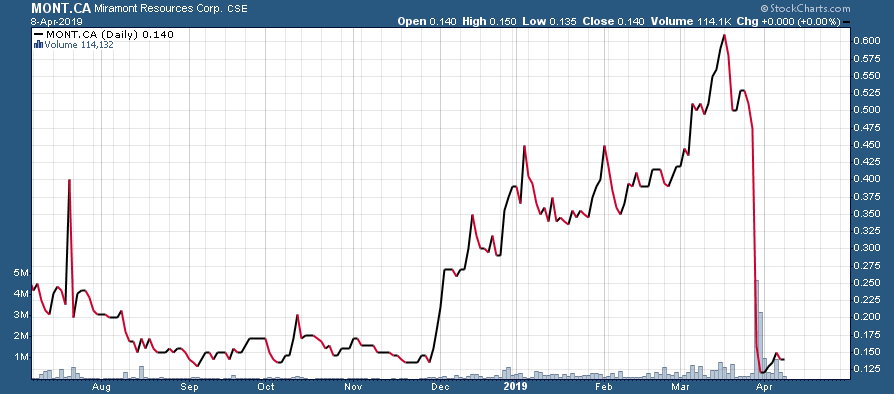

Goldfinger: Turning to the junior mining sector I want to talk about Miramont and that whole fiasco. We spoke about Miramont several times in the last six months and you were pretty clear that it was a drill play that you thought had a good shot of hitting. You even compared it to a lottery ticket that would have three drawings (3 sets of 3 holes each to be released). It’s also important to note that junior exploration companies rarely hit the discovery hole in the first ten holes, in some cases it could take more than 100 holes to drill the money hole. In greenfields exploration the odds of success are pretty low, and the odds of hitting a big hole on the first few holes of a drilling program are even lower.

What happened with Miramont and why were you so upset with CEO Bill Pincus?

Bob Moriarty: First of all, I was a major investor in Miramont. It was not something I was casually involved in. I had a couple of dozen phone calls with Bill Pincus and I had at least a dozen phone calls discussing what they were doing in the drill program and how it would progress. They had 3 separate targets areas and they were going to put 3 holes in each one. They were sending off 3 holes at a time to the assay lab and then they were going to report those holes 2-3 weeks later in sets of 3 holes at a time.

Now it’s always important when i’m writing about a company that I know exactly what to expect so readers can make their mind up. You’re absolutely correct that in a greenfields drilling program failure is the norm. Sometimes it can take more a hundred drill holes before you hit a monster drill hole. So the idea that you’re going to go out and hit a big one in the first few holes into a new target is pretty ridiculous. However, this was not a greenfields project. Greenfields projects are like Aurania poking into Ecuador or Irving drilling a sinter that’s never been drilled before. The odds of those guys hitting on the first hole or any hole isn’t very high.

Miramont’s project is a brownfields project because this project is in the shadow of the head-frame of a former gold mine in the diatreme. There are also hundreds of surface samples showing good grades. The odds are significantly higher drilling in the shadow of a head frame than they are with a greenfields project.

My problem is with the way the results were released. I was telling investors that they had 9 lottery tickets in their hands (3 targets x 3 drill holes per target) and there was going to be 3 different lottery drawings. Now we don’t expect every lottery ticket to be a winner but we need to actually have the lottery drawing to know if we have a winner or not. Now let’s presume that the first 3 holes were terrible, that happens all the time! Sure the stock would have gone down but it wouldn’t have gone down 77% in one day. But Bill Pincus sat on those results for three weeks and waited until the second set of results had come in to announce it. Even worse, in the NR on March 28th he didn’t say a word about those first 3 holes so he just ignored the first 3 holes and announced the 2nd set of 3 holes. The 2nd set of holes were dismal, they weren’t absolutely terrible but they were dismal. Shareholders looked down at their tickets and said “Wait a minute! This lottery drawing was 3 weeks ago and my tickets are no good.”

MONT.CA (Daily)

How you release drill results is very important. Garibaldi is an example of this. I would challenge anyone to go to Garibaldi’s website and tell me what the drill results are. Every 3 or 4 months they will cherry pick a hole and it will look very good. But in reality you have no idea what they’re discovering, or if they’re discovering anything at all.

It’s very important to release drill results in a way that investors can understand and know exactly what you’re doing. Miramont didn’t do that and in hindsight it was a pretty sad drill program that was very poorly announced. However, with that being said Miramont still has C$3.5 million in the bank and they still have a pretty good project. The market cap is C$7.5 million so the company is being valued at about C$4 million when you subtract the cash, that’s pretty cheap. The stock probably isn’t going to move much until they do something of significance and that could take 6-9 months.

