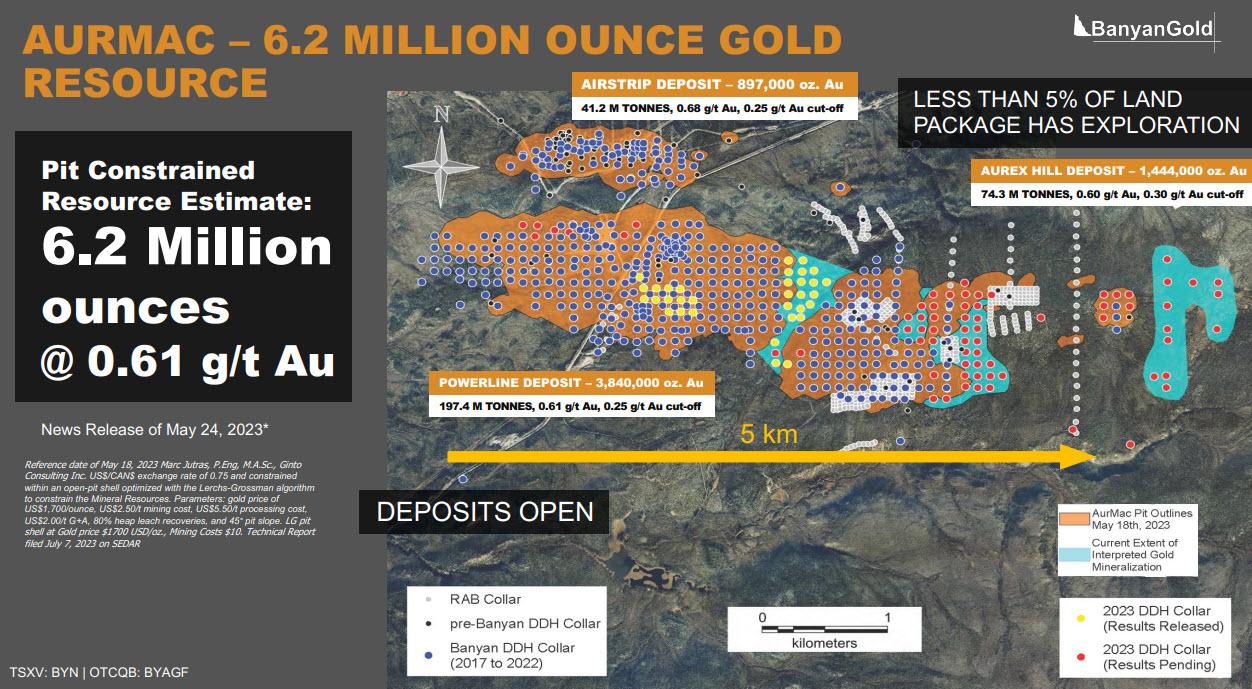

Banyan Gold (TSX-V:BYN, OTC:BYAGF) has had a busy year that includes publishing an updated mineral resource for its flagship AurMac Project in the Mayo Mining Area of the Yukon. The updated resource totals 6.2 million ounces of gold on the near-surface, road accessible AurMac Property. In addition, Banyan completed a 25,000 meter drill program and continues to build out its project development team. The additions of Kai Woloshyn (20 years of experiencing in environmental and permitting consulting) and Brad Thrall (metallurgical engineer with 35 years of experience in mine development operations) demonstrate that Banyan is very serious about advancing and further de-risking AurMac.

At last week’s New Orleans Investment Conference I had the opportunity to sit down with Banyan Gold CEO Tara Christie for a corporate update. Tara was as confident and focused as ever on delivering shareholder value.

Goldfinger:

Tara, it’s good to see you. We are at the New Orleans Investment Conference, I think this is where we first met. I believe it was at the 2017 conference. Feels like a long time ago, a lot has happened in the last six years.

Tara Christie:

A lot.

