While equities have more than tripled from the 2009 bottom and home prices have also tacked on significant gains (doubled in certain parts of the country) there is a valid case to be made that these asset classes are still relatively cheap by historical standards:

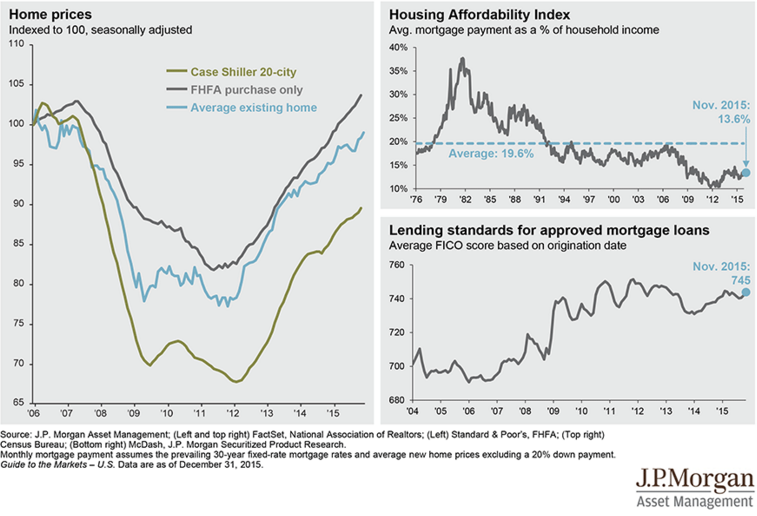

The average mortgage payment as a % of household income remains well below the historical average and lending standards are about as stringent as they’ve ever been.

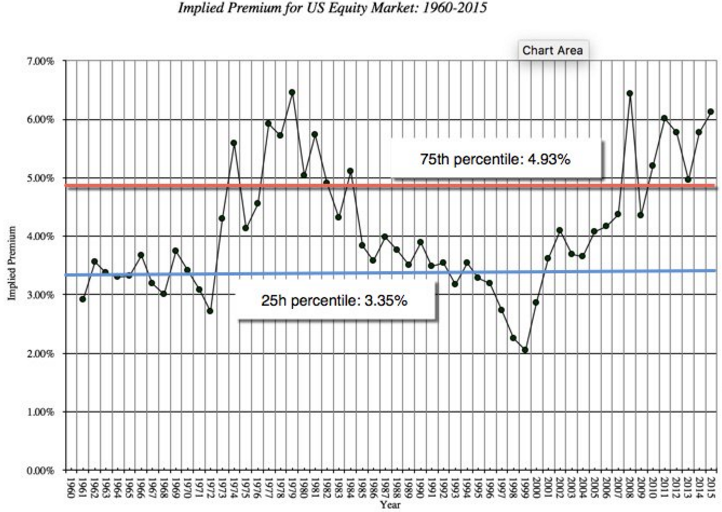

Meanwhile, the equity risk premium (a higher risk premium means that equities are cheaper relative to ‘risk-free’ assets such as the US 10-year Treasury Note) is exceptionally high (above 6%):

The key input in both housing affordability and the equity risk premium is the US 10-year Treasury Note yield. Historically low Treasury yields make housing more affordable (by affecting the 30-year fixed mortgage rate) and also make equities appear to be relatively cheap. Both of these could turn out to be a passing illusion when and if long-term interest rates begin to adjust upward. Right now there are very few people who believe that long bond yields will rise appreciably in 2016 (many market participants foresee a flattening yield curve with short term bond yields rise while long term bond yields remain the same or actually decline).

Regardless of what actually transpires with bond prices/yields it’s clearer than ever that if one knows the directions of interest rates they hold the key to the direction of many other financial asset prices. Moreover, it is for this reason that the Fed will be extraordinarily careful in raising short term rates.