Around this time of year (since 2017), I publish a Tax Loss Silly Season Shopping List of stocks that I believe offer attractive risk/reward profiles. I do this exercise for myself as much as I do it to benefit my readers. I usually start with 15-20 candidates, then gradually whittle the list down to the six best ideas. This year’s list also happens to feature two names from last year’s list, albeit at lower share prices than they were a year ago.

It’s important to remember that this is a list of stock ideas that should prompt the reader to do their own research. Furthermore, these are trade ideas based upon a well known seasonal tendency in the junior mining sector; most investors complete their tax loss sales by December 15th, thus creating a notable drop-off in selling pressure in the final two weeks of the year.

As usual, the criteria for this year’s list is the stock must be down year-to-date and well off its highs for the year. Thus making it a candidate for selling that is motivated primarily by individual tax liability considerations (booking losses to offset taxable gains elsewhere) that have little to do with the future opportunity available to shareholders of the company.

The exercise of picking stocks that have had poor performances year-to-date is an interesting one because most of the poor performances have some common themes including:

- Delays (drilling, assay lab results, permits, etc.)

- High investor expectations at the beginning of the year (high market caps relative to the stage of the companies’ projects etc.)

- Companies that are pointing to next year, thus creating a situation in which many investors don’t see much risk of missing out by selling and waiting 31 days

While narrowing the list down, I focused on companies with high-quality management teams, solid cash positions, insider buying activity, and actionable catalysts/news flow on the way in Q1 of 2023. Each one of the companies in this year’s list has a legitimate chance of delivering sizable returns over the next 12 months. However, each company is also dealing with varying levels of investor disappointment (and the resulting overhead share supply overhang) that will need to be reversed by delivering strong results and meeting key milestones on time in 2023. These are trade ideas, not marriages.

The annual tax loss silly season shopping list is not intended to offer an exhaustive analysis of each company. Instead, the focus is getting to the salient points that make these stocks attractive propositions at their current market valuations. Think of it as a list of ideas that might prompt the reader to dig deeper, review company filings on SEDAR, schedule a meeting with the CEO(s), or add some symbols to a watchlist.

While failure is the norm in junior mining exploration and financing risk is always present, each of the companies on this year’s list have had varying degrees of exploration success and demonstrated strong financing capabilities.

I will add one final point before diving into this year’s list. There were so many good candidates, I found it challenging to limit the list to only six symbols. I also decided to limit the universe of stocks to explorers/developers with market caps below C$200 million (Victoria Gold would have made the list if I didn’t add this market cap restriction) – these stocks usually offer the most upside potential, and often have been sold down the most on a percentage basis.

2022 Tax Loss Silly Season Shopping List

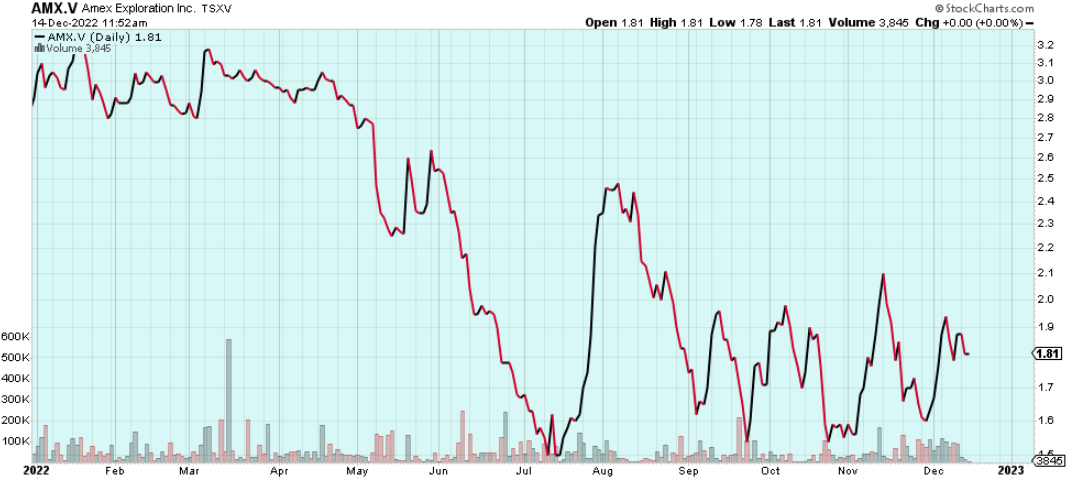

Amex Exploration (TSX-V:AMX, OTC:AMXEF) – Amex shares are down ~40% in 2022, significantly outpacing the ~15% decline for the GDXJ.

