“Build your new house out of copper bricks , cover that copper with gypsum wallboard so you forget it’s in the walls. Ten years from now you’ll be able to tear down that house and buy a fleet of electric Lamborghinis with your profits.” ~ Robert Friedland

Billionaire resource investor and copper mega-bull, Robert Friedland

“Almost all signals indicate a tightening market: low Exchange inventory & bonded stocks, treatment charges at lows, etc. Spring to bring a fresh demand boost that the supply side is ill-positioned to meet, generating upside risk for price.” ~ Morgan Stanley

“We are seeing some outright growth in developed market metals consumption in the construction, consumer appliances, and automotive sectors, as covid-19 drives home renovations and new home demand,” ~ Citi Commodities Research

Bank of America forecasts global copper consumption to rise 6% to 24.76 million tonnes in 2021, and Citi sees new home demand and home renovations driving higher copper demand in the US in the next couple years. Citi also sees the copper market shifting into a deficit in the 2nd half of 2021, followed by deficits in 2022 and 2023.

Bullish on copper yet?

If that’s not enough for you, have a listen to a recent conversation with billionaire resource investor Robert Friedland

Simply stated, decarbonization is bullish for metals. Copper goes through the eye of the decarbonization process and based on McKinsey & Co. estimates, global electricity consumption will double by 2050, led by the electrification of transport and buildings.

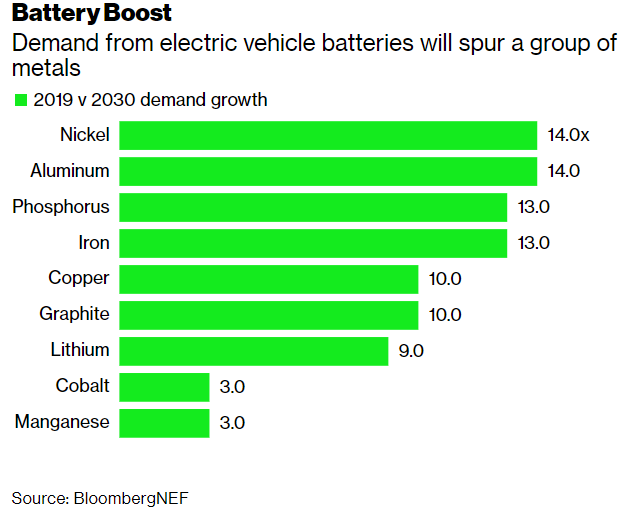

Copper will also benefit from a 10x increase in demand from electric vehicle batteries:

Generating electricity from renewable sources in an extremely copper intensive exercise; renewable energy systems use up to five times more copper than traditional power generation. This is because copper is an excellent thermal and electrical conductor, power systems that utilize copper generate and transmit energy with high efficiency and with minimal environmental impacts.

The bullish case for copper is compelling and multi-faceted:

-

Electric vehicle boom.

-

A post-covid global economic recovery.

-

Infrastructure programs being initiated around the globe.

-

Increasing new home starts and home renovations in the US.

-

Surging copper demand in China; data center, cloud computing, infrastructure etc.

-

Structural deficit globally underpinned by strong demand (emerging markets, electrification of power grid, etc.) and a mine depletion problem; two new copper mega-mines (Oyu Tolgoi Underground and Kamoa-Kakula) will only serve to balance out falling production at legacy copper mines.

The future is bright for copper, and it’s not much of a stretch to expect a new all-time (above US$4.65/lb) for copper at some point in the next year. Judging by past copper bull markets, the current one could still be in its early stages:

Now you’re probably wondering, how does one position themselves to benefit from the copper bull market?

Now you’re probably wondering, how does one position themselves to benefit from the copper bull market?

Trading copper futures or storing copper rods in one’s backyard are probably not a very practical route for most people. This leaves copper mining stocks as the simplest investment vehicles that can also provide substantial torque to the copper bull market. A 25% rally in copper could easily result in 200%+ rallies in many copper exploration and development stocks. In addition, copper producers like Freeport-McMoran (NYSE:FCX) and Southern Copper (NYSE:SCCO) are becoming cash cows spitting out massive free cash flow, that can be returned to shareholders via dividends and share buybacks.

I have scoured the copper investing landscape and selected five companies that I believe offer attractive risk/reward propositions to investors with a 12-24 month investment time horizon. I have selected one producer, one soon to be producer, one developer that should be in production fairly soon, and two explorers/developers that could offer substantial upside torque as the copper bull achieves new highs and these companies advance their projects and generate positive drill results. The world is going to need new copper mines coming into production 5-10 years from now and all of the companies I have selected have the potential to help meet the world’s growing copper appetite over the next couple of decades.