Goldfinger:

This year, you published a resource update that was how large?

Tara Christie:

6.2 million ounces.

Goldfinger:

6.2 million ounces. That’s a big accomplishment. I think of all the companies here, I would guess that Banyan has the biggest gold resource.

Tara Christie:

Yes, except for Victoria Gold. But they are a producer.

Goldfinger:

I think we can state that Banyan has made tremendous progress in a short period of time. However, as always, in the market, it’s, “What have you done for me lately?” We’re in another moment where we can’t sit on our laurels, it’s, “What’s next?” What’s next for Banyan?

Tara Christie:

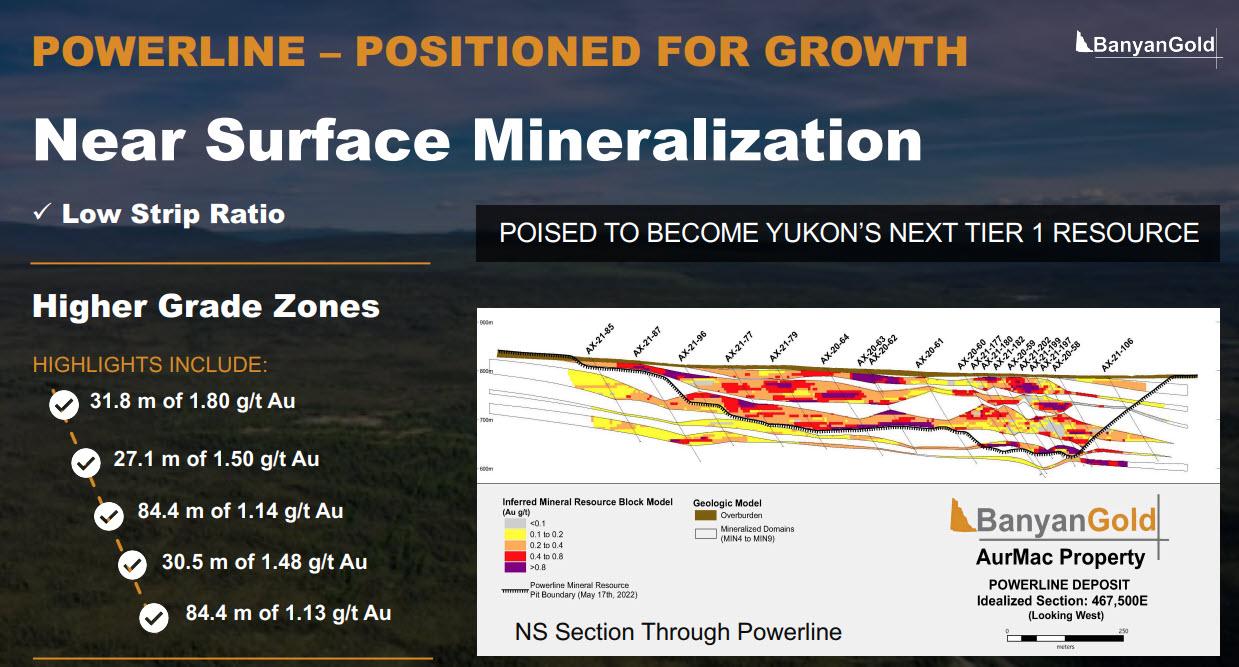

Well, first off we’ve had a great year this year. We drilled 25,000 meters. We’re still waiting for some of those drill holes back, but the ones that we put out showed that Aurex Hill and Powerline are connected, more consistent mineralization. We fill it in that area where we only drilled to 100 meters back at Powerline. We knew that that higher grade zone, in what we believe is likely your phase one mining area, which we did a little bit of high level engineering, looking at these deposits to give us a bit of a concept of how you might mine it from an engineering perspective.