AMX.V (Daily YTD)

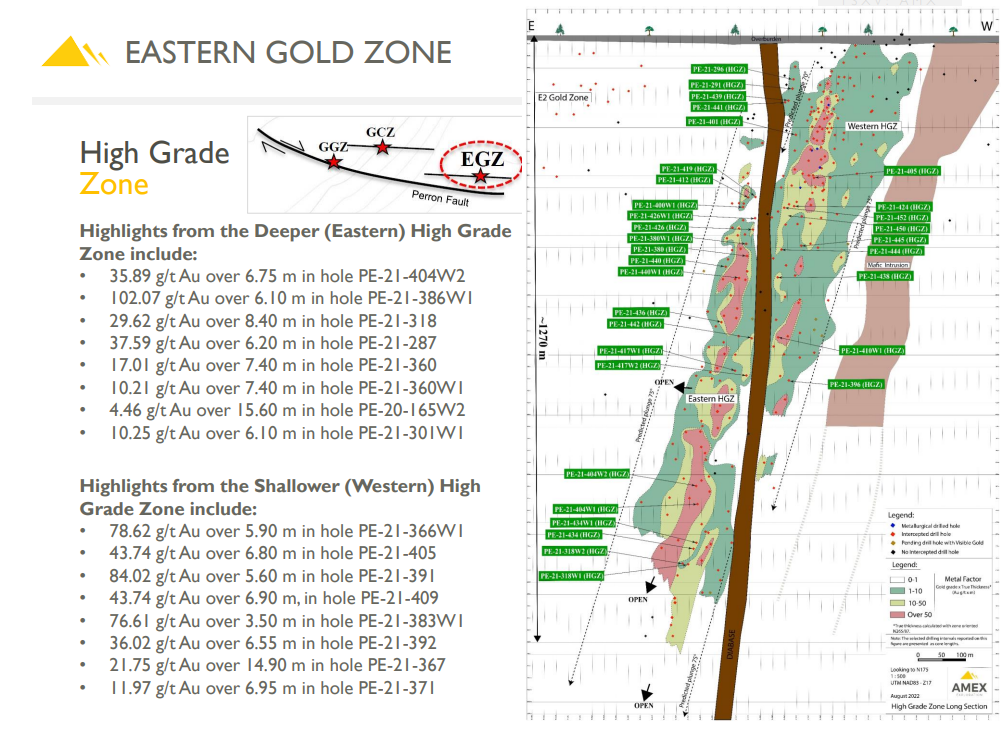

Strengths & Opportunities: Amex’s flagship Perron Project hosts extensive high-grade gold mineralized zones in a tier-1 mining jurisdiction (Abitibi Region of Quebec). Amex is planning to publish a maiden resource estimate for the High Grade Zone (HGZ) and Denise Zones in Q2 of next year. The company recently made a new discovery at the Team Zone, including drill intercepts of 6.75 g/t gold over 14.50 meters and 10.05 g/t gold over 9.5 meters. Amex has intercepted visible gold mineralization at the Team Zone over an area of approximately 300 meters by 150 meters from surface to a depth of nearly 400 meters.

More than $30 million in the treasury gives Amex plenty of cash runway and financial flexibility. The Perron Project is located in an ideal location for gold mining in a tier-1 jurisdiction (Quebec). The compelling combination of grade, scale, and location makes Amex an attractive acquisition target for a large gold producer.

Risks: Gold price risk, gold sector risk, financing risk. The biggest catalysts for Amex are the maiden resource estimates for the HGZ/Denise Zones, and continued exploration results across the Perron Property. Market expectations are for a minimum 3,000,000 ounces in resource at several grams/tonne average grade. If the MRE comes short of expectations it will be a disappointment to investors.

Share price and market cap at time of publishing: C$1.79 (C$185 million)

Cash position as of 9/30/2022 = C$32 million

Aurion Resources (TSX-V:AU, OTC:AIRRF) – 2022 has been a trying year for Aurion with the share price tumbling from $1.30 at the end of 2021 to below $.40 at its September low:

AU.V (Daily YTD)