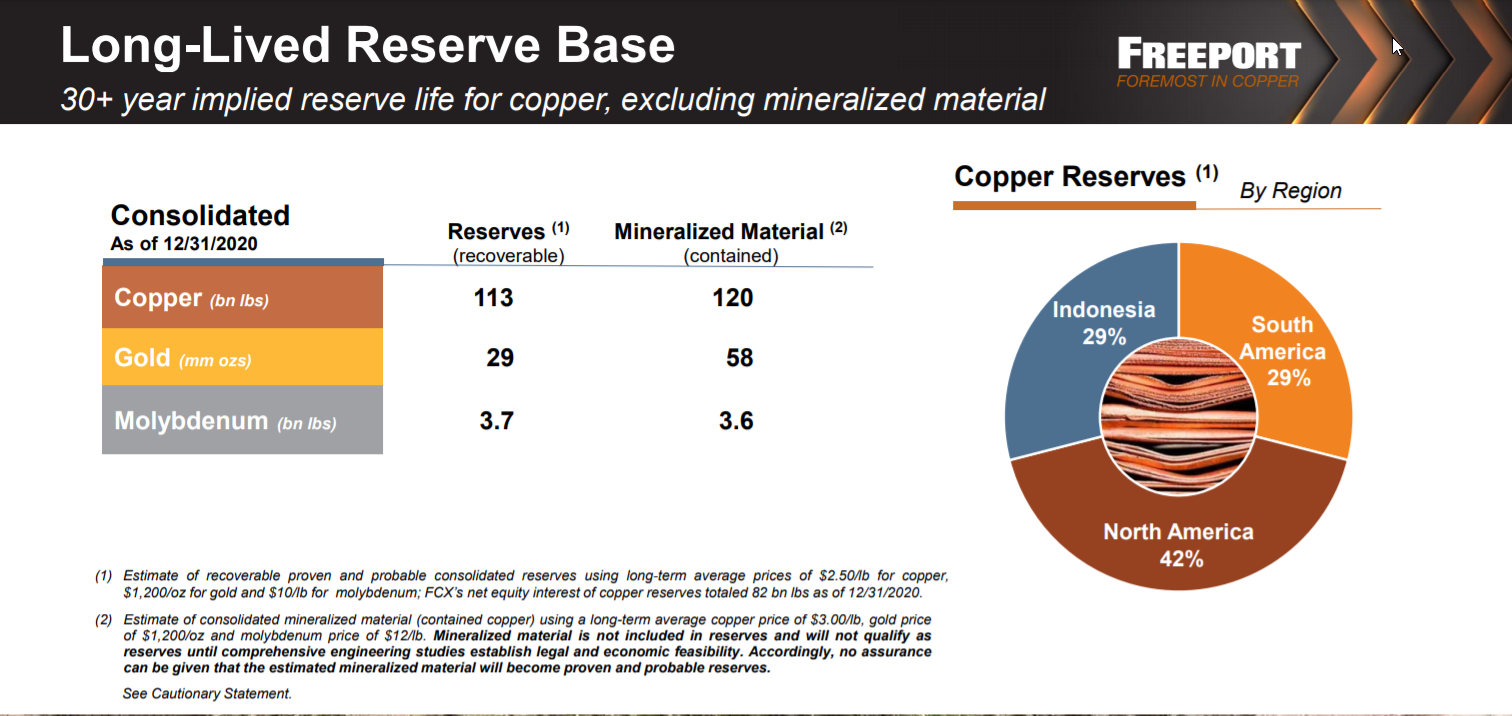

The first company is copper giant Freeport McMoran (NYSE:FCX), FCX is the majority owner and operator of the behemoth Grasberg Copper/Gold Mine in Indonesia. Grasberg produces roughly 1.5 billion pounds of copper and 1.6 million ounces of gold per year. In addition to Grasberg, FCX has an impressive portfolio of producing mines across the Americas including El Abra in Chile, and Lone Star in Arizona. FCX is set to generate US$8 billion of EBITDA using a US$3.50/lb copper price in 2021, however, the company also boasts a strong pipeline of development projects and brownfields exploration potential.

Many investors think of Grasberg when Freeport is mentioned, however, this is a company with a substantial reserves base across a diverse portfolio of assets in multiple mining jurisdictions:

FCX probably isn’t going to be a multi-bagger from its current US$45 billion market cap, however, it can definitely deliver 30%-50% upside for shareholders over the next 12-24 months. FCX also pays a $.30 per share dividend (.96% annual rate that is paid quarterly) dividend that I expect will be increased (potentially doubled) later this year.

Our second copper pick is Robert Friedland’s Ivanhoe Mines (TSX:IVN). Ivanhoe is the 39.6% owner of the high-grade Kamoa-Kakula Mine in the Democratic Republic of the Congo (DRC). Kamoa-Kakula is the largest undeveloped high-grade copper discovery in the world with an average grade of 2.74% copper and a massive resource hosting nearly 38 million tonnes of contained copper.

Some may immediately raise eyebrows over the jurisdictional risk of the DRC. However, it is worth noting that Ivanhoe’s JV partners at Kamoa-Kakula are Chinese national mining company Zijin Mining (39.6%) and the government of the DRC (20%). Kamoa-Kakula stands to put the DRC back on the map as an investable jurisdiction. In addition, Kamoa-Kakula will provide high pay jobs and significant employment opportunities through the economy in the DRC. Kamoa-Kakula will also be environmentally friendly; A 2020 independent audit of Kamoa-Kakula’s greenhouse gas intensity metrics performed by Hatch Ltd. of Mississauga, Canada, confirmed that the project will be among the world’s lowest greenhouse gas emitters per unit of copper produced.

Phase 1 copper production from the Kakula Mine is scheduled to begin in July 2021. Kakula is projected to be the world’s highest-grade major copper mine, with an initial mining rate of 3.8 million tonnes per annum at an estimated average feed grade of more than 6.0% copper at first, ramping up to 7.6 million tonnes per annum in Q3 2020. Phases 1 and 2 combined are forecast to produce approximately 400,000 tonnes of copper per year. Based on independent benchmarking, the project’s phased expansion scenario to 19 million tonnes per annum would position Kamoa-Kakula as the world’s second largest copper mining complex, with peak annual copper production of more than 800,000 tonnes.