An inferred geological pit is not necessarily a mining pit, and just a first pass. Then we also wanted to look at what would this look like as a heap leach versus a milling scenario? We’re doing metallurgy on both of those. We understand what those end bookends are, which I think is also important. It’s very early preliminary stuff, because you want to do this iteratively, as you get your metallurgy, as it’ll help us guide where we drill, where’s the higher grade?

Obviously, you’re phase one mining those higher grade areas. Looking at that, both geologically from the higher grade, structurally, and then also from a mining perspective, what actually would come in your first phases of mining, is important to inform our thinking for next year. Meanwhile, we’re waiting for our met work. We chose to not get back drilling again after the forest fires, because we thought, well, the market was starting to get bad, but we also knew that we would be better informed to have our drill results in hand, and spend so much time actually analyzing what we have.

With just under C$9 million in the bank, we’ve got a very strong position, and we are taking a bit of time to actually think about what the market will appreciate. We could have kept drilling into the Fall, but with the market not responding to good drill results I don’t think it would have moved the needle. We’ve seen fabulous drill results from all kinds of companies where it’s just been a selling opportunity. Right now, I don’t actually think that’s the most value add. We are taking a bit of time to actually think through our strategy. We’ll see where the broader market goes.

Meanwhile, we’re protecting our shareholders by making sure we have a strong treasury, and we’re not vulnerable, and people assume you have to finance at these prices. We’re being a bit defensive, because we know we have a pretty significant asset here, which we can add a lot of value to at a very low cost. We’ll take our time. I like to follow through on what I commit to, and that’s been part of our success. I’ll say, “This is what we’re going to do,” and then deliver on it.

We want to do that for 2024. We’ve got lots of cash to do that. We’ve got great supportive shareholders who we know will be there in the future, as long as we continue to deliver on what we say we’re going to do, so stay tuned. I’m not going to make commitments right now, because I think taking a little time to think things through, see where the market’s going, will really put us in a much better position. $9 million is a lot of money for us. That’s like three years of G&A. We weren’t given that money to stand still.

I’m not proposing that’s what we’re going to do, but we’re definitely going to make sure we spend it well. It was raised at $.40 and $.56 at the front end. I look at every one of those dollars as being worth 30 to 40% more. The value add that we have to get, how we spend them has to reflect that. That means, yeah, we’re taking a bit of time to do some deep dive and a lot of thinking.

Goldfinger:

What I hear you say is that you have C$9 million in the treasury, you’re taking some time to think things through. Taking a few months to think things through and see which way the wind is blowing in the market, and what investors want to see.

In the meantime, you’re preparing yourself for producing a PEA, and doing some feasibility level mine planning kind of work. And I think you have almost one hundred holes still pending assays, is that right?

Tara Christie:

69, yeah.

Goldfinger:

Okay, good number! You’ve got a lot of holes pending assays. Put it all together, it’s not a stretch to say you could have 7-8 million ounces at AurMac. That’s a lot of gold, so I think it makes a lot of sense to take some time to think things through and start to put some thought into the economics of what a mine might look like. Doing some mine planning makes a lot of sense, and it also makes sense to see how the market environment evolves.

The fact that you don’t have to raise money unless you really want to is a luxury in this environment. I think that’s very important. Yeah, the share price is obviously down, just like every other gold mining stock is down. The fact that you’ve been a little quiet might actually be a good thing. Let’s talk about the Yukon more broadly. There’s been some consolidation that’s happened, a few little takeouts have occurred the last couple of years.

Some new investors have come into the territory, the Lundins with Fireweed, Snowline has a major mining company as a major shareholder. How do you think the territory plays out from a gold mining standpoint over the next, I don’t know, five years? Is this going to be consolidated by one or two really big companies, or is this going to stay with maybe one or two majors, one or two mid-tiers, and a lot of juniors?