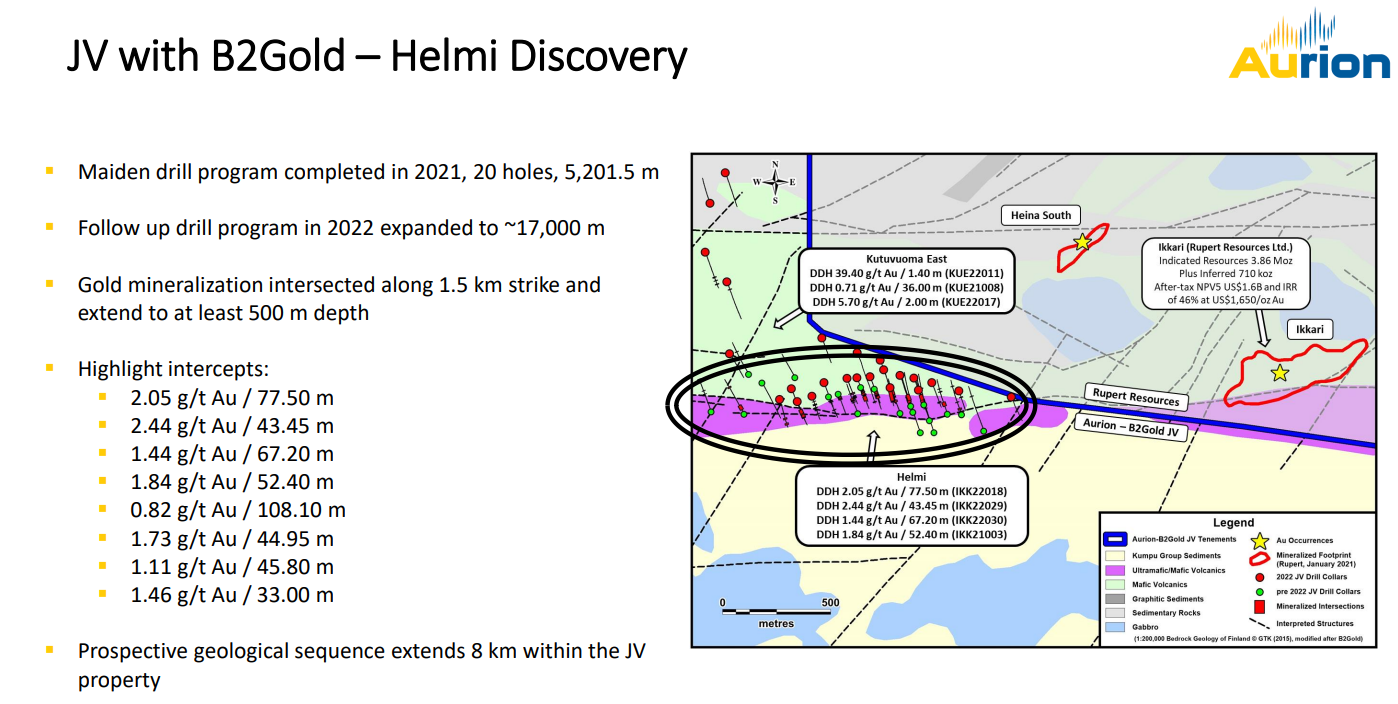

Strengths & Opportunities: Chairman David Lotan has been a relentless accumulator of Aurion shares on the open market with purchases totaling more than $500,000 in the last six months. Aurion has assembled a district scale project portfolio in one of the world’s emerging gold belts, the Central Lapland Greenstone Belt of Finland.

The Helmi JV with B2Gold (70% B2/30% Aurion) is Aurion’s most prominent catalyst by giving a solid underpinning of value based upon drilling to data and to the neighboring Ikkari Deposit that hosts more than 4,000,000 ounces at an average grade of ~2.5 grams/tonne gold.

Rupert’s recent PEA showed a US$1.6 billion NFP and a 46% IRR using a US$1,650 gold price. Furthermore, the pit shell illustrated in the PEA runs right up to the property boundary with Helmi. The continuity of gold mineralization along trend to the west from Ikkari, and the strategic importance of being able to engineer an open pit of adequate dimensions makes Helmi a natural acquisition for the owner of Ikkari.

Risks: Aurion has all the usual gold sector and gold price risks that any junior mining company faces. So far, it has been a challenge for Aurion to follow up on some of the high expectations that were created during the company’s incredible share price run in 2016/2017. High expectations could continue to be a challenge for Aurion.

Share price and market cap at time of publishing: C$.58 (C$68 million)