Goldfinger: Good explanation Bob. Isn’t this a fairly normal thing in the junior mining sector? There is a constant desire to want to impress and please the market and Miramont’s market cap was up to about C$30 million before the dismal results were announced. The CEO knew if he put out those first 3 holes his stock would get cut in half in all likelihood so my guess is that he waited so he had a chance to hit in the next set of holes.

In my experience a lot of junior mining companies do this. I’m not going to name names but I can think of a handful of companies who probably did something similar in the last year. I’ve seen a lot of companies batch holes together and hold up releasing assays until they had a better hole to announce. It’s a common thing in the sector isn’t it Bob?

Bob Moriarty: Yes it is, and it’s still fraud. If the first three holes were announced and didn’t hit, it means the investors still had six lottery tickets. The stock probably would have gone down but 20-25%, not 77%. Investors could have gotten pissed off and sold or they could hold the remaining tickets or they could buy more of what is now a cheaper company. The real key is that investors could make their own decisions. When management chose to sit on three bad holes and dump six bad holes on the market, management made the decision, not the investor and that just isn’t right. If it’s not fraud, it’s pretty foolish.

Goldfinger: Is it really? Is it a violation of securities law in Canada to withhold results that don’t materially change a company’s prospects?

Bob Moriarty: It’s fraud because it changes who has control of the decision making process. If a company doesn’t give its shareholders the full story then it is lying by omission. I’ve got this old fashioned belief that the people who own shares in a company are the owners of the company. They are the ones taking the risk and they should be the ones making the decision to buy or sell based upon the most accurate information available.

Now I can give you twenty examples of companies that had drill programs and six months later we were still waiting for drill results. You know it only takes 2-3 weeks to get assays back from the lab so you realize that the company must be waiting for a better hole before reporting assays. It’s fraud.

Goldfinger: I think this is a very interesting topic and one that should probably be addressed in more detail. I know for a fact that junior mining companies hold results all the time in the hopes of better results coming in the future. I also think it is very difficult to manage market expectations for drill results and a junior simply cannot expect to please the market with every single NR they release.

Bob Moriarty: The biggest mistake that Bill Pincus made was telling me one thing (how he would release 3 holes at a time) and then doing something completely different. I would encourage that if anyone wants me to work with their company don’t lie to me. I don’t like lying.

Goldfinger: The timing of assays and the release of assays is one of the more frustrating aspects of the junior mining sector. Too often companies will give guidance as to the timing of assay results and that timeline won’t even be close to what actually ends up happening. I have been very frustrated with companies that say one thing and then a month later switch to a completely different story. I have learned that when assays are taking the slow boat it’s a bad sign 99% of the time. Good results seem to come out even faster than expected and bad results tend to end up being released 2-3 months after the company initially said they would reported.

Bob Moriarty: There’s a saying “Good news travels on a jet plane and bad news travels on a mule train.”

Goldfinger: (laughs) Exactly!

Bob Moriarty: Look, i’m the most negative guy in the junior mining sector. The standard in this industry is failure. Most companies are going to fail. 50% of the companies in this sector are lifestyle companies, they could drill into the Fed gold vault in New York City and they wouldn’t report the results because the last thing they want is shareholders making any money out of it. Many junior mining companies are scams or close to it. That’s why it’s important for investors to figure out whether management is going to shoot straight with you. If they are going to shoot straight with you then you should probably invest, if they’re not then you know what to do.

Before investing in a junior mining company it’s important to answer this question: “Is the management of this company running the company for shareholders or for themselves?” You should want to invest in companies that are being run for shareholders.

Goldfinger: Are you still a shareholder in Miramont?

Bob Moriarty: I am a shareholder still but only because there are some shares in a private placement at C$.35 that don’t start free trading for another month. I would need to see something substantial from management in the next month for me to stay a shareholder but I don’t think there’s going to be any major movement in the share price aside from the fact that it’s simply gotten so damn cheap. I think drilling is another 6-9 months away at the earliest so it could take some time to turn this ship around.

Goldfinger: Irving Resources and Novo got hit shortly after Miramont dropped and this was probably some collateral damage from the Miramont mess. Both have since stabilized. Do you see this as a buying opportunity in Irving as I know they are currently drilling? Also, do you have any thoughts on Japan Gold which is another Japan focused gold explorer, except that it has about ⅓ the market cap?