Tara Christie:

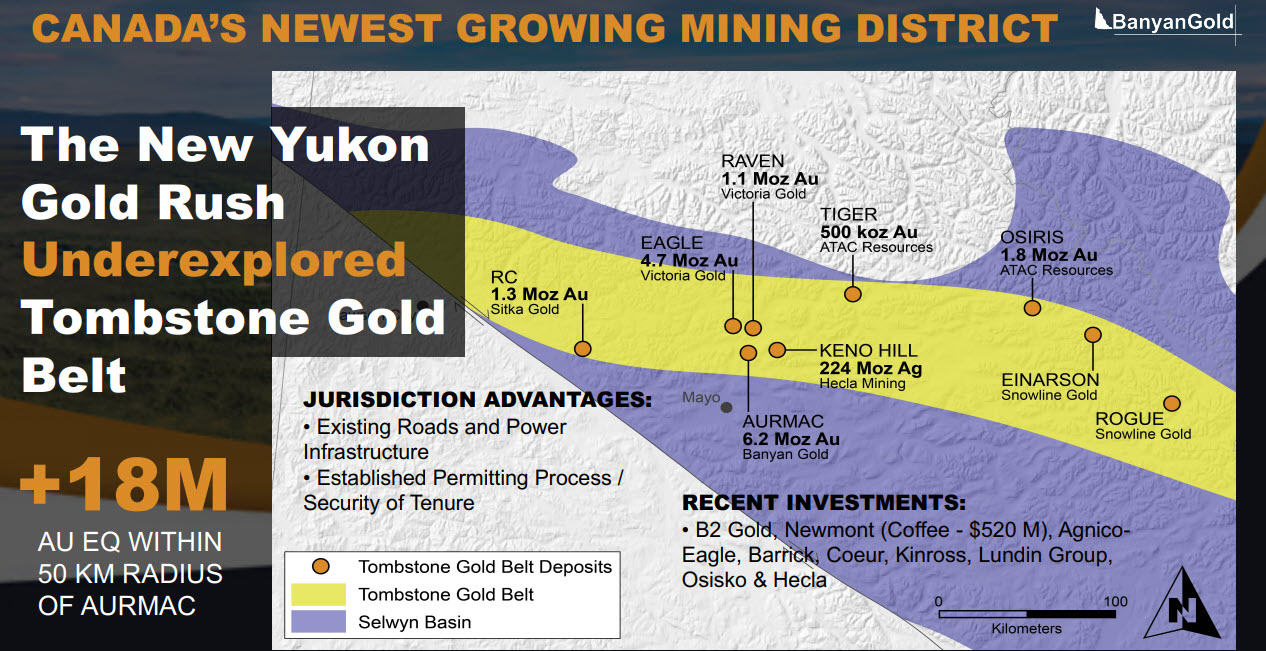

That’s a hard question, because there are a lot of things that are solid. Definitely, the B2 Gold investment in Snowline is bringing attention. Fireweed with the Lundin Family, that’s bringing additional eyes. I think time is actually on our side here, as people get to understand what is happening in this area of the Yukon (Mayo Mining District). If you drew a circle around us right now, we’d have 15 million ounces in gold equivalent resources. That doesn’t include Snowline. It also doesn’t include the new Raven drill results that will come out in the updated resource from Victoria Gold.

I think that’s super exciting. There’s high grade and it’s just right across the valley. We can stand at our Thompson Creek Camp and look across the valley, and see the lights of those drills (at Victoria’s Raven Deposit), where those beautiful holes came from. I wouldn’t be surprised if that resource is 2.0 grams/tonne. It shows we’re making new discoveries in a district where we thought everything had been found and it was like, “Oh, Victoria Gold, there’s the mine,” but look at what else they have. They’ve got 550 square kilometers, other targets, but I’m pretty excited about what they found at Raven.

If they can find it, we have 300 square kilometers. That’s the other piece that actually might be more exciting if we did some regional exploration work. Because in this market, people don’t care about drill holes. You can put out drill holes, and some of our drill holes were great, adding 10,000-20,000 ounces per hole from the ones that were connected. The market didn’t care. Even with our resource update, people had already factored that in by the time we got the resource, because it’s such a simple deposit. You can do the math yourself.