Cash position as of 9/30/2022 = C$12 million

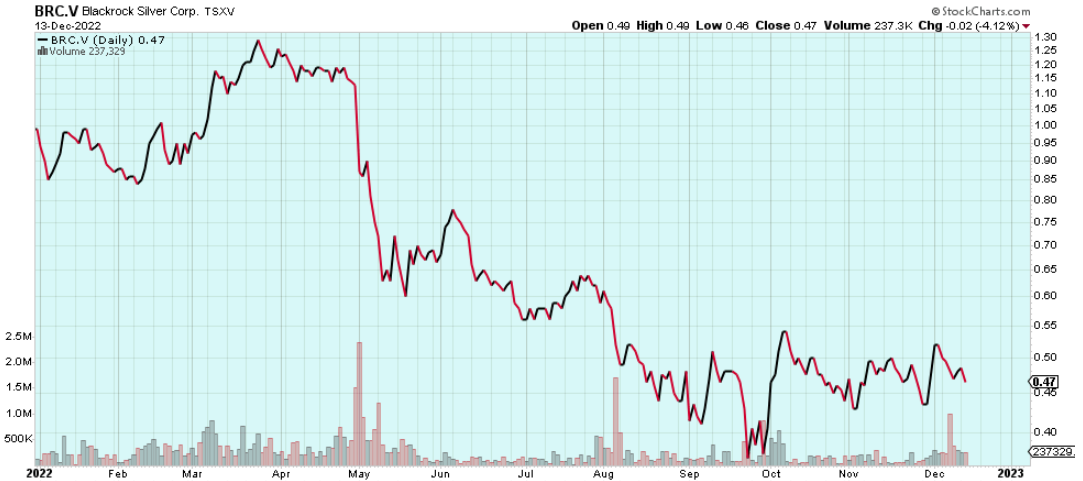

Blackrock Silver (TSX-V: BRC, OTC:BKRRF) – After phenomenal years in 2019 (up ~450%) and 2020 (up more than 300%), Blackrock shares have declined more than 50% in 2022.

BRC.V (Daily YTD)

Strengths & Opportunities: Blackrock is a well positioned Nevada gold/silver exploration & development company. The Tonopah West Project underpins the valuation of the company with an inferred maiden resource estimate totaling 42.6 million silver-equivalent ounces at an average grade of ~450 g/t Ag-Eq. CEO Andrew Pollard has been a regular buyer of BRC shares on the open market since taking the helm as CEO in May 2019:

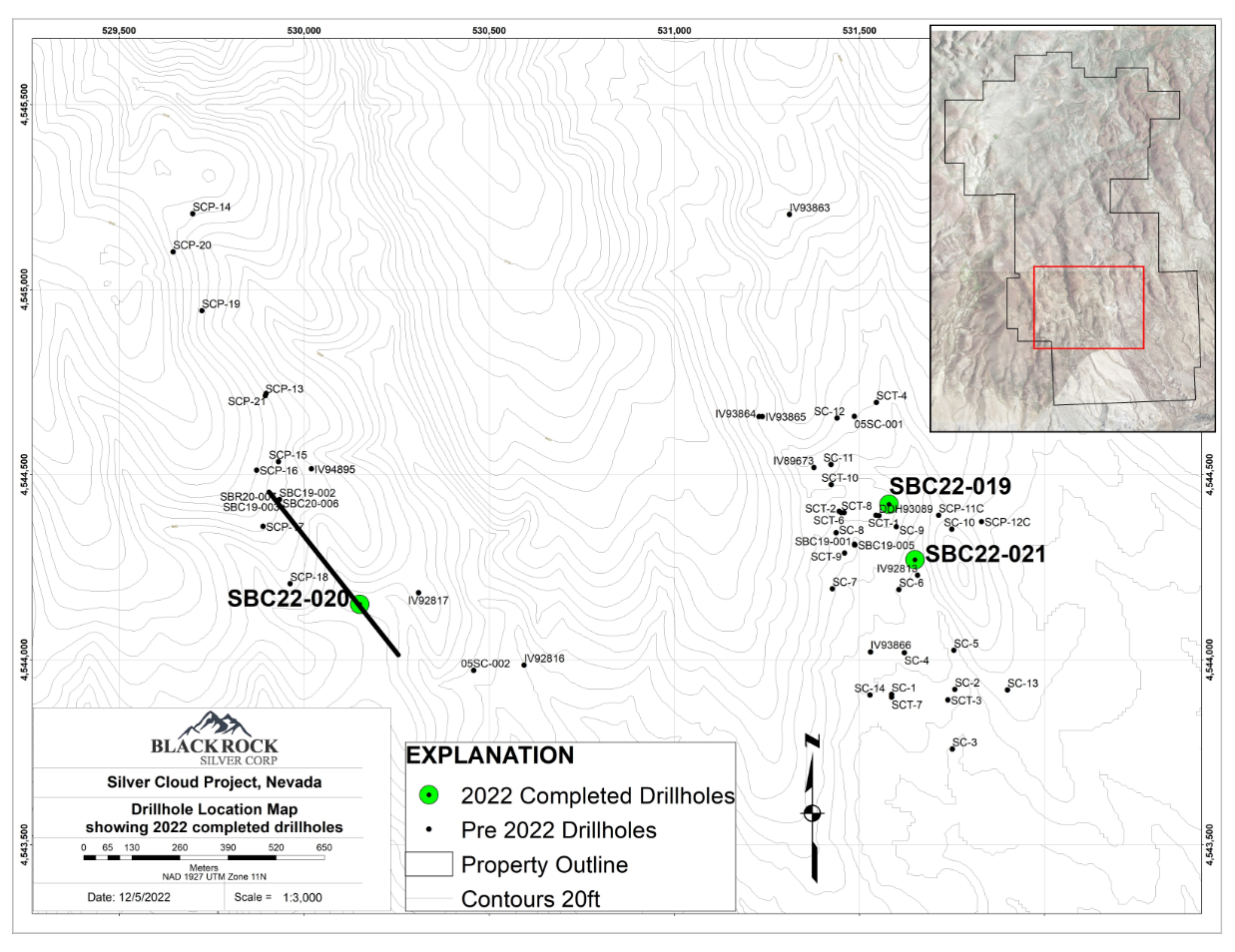

Prominent shareholders include First Majestic Silver (NYSE:AG) and Eric Sprott. While Tonopah West is the foundation of Blackrock, the company just made a discovery at its Silver Cloud Project in the Northern Nevada Rift. Pollard calls Silver Cloud the “donut hole” in the middle of the Hollister and Midas Mines. Hollister and Midas (Hecla Mining) are two of the highest grade mines in Nevada and Blackrock believes there is potential for a “Midas style” gold deposit at Silver Cloud.

Last week, Blackrock announced that it intersected 52.62 g/t gold and 606 g/t silver over 1.5 meters (hole SBC22-020) in the Northwest Canyon area of Silver Cloud. This hole represents a new high-grade vein discovery now known as Zeus.

Hole SBC22-020 targeted a structure that was projected based upon two historical drill intercepts (one drilled by Blackrock in 2019 and the other drilled by Placer Dome in the early 2000s). The bonanza grades are associated with a banded quartz vein that contains black sulphides, and the 606 g/t silver is the highest-grade silver intercept on the Silver Cloud property to date.

1.5 meters is a significant interval when it contains grades this high. Blackrock’s opportunity, and challenge, will be to now follow up on this intercept and demonstrate that the vein continues over a considerable strike length. The evidence that it does is encouraging based upon Blackrock’s 2019 hole #2 that intersected 8.32 g/t gold over 1.52 meters and Placer Dome’s SCP-15 that intersected 5.61 g/t gold over 12.2 meters. These assay intercepts represent a high-grade drill defined structure separated by 425 meters.

Risks: BRC’s share price was highly correlated to the silver price earlier in the year as silver fell from over $28/oz to below $18/oz. In addition, drilling in Nevada isn’t cheap and Blackrock will need to complete a financing in early 2023 to fund follow-up drilling at the new Silver Cloud discovery as well as resource expansion drilling at Tonopah.

Share price and market cap at time of publishing: C$.47 (C$85 million market cap)

Cash Position as of 9/30/2022 = C$2 million

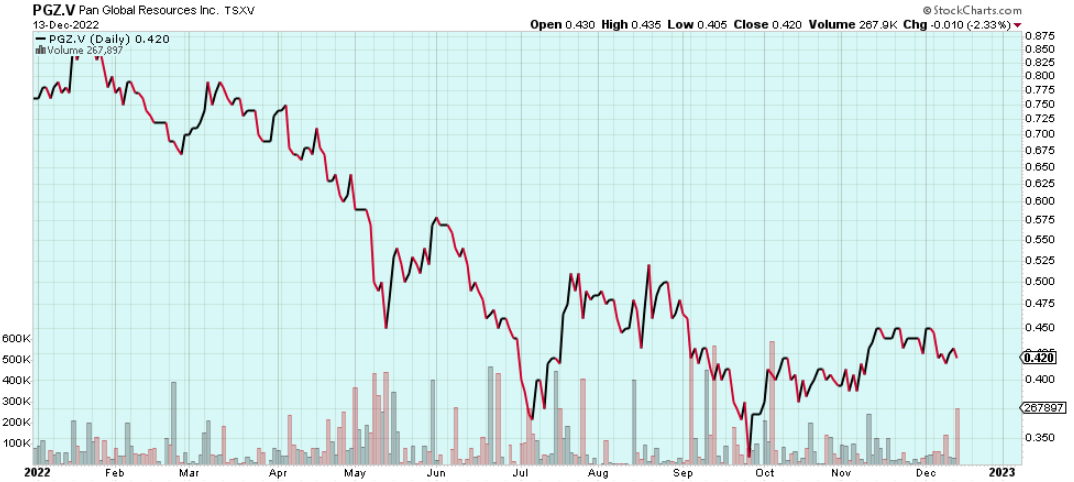

Pan Global Resources (TSX-V:PGZ, OTC:PGNRF) – Pan Global shares have suffered along with other base metals exploration stocks in 2022 – PGZ shares are down ~45% year to date.