Kamoa-Kakula is the centerpiece of the Ivanhoe story, however, IVN also boasts a large exploration license area called “Western Foreland” directly to the west of Kamoa-Kakula. Western Foreland has already delivered an impressive discovery at Makoko with impressive drill intercepts such as 7.44 meters (true width) of 7.81% copper at a 2.0% copper cut-off.

Ivanhoe’s 64% owned Platreefs palladium/platinum/rhodium/nickel/copper/gold project in South Africa is another key asset in Ivanhoe’s portfolio. Platreefs recently delivered an updated feasibility study which evaluates a 4.4-million-tonne-per-annum (Mtpa) underground mine with annual production of more than 500,000 ounces of palladium, platinum, rhodium and gold; plus more than 35 million pounds of nickel and copper. This feasibility study also shows an after-tax NPV8% of US$3.7 billion and IRR of 28% at spot metal prices; with a cash cost of US$442 per ounce of palladium, platinum, rhodium and gold, net of by-products and including sustaining capital.

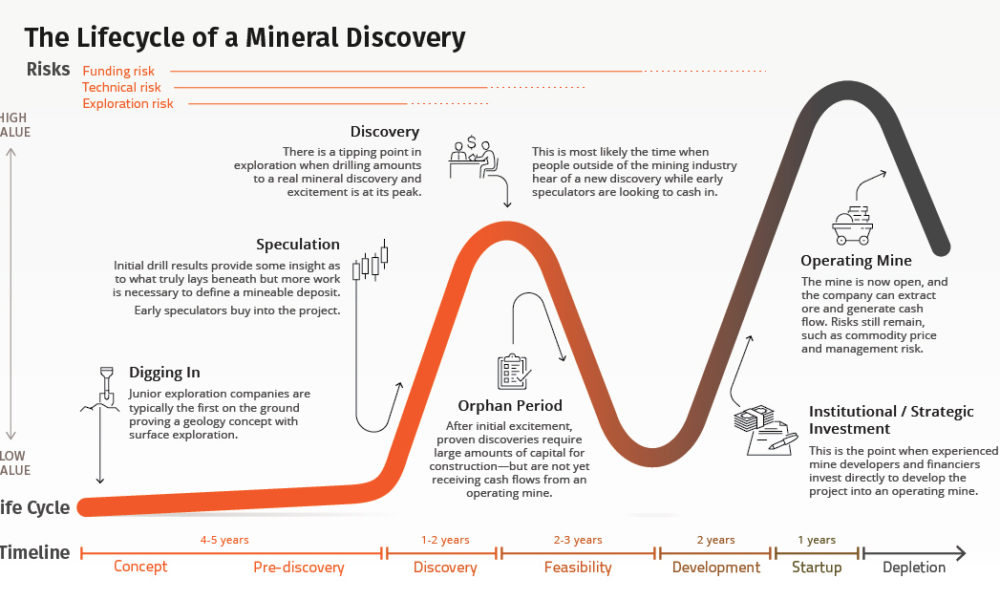

Ivanhoe is at the sweet spot in the mining life cycle according to the Lassonde Curve and with a smooth ramp up of mining operations at Kamoa-Kakula it wouldn’t be a stretch to see IVN shares double over the next 12-24 months.

Our third copper pick is a company that is just beginning to ramp up copper production at its Gunnison Copper Project in Arizona. Excelsior Mining (TSX:MIN, OTC:EXMGF) is steadily ramping up copper production after announcing the sale of 90,000 pounds of copper cathode in January. Excelsior anticipates achieving the nameplate production rate of 25 million pounds per annum later this year. Similar to Ivanhoe, Excelsior is positioned in the sweet spot of the Lassonde Curve.

Our third copper pick is a company that is just beginning to ramp up copper production at its Gunnison Copper Project in Arizona. Excelsior Mining (TSX:MIN, OTC:EXMGF) is steadily ramping up copper production after announcing the sale of 90,000 pounds of copper cathode in January. Excelsior anticipates achieving the nameplate production rate of 25 million pounds per annum later this year. Similar to Ivanhoe, Excelsior is positioned in the sweet spot of the Lassonde Curve.