What would we need to drill out to get to 8 million ounces? Well, it’s because it’s such a predictable mineralization, I think that’s partly why our results don’t get much excitement as people already factor that in. Some of this regional work, showing that we have other potential for intrusions, and our Nitra Property does. Victoria Gold just bought the Gold Dome Property, which is a known intrusion-related deposit, which is right outside, right on our property boundary.

Looking at that historically, I believe, and I think Victoria Gold’s geologists agree, that they drilled it in the wrong direction. We did a little bit of work around there, and there’s a lot of placer mining streams over there. That placer mining gold came from somewhere. There’s some known intrusions, none that are right on the surface that are visibly mineralized, but nobody’s done any work there, or really modern day properly done grids of soils and prospecting.

We did a little bit this year, and certainly there’s a lot more to do. It’s a very large claims package. Giving ourselves a bit of a start on that, because making a new discovery in this market might actually bring some more excitement. There are going to be discoveries in this district. We’re right across from the McQuesten Valley, the Nitra property, there’s the McQuesten River, and then there’s Sitka on the other side. They’ve been making some new discoveries.

Goldfinger:

Yes, Sitka has had some nice hits.

Tara Christie:

It’s all the same belt of intrusion-related rocks. There is potential for more discoveries. Meanwhile, we can continue to advance AurMac, de-risk it, and make it a very compelling resource. There’s no property in the Yukon that has as much baseline data that’s held by a junior as our project, that hasn’t gone into permitting yet.

That means that if you actually designed a project, you could go into construction within four to five years, like Victoria Gold, once you get the project designed. Of course, you have to make sure you have the First Nation on your side, and you can’t really do that until you decide what the project is.

Goldfinger:

Right.

Tara Christie:

One settled First Nation in this area, which works with Hecla and Victoria Gold, so that’s a benefit. It does process quite a bit more predictable than in many other places in Canada and the world, where permitting can be quite challenging.

Goldfinger:

I think that the Yukon Territory is a massive, massive land area. And it is highly underexplored due to a few factors including the extremely small population, and remote nature of exploration in this territory.

Tara Christie:

It’s so under-explored.

Goldfinger:

It’s so under-explored, and there’s a lot of gold there. There is a large mineral endowment and It’s not just gold, there is copper, lead, zinc, and I could go on. There’s a lot of new discoveries to be made in the Yukon. I’m pretty confident in that, and it’s been proven over the last decade, with a lot of new discoveries.

As I think about how we can generate more shareholder value for Banyan shareholders now, one thing that a lot of people may not have understood about this downturn in 2023 is a lot of it has to do with the Fed rate hikes, and 5.5% on the Fed funds rate. I am not sure where the Bank of Canada is at, four or four and a half percent, but they’ve hiked a lot as well. The cost of capital goes up.

Companies that do not generate cash flow, but they have some sort of terminal value for their asset at some point, 10, 15, 20 years down the road, all of those values get dropped down because the discount rate is higher. Cash flows further out on the mine life are worth less and less as the discount rate increases.

Tara Christie:

Yep.

Goldfinger:

That’s really hurt a lot of juniors that don’t have cash flow. The nature of the sector is to invest in an asset that has some terminal value out there in the future, and then to do all the work required to de-risk that asset and unlock its value for shareholders.

Obviously, the gold price affects investor sentiment in the junior mining sector. However, we are currently experiencing an unusual market environment with a strong gold price at a time when investor sentiment on juniors couldn’t be much worse.

How do you generate value? I think it’s either through a new discovery, or you further de-risk the project and demonstrate robust economics through PEA/PFS etc.

Those are pretty much the only two clear ways that I can see that you can generate value at this point in time, aside from magically, you get a permit or something like that.