PGZ.V (Daily YTD)

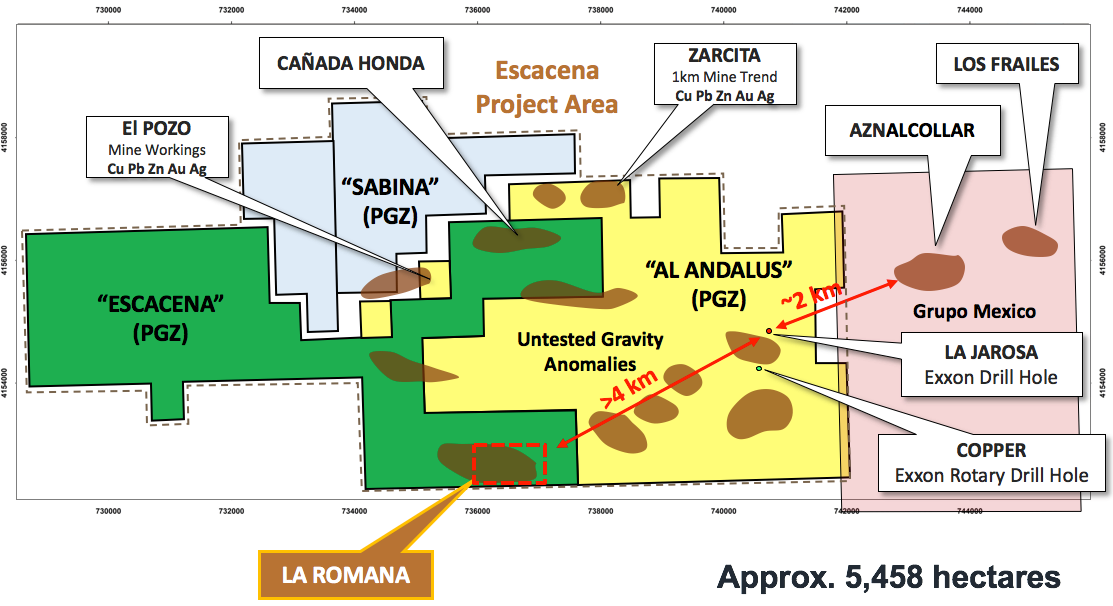

Pan Global has 100% ownership of The Escacena Project located in the Iberian Pyrite Belt of Spain. Escacena is located near operating mines at Las Cruces and Rio Tinto, immediately adjacent to the former Aznalcollar and Los Frailes mines where Minera Los Frailes/Grupo Mexico is in the permitting stage to restart mining. The Escacena Project hosts the La Romana copper-tin discovery and a number of other prospective targets including La Jarosa, Hornitos, Zarcita, Romana Deep, Pilar, Bravo and Barbacena.

Romana is a high-grade massive sulphide copper/tin discovery that hosts grades as high as 14.25% copper in diamond drilling. PGZ is currently drilling an intriguing geophysical target called Romana Deep. Romana Deep is based on a large heliborne electromagnetic (HEM) anomaly that coincides with the down-dip projection of the near-surface La Romana copper/tin mineralization:

Some of the strongest copper mineralization at La Romana exhibits a similar HEM signature to the Romana Deep Target. In addition, the down plunge trend of copper mineralization at La Romana remains open in the direction of the Romana Deep target.

PGZ currently has three drill rigs turning at new targets in the Escacena Project. One rig is currently focused on Romana Deep to the north of the La Romana deposit; the second rig at the Zarcita target approximately 3 kilometers north of La Romana; and a third drill rig has begun drilling the first hole on the Cañada Honda gravity target to the southwest of Zarcita.

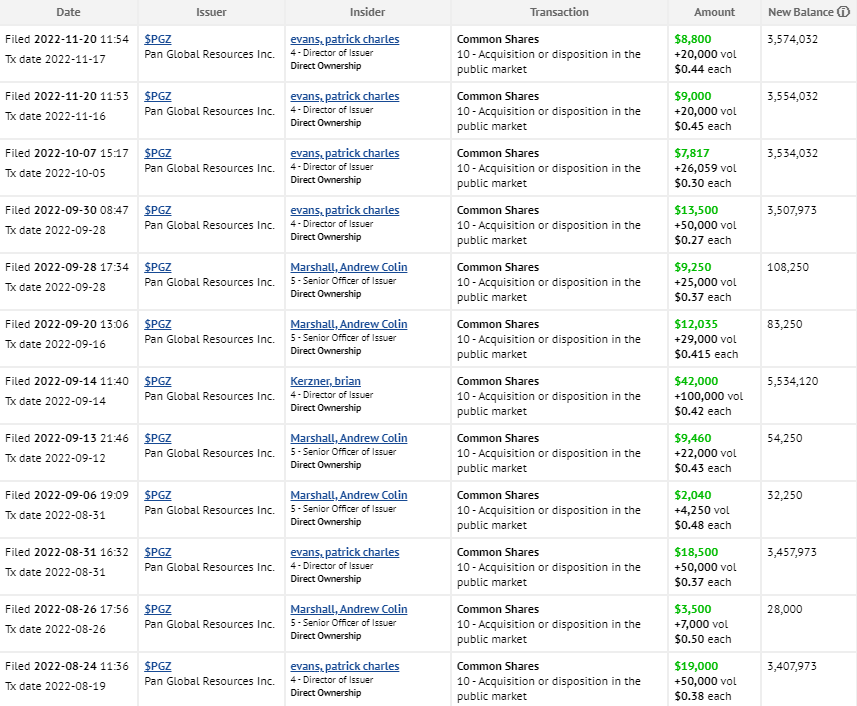

PGZ insiders have been regular buyers of the company’s shares on the open market in 2022, including at prices well above today’s $.41 share price:

Risks: More expensive deeper diamond drilling at Romana Deep could be considered riskier exploration by some investors. Moreover, exploration is an iterative process and the first hole into a new target rarely hits the motherlode. While the Iberian Pyrite Belt has a long history of mining, some resource investors prefer to avoid Spain altogether.

Share price and market cap at time of publishing: C$.41 (C$87 million market cap)

Cash Position as of 10/31/2022 = C$11.2 million

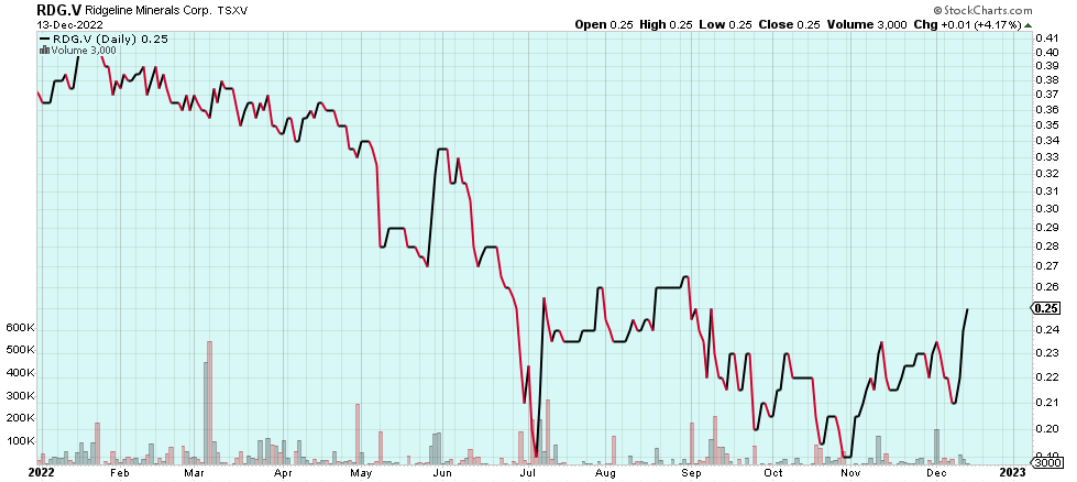

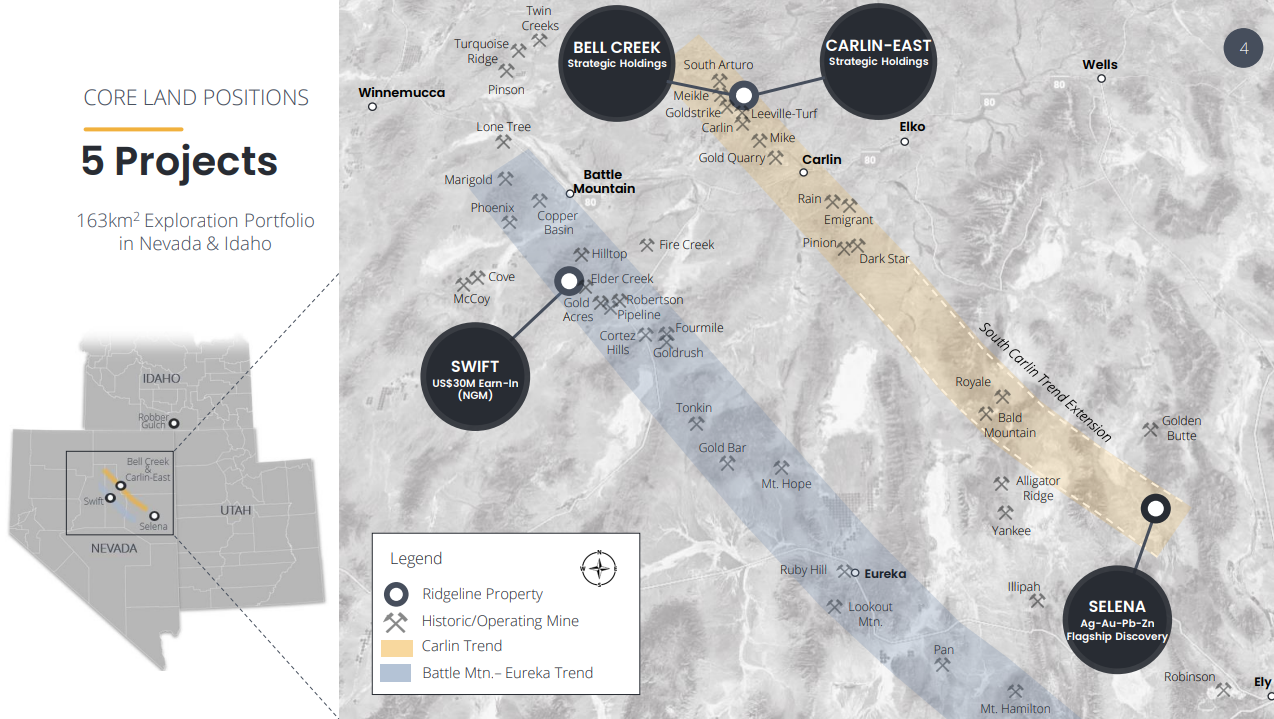

Ridgeline Minerals (TSX-V:RDG, OTC:RDGMF) – Ridgeline is a discovery focused junior exploration company with an impressive project portfolio across Nevada and Idaho. RDG shares are