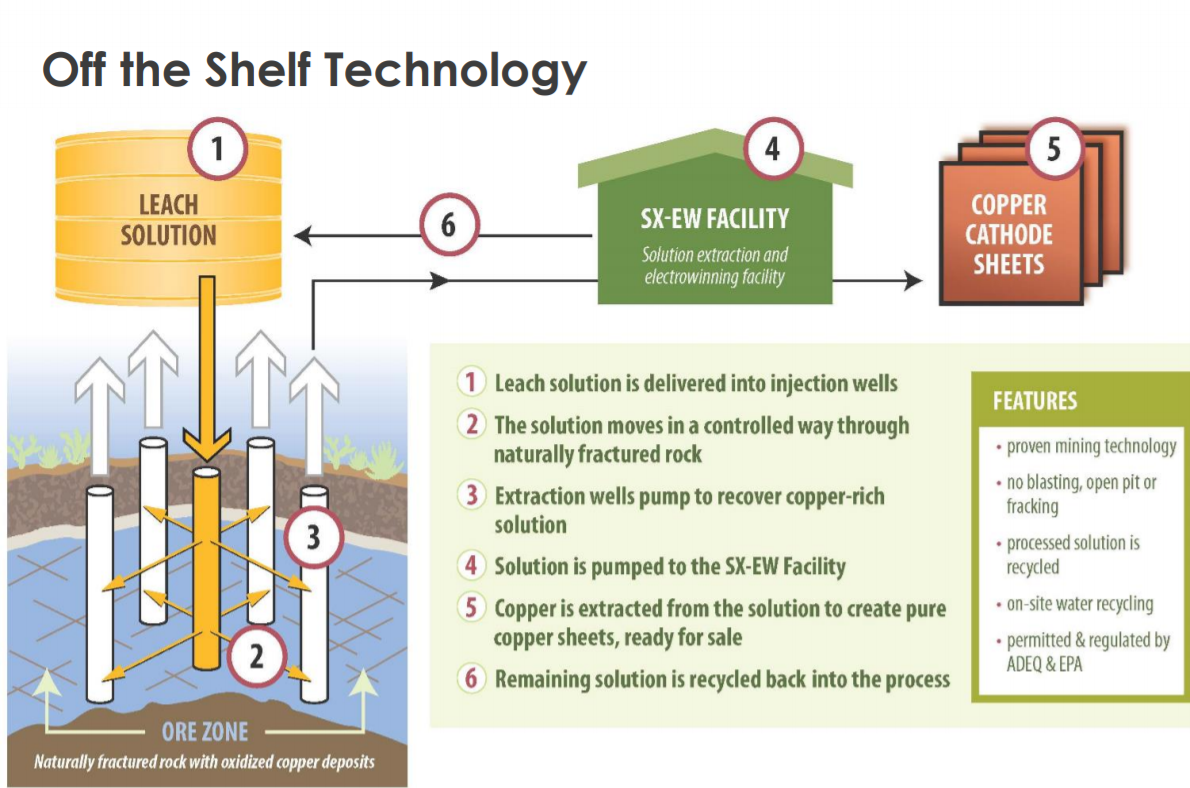

Excelsior is America’s newest copper producer and Gunnison has the unique title of being the world’s most environmentally friendly copper project. This is due to the fact that Gunnison utilizes an ISR mining method (in-situ recovery), which means that there is no heavy equipment, no blasting or fracking, and no underground tunneling required. At Gunnison, leach solution (acid) is delivered into injection wells and the solution moves in a controlled way through naturally fractured rock. Extraction wells then pump to recover a copper-rich solution:

This copper-rich solution is pumped to the SX-EW facility (solution extraction and electrowinning facility) and copper is extracted from the solution to create pure copper sheets. The remaining solution is recycled back into the process.

A final feasibility study completed in 2017 showed a US$807 million net present value (NPV) for Gunnison using a 7.5% discount rate and a US$2.75/lb copper price. At today’s US$3.89 copper price the NPV is well over US$1.5 billion. Meanwhile, Excelsior’s current market cap is less than US$200 million.

This gap between Excelsior’s potential future value and its current value has a lot to do with last year essentially being a write-off year for the company. Covid certainly made everything more challenging, however, Excelsior also decided to take many months in order to complete a wellfield optimization to improve efficiency for long-term production performance.

The Gunnison Project is currently in the early days of ramping-up copper production, which is expected to achieve the rate of 25 million pounds per annum later this year as the first phase of a multi-staged development plan. Gunnison will eventually be expanded to achieve a production rate of 125 million pounds per year – this will occur in year 4 or 5 of a 24 year mine life.

Later this year, once the entire wellfield is active at Gunnison and copper cathode production accelerates, I expect Excelsior shares to quickly see an upward revaluation to C$1.50+.