Tara Christie:

Obviously, the rate hikes have had that impact on the terminal values, but it’s also given investors an alternative to get a decent 5%-6% return with low risk.

That means why not take the safe return? There’s so much uncertainty. It also means that our institutional investors, which are generally the ones that would invest at this stage, and really take it the next lap, are liquidity constrained. If you look at our volume, there’s not a lot of volume trading, which I guess is actually a good thing. Our share price has traded down on light volume. I’d be way more worried if we had huge volumes with the share price going down, meaning that there was a broader dissatisfaction or lack of confidence.

BYN.V (Weekly)

That’s happening across the sector, some fund managers are getting squeezed. We’re seeing some of them are actually having to sell positions to deal with the liquidity issues. It’s not simply because they don’t like the stock, it’s because they essentially have no choice. That’s just what their rules require them to do. That’s putting undue pressure on the space as well, because the gold price is actually pretty strong. We saw $2,000 gold again today (November 3rd, 2023).

For juniors like me, I worry about this. We’ve got these majors that have significant cash balances growing on their balance sheet at $2,000 gold. Even with some of the inflationary prices on all the sustaining costs with some of the big companies. In Australia it seems that it’s a very different market. There still is a lot of excitement for gold mining and exploration in Australia, and if we compare it to our North American market. It’s a dichotomy.

It worries me, because I don’t want my company to have some offer at a low premium when market share prices are at these levels. I think that at some point things have to re-rate. That’s partly why our strategy is what it is, we know we have a real asset that is desirable, so making sure that we do everything to protect that shareholder value. Yes, advancing it, de-risking it, but would I risk going out and spending a whole lot of money right now on a program?

That’s why we don’t have to drill this winter. We could, if we really thought we could add value. We really do have a better understanding of some of the higher grade areas. I think you’d need to drill up a significant amount in order for that to be meaningful. Having a bit of patience, making sure shareholders know that, that’s part of our strategy is to make sure that when we go full guns again, that we have a clear path to create value, and it will be appreciated in the market.

I looked at the drill results we’ve put out already, and they were good. They didn’t really get a lot of excitement. I’ve seen companies spending a lot of time and effort on news releases, and some companies put out two or three holes per news release and we’ve seen their price successively go down. So I don’t think it’s a good use of our time right now.

Goldfinger:

Yeah, in a way, I think it’s an effective strategy to just lay low, and dot your I’s and cross your T’s where you can without a lot of capital spending. Then in early 2024, at some point in the future, you wake up and you say, “Well, this is our plan,” and there is a sense of urgency. If you don’t get in now, you’re going to miss out. The valuation opportunity speaks for itself. I don’t think we need to go over that. It’s 6.2 million ounces, you can see the market cap, you can do the math on your calculator.

For the most part the psychology of investors in this sector today is that we’re in a downtrend, it’s year end, and there’s no urgency to buy. The next two months are likely to be challenging one for most juniors simply due to the tax loss selling overhang. Then on the other hand, if you’re an investor, it’s an opportunity. Just depends on how you want to see it, right?

Tara Christie:

I’m not convinced tax loss selling is going to be significant this year. I think most people have long ago crystallized their losses for tax loss. There’ll be a small few, but is it going to be significant? I’m not convinced that…

Goldfinger:

There’s probably not a lot of gains to offset either. What can shareholders expect from Banyan in the next year? Obviously, I’m not going to nail you down to certain dates, but just a broad overview of what we can expect.

Tara Christie:

Well, the first thing we’re going to do is we’re going to make sure that we’re very strategic in how we spend our account, that we’ve taken the time, and quite frankly, have a bit of time. We’ve been so build ounces, build ounces-focused, but taking this time to actually analyze what we have, look at it is actually a real value add. Same with some of the engineering, the mining, getting the baseline data in order, so that they could advance permitting if we wanted to take that approach.