Bob Moriarty: Irving and Novo both have excellent management teams that are running the companies for shareholders. I bought some more Irving after it dropped last week and it is now my largest position.

There was a lot of discussion on the chat board about Japan Gold and Irving both being in Japan. As of Friday JG’s partner on 5 of its projects backed out of a deal. I think it’s important to understand what a management of a company is running the company for and I think if you look at management compensation of Japan Gold relative to Irving Resources I think you’ll find your answers.

Goldfinger: Interesting that you say that because it seems to me that Japan Gold is an interesting trade here after the First Quantum news (discontinuing the option on 5 lithocap projects that Japan Gold has). They are cashed up and all set to drill beginning in May. JG has two drill programs including one target that is on trend with Hishikari (one of the world’s largest and highest grade gold mines). Goldcorp (soon to be Newmont) is Japan Gold’s partner on the 12 gold projects and Newmont has stated publicly that Japan is a jurisdiction they are very interested in. I bought some Japan Gold shares last week and I think it has a decent chance of revisiting recent highs in the high $.30s as drilling begins. I think Irving is also very interesting and I will follow their drill results with great interest over the coming months. I think that any drilling success by either Irving or Japan Gold will be good for both stocks and help to draw more investor interest towards Japan as a mining jurisdiction.

Bob Moriarty: Let me point something out to you. 1 out of 20 juniors will explode higher on drill results or some other news. Now you’ve got to look for the subtle differences sometimes and that usually has to do with the location and the management team. I like my chances with Keith Barron and Aurania (TSX-V:ARU) and I like my chances with Irving and its management team including Chairman Quinton Hennigh. ARU and IRV are putting a lot of money into drilling and exploration, as opposed to into the pockets of management. This is very important because a dollar that goes into management’s pockets is a dollar that is not going to go into the ground with drilling.

Goldfinger: If the standard in the sector is failure then why should anyone be involved in the junior mining sector?

Bob Moriarty: I’m going to refer you to my latest book “Basic Resource Investing: The Idiot’s Guide”. When the winds are high enough even turkeys fly. I believe we are about to go into a cycle where we will see this play out, everything precious metals and resource related is going to fly. Strangely enough the highest percentage returns will be on the $.04 and $.05 stocks, some of which are probably going to be the biggest pile of garbage stocks out there.

Goldfinger: What you’re saying is despite the fact that the majority of junior mining companies aren’t going to be successful over the long run, there is still plenty of opportunity to profit from market volatility in the short term.

Bob Moriarty: If a stock goes from $.04 to $.20 in a couple of months you shouldn’t care if it generates value for investors in the long run, you’ve got a 400% gain in the short term! If you can pick stocks up when they’re cheap and sell them when you’ve got a nice profit there is plenty of volatility in the junior mining sector to profit from. Everyone is looking for 10-baggers but those only happen once in a great while. Doubles and triples happen all the time and if you don’t sell when you’ve got a profit then the only alternative is to sell at a loss.

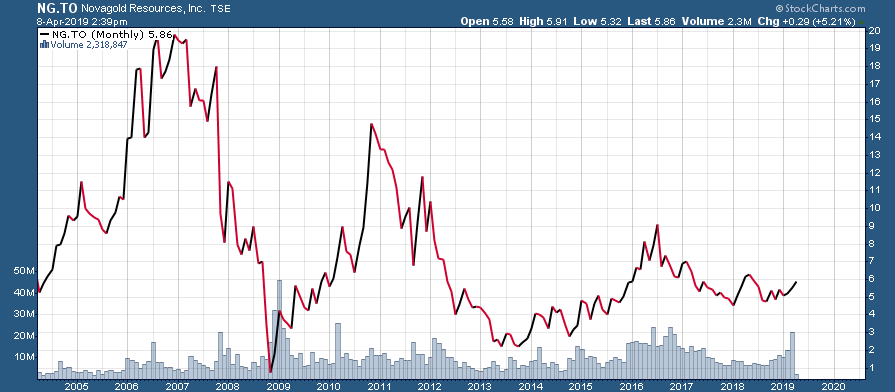

Goldfinger: That’s an important point Bob. If you were to only buy and hold you’re probably not going to do great over the long run in the junior mining sector, unless of course you have impeccable timing like buying in January 2016. However, if you are willing to be nimble and lock in some gains on double and triples you should be able to do quite well in this sector. I remember that long term Novagold chart from your book, I think it’s a great example of the insane swings that we often see in junior mining stocks.