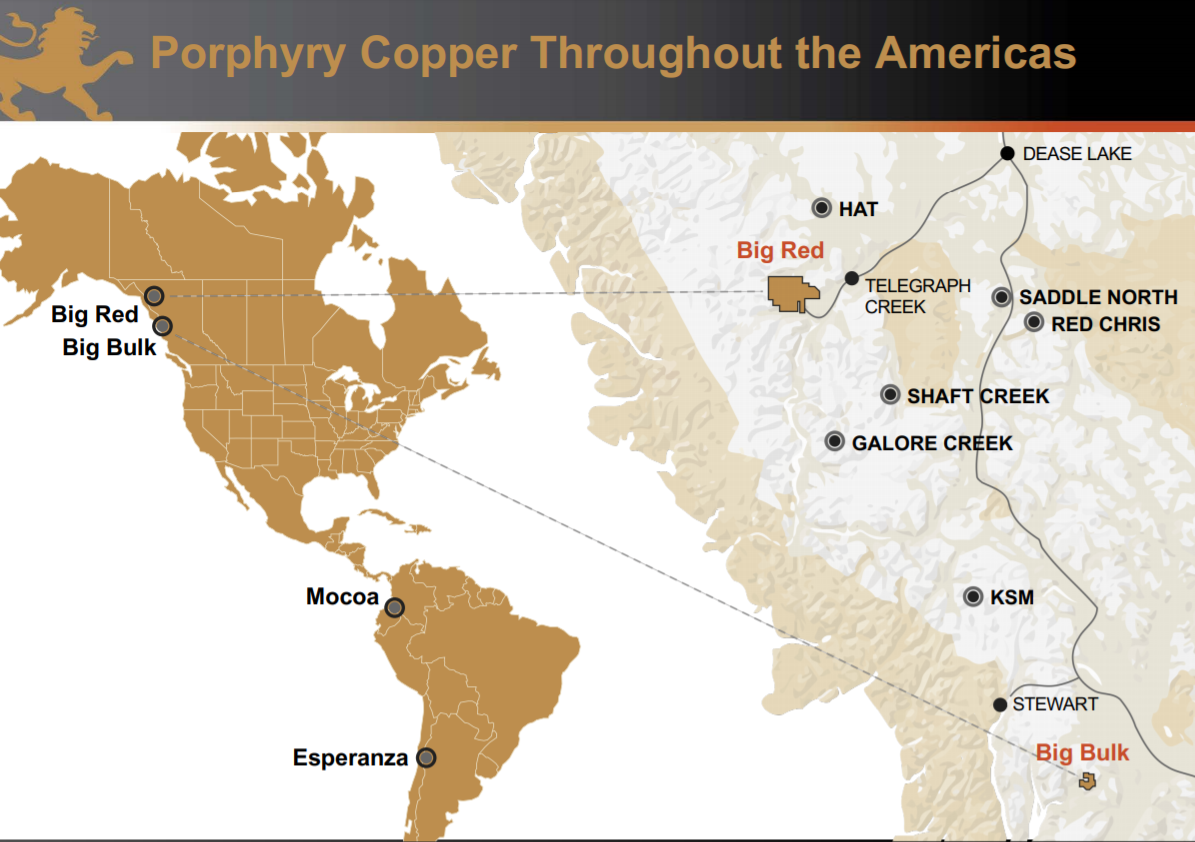

Our fourth copper pick is an explorer/developer with four projects at different stages located across the Americas. Libero Copper & Gold (TSX-V:LBC, OTC:LBCMF) has two exploration stage projects located in the Golden Triangle of British Columbia, Canada and two more advanced stage projects located in South America (Mocoa in Colombia and Esperanza in Argentina). The company has just raised C$7 million in order to prepare for a busy year of drilling that will include 5,000 meters at Esperanza and 7,000+ meters at Big Bulk and Big Red in the Golden Triangle.

Mocoa is Libero’s most advanced project; mocoa has a pit constrained resource that contains 636 million tonnes of 0.45% copper equivalent at a cut-off of 0.25% copper equivalent containing 4.6 billion pounds of copper and 511 million pounds of molybdenum. Libero is planning on drilling Mocoa later this year to expand mineralization along strike and at depth. Previous drilling included 0.67% copper equivalent over 634 meters and 0.59% copper equivalent over 779 meters ending in high grade mineralization beneath the current resource. Regional copper anomalies will also be drilled for the first time as porphyries typically occur in groups. Mocoa is in the Jurassic porphyry belt which also holds the Mirador mine and Solaris’ Waritza deposit. Solaris Resources (TSX: SLS) has reached a C$700 million market cap based on similar drill results to Mocoa.

Esperanza, in San Juan, Argentina is Libero’s first order of business this year. Surface work is starting immediately followed by 5,000 meters of drilling commencing in April focused on the large 2.0-kilometer by 1.2-kilometer surface alteration footprint and stepping-out from the discovery hole that intercepted 387 meters of 0.78% copper equivalent from surface through the end of hole.

Libero will commence surface mapping, sampling and IP surveying at Big Red beginning in June. This will be followed by 5,000 meters of drilling following up the 2020 greenfield porphyry discovery on the periphery of a greater than one kilometer in diameter porphyry footprint.

Libero will commence surface mapping, sampling and IP surveying at Big Red beginning in June. This will be followed by 5,000 meters of drilling following up the 2020 greenfield porphyry discovery on the periphery of a greater than one kilometer in diameter porphyry footprint.