Getting the baseline data that we could take is a PEA. One of the things that we’re actually doing in a very systematic way, where we’re saying, “Okay, if we drilled out a million ounces of our highest grade, what would that cost? What is our likelihood of success?” We’re doing a lot of work in the background, looking at, well, if we want to grow this to 8 million ounces, how many more holes would we think we have to drill? Where would we drill them? Where would we get the value?”

Looking at that regional exploration, “Okay, what are our odds of success? How much money is it going to take? What would we do?” That’s a very logical way to get all your options, understand what the costs are, what the risks and the potential rewards are, and then make our decisions based on that in the context of the market. Look for us to do that. We are very strategically going to come up with a plan for 2024 that has volume.

Meanwhile, we’ve got our met work, which we said is coming along. We’re pleased about it, we’re already planning a second phase. That’ll be part of 2024, because the work never ends until you actually build a mine.

Goldfinger:

Then it keeps going, even as you’re building the mine and you’re operating the mine, right?

Tara Christie:

Well, and looking at that optionality was a big part of our strategy. I think we were a bit pigeonholed, as you’re a heap leach just like Victoria Gold, which then people will then look at the challenges of Victoria Gold, and step back and go, “Huh, we actually have optionality here. We should be looking at the broad range.” Particularly with Raven and that resource, I think they planned for Q1, don’t quote me on that, but that being so close to us, and having obvious synergies.

If there’s a mill, there’ll be a district mill somewhere with all these discoveries that have been made. I think that is actually a real value add for our shareholders to have that, and for us to understand, 90% recoveries for mills generally versus like 74. The long-term value of a resource can be different. A large mining company might want to build a more capital intensive project to get a better IRR, and a longer mine line and bigger resource.

That, I think, will add a lot of value. That’s coming. We will have our drill results. I’m not expecting drill results… When you got 6.2 million ounces, 6.2 million ounces, yes, I can see a view to eight million ounces, maybe beyond that as well.

Goldfinger:

It’d be interesting if you had a hole that was like 200 meters of a gram. It’d be interesting to see what the market would respond to that. I don’t know, I’d be very curious. I’m not saying that you’re going to have that, but it’d just be interesting to see if you had one that was a little bit higher than your current average, over a really good interval, it’d be interesting to see.

Tara Christie:

Would that honestly be material?

Goldfinger:

Right, in the context of 6.2 million ounces? No, probably not, but it would be interesting because people look at the headline intervals, and they do get attention.

Both Hecla and Victoria Gold have been acquisitive in the territory in the last year. Victoria Gold is obviously your largest shareholder, and Hecla has Keno Hill in your neighborhood. How do you generate competitive tension there, and do you talk with Hecla at all?

Tara Christie:

They’re our neighbors, and actually, they’re staying in our camp. We’re actually getting some cost recovery, which is something that’s different about our balance sheet as well. You’ll see we actually have this thing called income, which offsets…

Goldfinger:

Banyan has income? I didn’t know that!

Tara Christie:

We have income, yeah. Yeah, we talk to them. There’s a lot of people looking around the Yukon, and I think people are well aware of that. You’ve got B2 Gold investing in Snowline. Newmont with the Coffee Gold Deposit, you’ve got Kinross, and Agnico in various projects. They’ve invested in the jurisdiction. I don’t think it’s a secret that companies continue to look in the jurisdiction, and keep themselves up to speed on projects. I personally believe at some point there will be, as we start to talk about consolidation in the Yukon, I think it’s a natural progression. How do you develop that competitive tension?

Well, you make sure that all of the corporates have a bit of knowledge of you. That’s part of the problem, if one corporation feels that they are behind in being able to do due diligence, and somebody has an advantage, it’s harder to get some competitive bids. I think we’ll see that in the Yukon. When the tide turns, I think it’ll turn hard. Corporates, I think, would be wise to be looking before that tide turns, because everything’s so cheap right now, and really ridiculously cheap for resources that are in areas where you can build a mine.