NG.TO (Monthly)

Bob Moriarty: That’s exactly right. Let me give you another example of a stock that I bet you haven’t heard of before. The symbol is USGD and it trades on the CSE. It’s called American Pacific Mining and it went from C$.04 three and a half months ago to C$.31 last Friday. These things happen all the time! They haven’t done anything remarkable, they simply got rid of all the weak hands and suddenly the stock is up almost 700%. If people were to look for 30%-50% gains, which is exceptional, they can get that in junior mining stocks all the time. But they have to buy cheap and sell at a profit and believe it or not, it’s hard to get people to do that.

Goldfinger: Is USGD an advertiser? Is this the company that optioned a project from Novo?

Bob Moriarty: Yes they are an advertiser, and they got the Tuscarora project in Nevada near the Carlin Trend from Novo.

Goldfinger: I’ve actually heard of it, a couple of people mentioned USGD to me last week which is what usually happens after a stock has a big move; people come to me when stocks are up 400% and ask me if they should buy it.

Bob Moriarty: See you just made my point! How many people mentioned USGD to you when it was four cents?

Goldfinger: Nobody.

Bob Moriarty: Exactly. Then as soon as it goes up 700% everybody’s talking about it. I keep telling people to stop listening to gurus and stop worrying about minor technical things. If it’s cheap buy it.

Goldfinger: That reminds me of something Bob. Did you read my post last week on the Yukon featuring Alexco Resources, Banyan Gold, and Victoria Gold?

Bob Moriarty: I saw it but didn’t read it.

Goldfinger: Ok, i’m going to give you a homework assignment to read it but i’ll tell you the basics right now. Banyan Gold (TSX-V:BYN) is trading at C$.045 with a C$4.7 million market cap, and it has a project called Aurex-McQuesten that is right near Alexco’s Keno Hill Project and Victoria Gold’s Eagle Gold Project that are both set to be in production by the end of the year. Banyan also has a project with a 524,000 ounce 43-101 compliant gold resource that is open in all directions for expansion. In my estimation both projects should be worth a lot more than the market is currently valuing them at. (Author is long Banyan Gold in a long term portfolio at time of publishing)

Bob Moriarty: You’ve already given me the information that I need. What did you say Banyan’s market cap is?

Goldfinger: C$4.7 million.

Bob Moriarty: They’re cheap! Everybody wants to make it more complicated than it needs to be. Every guy who wants to charge money for information wants to make things more complicated than it needs to be so they can introduce voodoo. There is no voodoo. A four and a half cent stock is cheap and who knows maybe it will go up when gold breaks out.

Goldfinger: As always, thank you for your time and insights Bob. I think this was a very interesting conversation and I found the topic of assay releases to be of particular interest. It’s time that CEOs in this sector start shooting straight with shareholders a lot more than they have.

Disclaimer

The article is for informational purposes only and is neither a solicitation for the purchase of securities nor an offer of securities. Readers of the article are expressly cautioned to seek the advice of a registered investment advisor and other professional advisors, as applicable, regarding the appropriateness of investing in any securities or any investment strategies, including those discussed above. Banyan Gold Corp. is a high-risk venture stock and not suitable for most investors. Consult Banyan Gold Corp’s SEDAR profile for important risk disclosures.

EnergyandGold has been compensated to cover Banyan Gold Corp. and so some information may be biased. EnergyandGold.com, EnergyandGold Publishing LTD, its writers and principals are not registered investment advisors and advice you to do your own due diligence with a licensed investment advisor prior to making any investment decisions.

This article contains certain forward-looking information and forward-looking statements within the meaning of applicable securities legislation (collectively “forward-looking statements”). Certain information contained herein constitutes “forward-looking information” under Canadian securities legislation. Generally, forward-looking information can be identified by the use of forward-looking terminology such as “expects”, “believes”, “aims to”, “plans to” or “intends to” or variations of such words and phrases or statements that certain actions, events or results “will” occur. Forward-looking statements are based on the opinions and estimates of management as of the date such statements are made and they are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed by such forward-looking statements or forward-looking information, standard transaction risks; impact of the transaction on the parties; and risks relating to financings; regulatory approvals; foreign country operations and volatile share prices. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Actual results may differ materially from those currently anticipated in such statements. The views expressed in this publication and on the EnergyandGold website do not necessarily reflect the views of Energy and Gold Publishing LTD, publisher of EnergyandGold.com. Accordingly, readers should not place undue reliance on forward-looking statements and forward looking information. The Company does not undertake to update any forward-looking statements or forward-looking information that are incorporated by reference herein, except as required by applicable securities laws. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SEDAR.com for important risk disclosures. It’s your money and your responsibility.