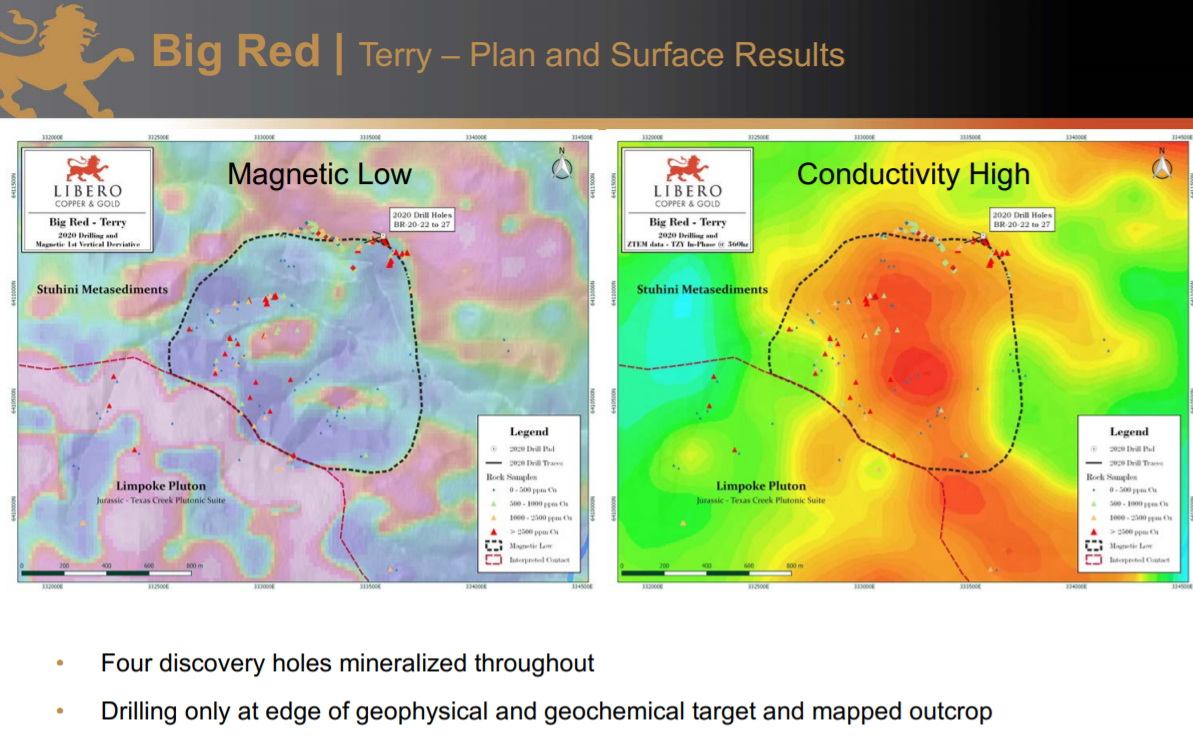

Big Red is a new greenfield porphyry copper discovery that was made in 2020 with five drill holes that were mineralized from surface to the end of the holes at the Terry Target. Highlight intersections include 70.1 meters grading .41% copper, including 12.19 meters at 1.02% copper AND 80.77 meters grading .36% copper, including 13.72 meters at .71% copper.

The reverse circulation drill that was used in the 2020 drill program at Big Red had limited depth capabilities. Phase 2 drilling at Big Red in summer 2021 will utilize diamond drilling to test the depth extent. Drilling will also step out from the 2020 drilling which was on the periphery of a greater than one kilometer in diameter porphyry footprint including high-grade copper and gold surface rock samples and potassic alteration within a magnetic low and conductivity high.

GT Gold’s Saddle North deposit and Newcrest’s Red Chris mine share a similar geological setting to Terry with average copper grades comparable to the initial drill results at Terry.

GT Gold’s Saddle North deposit and Newcrest’s Red Chris mine share a similar geological setting to Terry with average copper grades comparable to the initial drill results at Terry.

Libero offers shareholders multiple ways to win, including year round news flow at four different projects across three jurisdictions in North and South America. At a post-financing market cap of roughly US$20 million with C$7.5 million in the company treasury, Libero offers an attractive bet on the copper bull market with ample potential for new discoveries that could deliver big upside to those who buy LBC.V at today’s prices.

Our fifth and final copper pick is definitely the riskiest, but it also probably has the most potential upside due to its low valuation. Bitterroot Resources (TSX-V:BTT, OTC: BITTF) is in the midst of a phase two drill program at its LM Project in Michigan’s Upper Peninsula.

Bitterroot Resources Ltd.(51%) and its privately held partner Below Exploration Inc. (49%) are exploring the LM Property for high-grade nickel-copper-platinum-palladium deposits similar to Lundin Mining’s Eagle and Eagle East mines in the Upper Peninsula of Michigan.

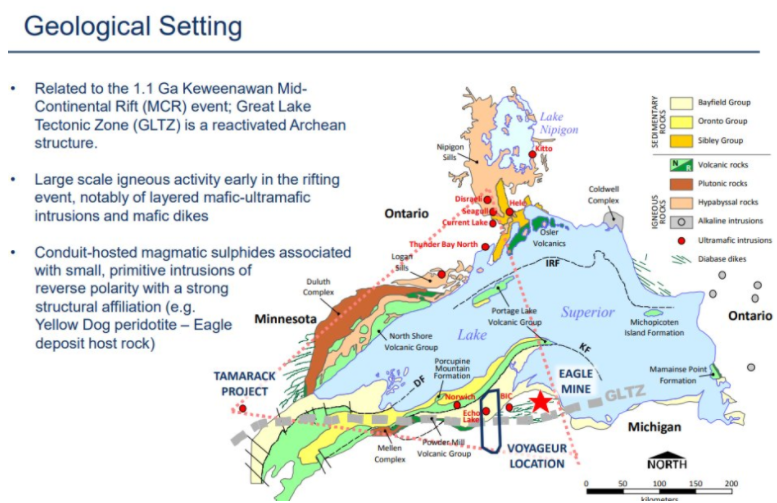

The upper peninsula of Michigan is part of the Canadian Shield, bisected by the “mid-continent rift”. Miners have known for a while that this area had the potential for high-grade, conduit-hosted copper/nickel deposits and Rio Tinto was able to prove this theory with the discovery of the Eagle Mine (now owned and operated by Lundin Mining) and the Tamarack deposit in Minnesota (now a JV with Talon Metals Corp.).

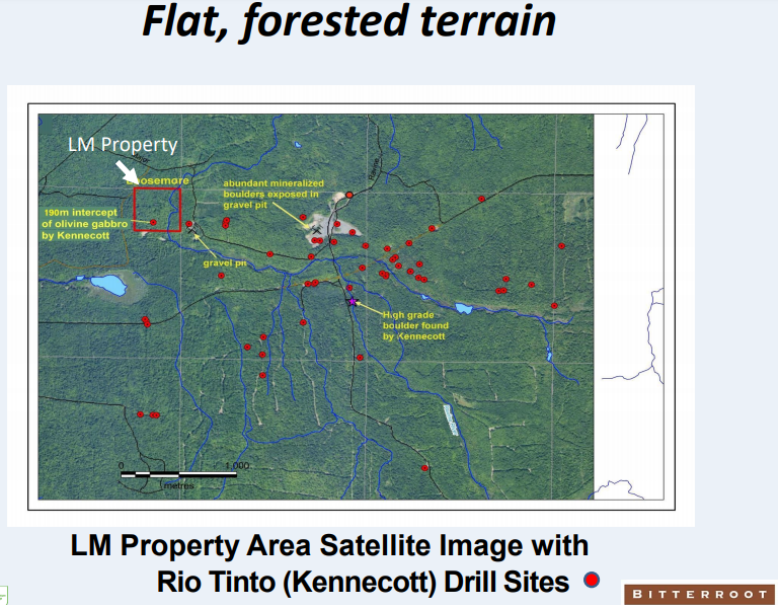

In the late 90s and early 2000s, Rio Tinto’s US subsidiary Kennecott Exploration carried out significant exploration in this area of the Upper Peninsula. LM is located within a mile of a gravel pit with nickel-copper sulfide-bearing olivine gabbro boulders. In 1995, Kennecott intercepted 190 meters of olivine gabbro in its first and only drill hole at LM, but never followed up on the hole due to budget cuts in the late 1990’s. Another junior explorer leased the property from 2003-2014, but did not do any drilling.

