The Federal Open Market Committee (FOMC) will announce its interest rate decision at 2 pm EST tomorrow, followed by a press conference with Fed Chairman Powell at 2:30 pm EST. Only 24 hours ago, it seemed like a quarter point hike to 5.25% on the Fed Funds Rate (FFR) was a foregone conclusion. However, today’s weak JOLTS data, in combination with carnage in the regional banking sector, has thrown some doubt into the mix (from a 93% probability of a 25bps hike to roughly 85% at last check).

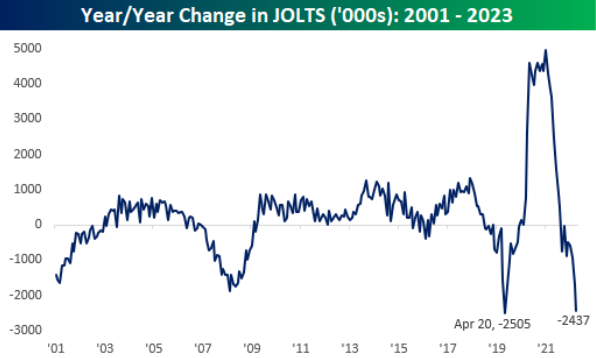

The JOLTS data showed job openings posting a near-record year-over-year decline in the month of April.

Today’s JOLTS data brings additional signs of a cooling labor market. The ratio of hires to openings in the private sector rose to 0.673, the highest level since April 2021. When this ratio goes up, it implies that firms are having an easier time filling open positions. This will be welcome news to a Fed that has been focused on engineering a rebalancing in the labor market that will help to cool off inflation. The trend in layoffs is clearly moving higher, but still not at a level high enough that the Fed will be concerned it has caused too much damage to the US labor market.

Meanwhile, the damage in the US regional banking sector is becoming increasingly pronounced. The KRE fell to fresh 52-week lows today as deposit flight to mega-cap money center banks continues in the wake of the 2nd largest US bank failure in history, First Republic Bank.

KRE (Daily)

Despite today’s market turmoil, the WSJ’s ‘Fed Whisperer’ Nick Timiraos signaled that a 25bps rate hike is a virtual certainty on Wednesday. The bigger question will be whether Powell will offer any hints that the Fed is leaning towards signaling an end to the fastest rate-hiking cycle in Federal Reserve history.

Whatever Powell decides to say during tomorrow’s press conference, the 2-year US Treasury yield is sending a strong message that the Fed is on the verge of making a policy error by tightening too much. Monetary policy acts with long and variable lags, and judging by the yield on the 2-year note, the market is betting that the Fed will be forced into a major easing cycle sooner than later.

Remember that the Fed is still in its fastest rate-hiking cycle on record, at the same time that global debt levels have never been higher. Large US budget deficits and a debt ceiling debate in Congress only serve to make the situation even murkier.

Gold has been sniffing out the weakening global economy and the Fed’s dubious policy path for the last couple of months. Today, gold rallied 1.6% in an attempt to punch through the upper end of its recent trading range.

Gold (Daily – Comex)

Today’s gains in gold are encouraging for bulls; however, it will be the weekly close that carries the most weight. Bulls will be looking for a new all-time high weekly close above $2,028/oz to signal that the recent range-bound consolidation has resolved to the upside.

Support is evident near $1985, followed by $1950.

While an increase to 5.25% on the FFR tomorrow appears to be a foregone conclusion, I will be most interested in whether Powell acknowledges the recent large downside surprise in GDP and the sharp decline in job openings. In addition, any hint that a rate cut could be possible later in the year would likely be cheered by precious metals and equities. Meanwhile, a Powell that emphasizes there is more to be done to rebalance the labor market and bring down inflation is likely to be met with jeers from traders.

At this point, the comparisons to 2008 are overdone and not particularly helpful. However, I will note that I am increasingly reminded of the 2006/2007 market period. The Fed hiked to 5.25% on the FFR in June 2006, and in the process helped to tighten liquidity conditions enough to help bring about the beginning of the Global Financial Crisis a year later.

The more things change, the more they stay the same.

_____________________________________________________

DISCLAIMER: The work included in this article is based on current events, technical charts, company news releases, and the author’s opinions. It may contain errors, and you shouldn’t make any investment decision based solely on what you read here. This publication contains forward-looking statements, including but not limited to comments regarding predictions and projections. Forward-looking statements address future events and conditions and therefore involve inherent risks and uncertainties. Actual results may differ materially from those currently anticipated in such statements. This publication is provided for informational and entertainment purposes only and is not a recommendation to buy or sell any security. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SEDAR.com for important risk disclosures. It’s your money and your responsibility.