I don’t have a crystal ball, but if I was looking for opportunities and I was cash flowing significantly, why wouldn’t you go shopping when things are on sale? There was a quote from Warren Buffet, “Whether it’s stocks or socks, I like to buy things when they’re on sale.” I know majors often like to wait until things are really expensive, like the Great Bears that are valued at high prices, and then make their purchases, but…

Goldfinger:

It’s really interesting, because you think about the Great Bear transaction. Obviously, that was a very special discovery, a very special project, but Kinross paid a very high dollar price tag for that. Yeah, it’s like 5 million ounces. Yeah, it’s higher grade than the AurMac project, but it’s 5 million ounces. At the end of the day, it’s not even as big as AurMac. That was $2 billion, and you’re a C$78 million market cap this morning, right?

Tara Christie:

Crazy. Yeah.

Goldfinger:

It’s very interesting how major mining companies make these calls, something they really loved about that project that they couldn’t resist, but they could buy Banyan, and they could even buy neighboring projects for a fraction of that price tag.

Tara Christie:

Yes, they could buy an operating mine for that, right next door to us, and us, for that price tag, and a few others.

Goldfinger:

It’s just very interesting to see some of these big ticket transactions that have occurred. Then you look at the Taylor/Hermosa Deposit in Arizona, which was bought by South32 for C$2 billion in 2018. It’s till not in production, actually not even close. They took a $500 million write down on the asset in their latest quarter, because of construction/permitting challenges and lower metal prices.

Some of the decisions that the majors make do not seem very rational from my perspective. In addition, they also seem to overlook some very good projects.

Tara, thank you for your time.

Tara Christie:

Yeah, thank you.

Goldfinger:

I think the last time we chatted at this conference, the share price was around $.05, and it proved to be a great buying opportunity. Knock on wood, it’s another great opportunity.

Disclosure: Author owns BYN.V shares at the time of publishing and may choose to buy or sell at any time without notice.

___________________________________________________

Disclaimer

The article is for informational purposes only and is neither a solicitation for the purchase of securities nor an offer of securities. Readers of the article are expressly cautioned to seek the advice of a registered investment advisor and other professional advisors, as applicable, regarding the appropriateness of investing in any securities or any investment strategies, including those discussed above. Banyan Gold Corp. is a high-risk venture stock and not suitable for most investors. Consult Banyan Gold Corp’s SEDAR profiles for important risk disclosures.

EnergyandGold has been compensated to cover Banyan Gold Corp. and so some information may be biased. EnergyandGold.com, EnergyandGold Publishing LTD, its writers and principals are not registered investment advisors and advice you to do your own due diligence with a licensed investment advisor prior to making any investment decisions.

This article contains certain forward-looking information and forward-looking statements within the meaning of applicable securities legislation (collectively “forward-looking statements”). Certain information contained herein constitutes “forward-looking information” under Canadian securities legislation. Generally, forward-looking information can be identified by the use of forward-looking terminology such as “expects”, “believes”, “aims to”, “plans to” or “intends to” or variations of such words and phrases or statements that certain actions, events or results “will” occur. Forward-looking statements are based on the opinions and estimates of management as of the date such statements are made and they are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed by such forward-looking statements or forward-looking information, standard transaction risks; impact of the transaction on the parties; and risks relating to financings; regulatory approvals; foreign country operations and volatile share prices. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Actual results may differ materially from those currently anticipated in such statements. The views expressed in this publication and on the EnergyandGold website do not necessarily reflect the views of Energy and Gold Publishing LTD, publisher of EnergyandGold.com. Accordingly, readers should not place undue reliance on forward-looking statements and forward looking information. The Company does not undertake to update any forward-looking statements or forward-looking information that are incorporated by reference herein, except as required by applicable securities laws. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SEDAR.com for important risk disclosures. It’s your money and your responsibility.

situs slot danagacor