In the late 90s and early 2000s, Rio Tinto’s US subsidiary Kennecott Exploration carried out significant exploration in this area of the Upper Peninsula. LM is located within a mile of a gravel pit with nickel-copper sulfide-bearing olivine gabbro boulders. In 1995, Kennecott intercepted 190 meters of olivine gabbro in its first and only drill hole at LM, but never followed up on the hole due to budget cuts in the late 1990’s. Another junior explorer leased the property from 2003-2014, but did not do any drilling.

Bitterroot acquired the LM lease in 2014, in part, because a former Kennecott exploration manager for the region thought that LM was the most compelling untested target in a very prospective area.

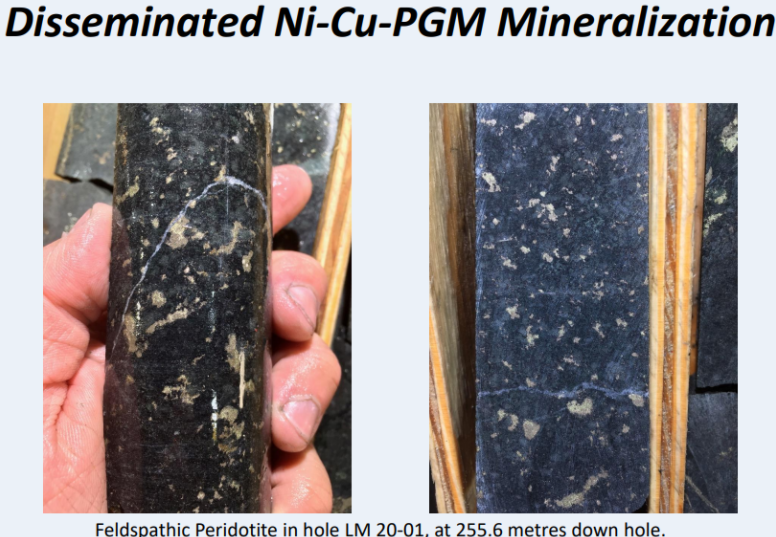

Gabbroic intrusions in this area are prospective for nickel, copper, cobalt, platinum, and palladium in massive sulfides. At Lundin Mining’s Eagle Mine and elsewhere in the Mid-Continent Rift region, disseminated sulfides occur around bodies of massive and semi-massive sulphide mineralization. In Bitterroot’s maiden drill program at LM, the company intersected a highly encouraging section of mafic/ultramafic rock with disseminated blebs of chalcopyrite, pentlandite and pyrrhotite. These are the same types of mafic/ultramafic rocks that host Eagle and Eagle East.

Hole LM20-01 intersected a 5.3 meter interval (4.8 meters estimated true thickness) of mafic/ultramafic rock with disseminated blebs of chalcopyrite, pentlandite and pyrrhotite. This interval grades 0.62% copper, 0.58% nickel and 0.327 grams Au+Pd+Pt/tonne. This is the kind of ‘sniff’ of disseminated sulfides in just the right geological setting that could be characteristic of a much larger deposit of semi-massive and/or massive sulfides.

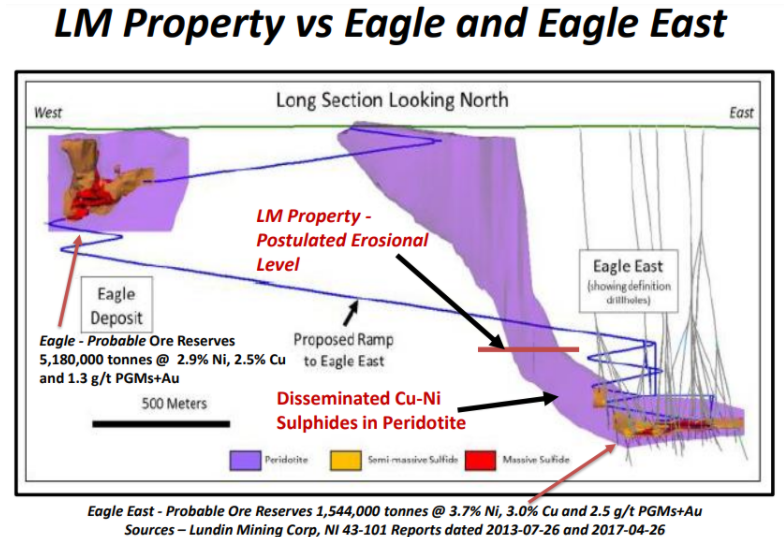

At Eagle and Eagle East disseminated copper-nickel sulfides in peridotite (host rock) occur around massive sulfides that grade as high as 5% copper, 5% nickel, and 3-4 g/t PGMs:

It is particularly intriguing that the metal tenor of the disseminated sulfides intersected in hole LM20-01 indicates that massive (100%) sulfides would grade much higher; roughly 7% nickel, 8% copper, and 3-4 g/t PGMs.

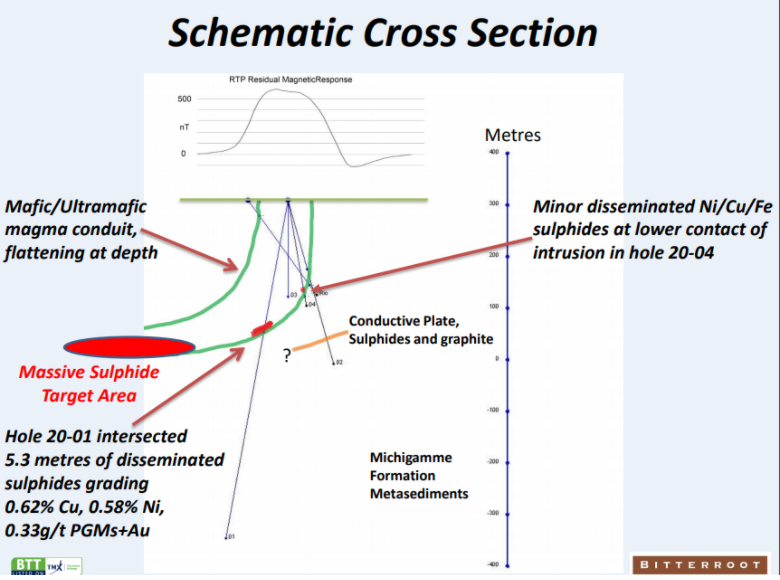

In the summer of 2020 Bitterroot drilled 4 holes totaling roughly 1,400 meters of diamond drilling. Although one of the four holes hit good grades, the other holes were important because they allowed BTT to get a much better grasp of the apparent geometry of the magma conduit. BTT now has a lot more confidence as to the shape and geometry of the gabbroic intrusion, basal mafic-ultramafic unit and the conduit that contains it.

As can be seen above the conduit appears to be flattening out at a moderate depth (less than 300 meters). This is quite significant if confirmed by the phase 2 drilling which is now underway at LM. Conduit hosted massive sulfides are typically found at the base of the conduit, or where the shape of the conduit allowed sulfides dropping out of solution to pool together.

BTT’s phase 2 drill program at LM is underway as of two weeks ago, so they are likely on hole #2 now (~300 meter holes at a drill rate of 40-50 meters per day). The phase 2 drill program will attempt to follow the mineralized zone intersected in hole LM20-01 down-plunge. The phase 2 program at LM will encompass 6-8 diamond drill holes for a total of roughly 2,400 meters.

There couldn’t be a better location, OR a better time to make a new base metals discovery in the United States. The Upper Peninsula of Michigan is an area that already has active operating mines and a favorable history of mining and mineral exploration. In addition, the incoming Biden administration has made it very clear that it will support battery metals mining in the US. Metals such as cobalt, copper, and nickel are of vital strategic interest to the future of the United States and the growth of the electric vehicle industry. Moreover, billionaire mining financier Robert Friedland recently stated that he is actively looking to invest in battery metals projects in the United States where “we can get a social license to mine”. Bitterroot’s LM Project could be the perfect project at the perfect time and the market has only just begun to take notice.

I own all five companies mentioned in this article. You should judge which ones you prefer based upon your risk tolerance, time frame etc. However, diversifying your risk by picking up a basket of all five is probably a good idea too. FCX being the least risky could receive the highest weighting, while Libero and Bitterroot are the riskiest and thus probably deserve the lowest dollar allocation.

Disclosure: Author owns shares of some of the companies mentioned in this article at the time of publishing and may choose to buy or sell at any time without notice.

Disclaimer

The article is for informational purposes only and is neither a solicitation for the purchase of securities nor an offer of securities. Readers of the article are expressly cautioned to seek the advice of a registered investment advisor and other professional advisors, as applicable, regarding the appropriateness of investing in any securities or any investment strategies, including those discussed above. Libero Copper & Gold Corp. is a high-risk venture stock and not suitable for most investors. Consult Libero Copper & Gold Corp’s SEDAR profiles for important risk disclosures.

EnergyandGold has been compensated to cover Libero Copper & Gold Corp. and so some information may be biased. EnergyandGold.com, EnergyandGold Publishing LTD, its writers and principals are not registered investment advisors and advice you to do your own due diligence with a licensed investment advisor prior to making any investment decisions.

This article contains certain forward-looking information and forward-looking statements within the meaning of applicable securities legislation (collectively “forward-looking statements”). Certain information contained herein constitutes “forward-looking information” under Canadian securities legislation. Generally, forward-looking information can be identified by the use of forward-looking terminology such as “expects”, “believes”, “aims to”, “plans to” or “intends to” or variations of such words and phrases or statements that certain actions, events or results “will” occur. Forward-looking statements are based on the opinions and estimates of management as of the date such statements are made and they are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed by such forward-looking statements or forward-looking information, standard transaction risks; impact of the transaction on the parties; and risks relating to financings; regulatory approvals; foreign country operations and volatile share prices. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Actual results may differ materially from those currently anticipated in such statements. The views expressed in this publication and on the EnergyandGold website do not necessarily reflect the views of Energy and Gold Publishing LTD, publisher of EnergyandGold.com. Accordingly, readers should not place undue reliance on forward-looking statements and forward looking information. The Company does not undertake to update any forward-looking statements or forward-looking information that are incorporated by reference herein, except as required by applicable securities laws. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SEDAR.com for important risk disclosures. It’s your money and your responsibility.