down ~35% in 2022, but have recently begun to show some signs of life after putting in place a potential double-bottom at C$.19:

RDG.V (Daily YTD)

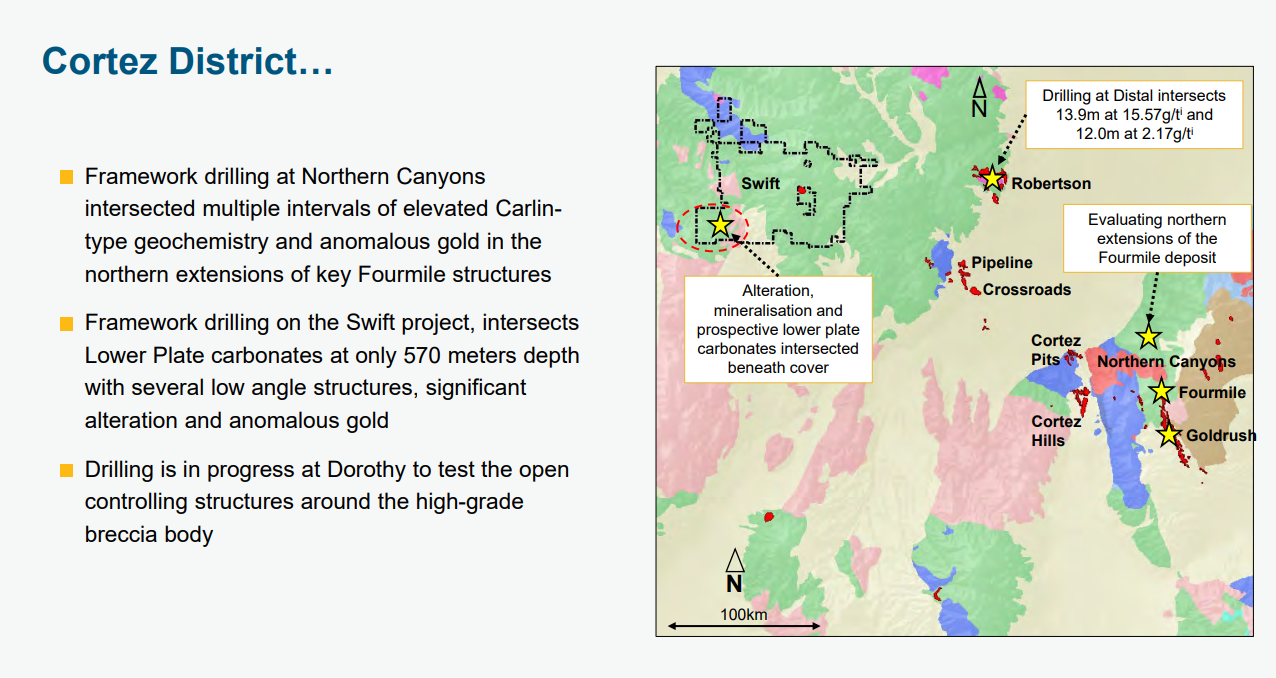

With the downturn in the gold mining sector in 2022, Ridgeline has seen its exploration model shift from RDG sole funding exploration at all projects, to selectively partnering projects in its portfolio with major gold mining companies (Example: Swift JV with Nevada Gold Mines). This shift of strategy has allowed RDG to minimize corporate dilution by diluting at the project level while still maintaining meaningful ownership in its partnered projects. This also allows Ridgeline to prioritize exploration at its 100% owned projects such as Selena (Nevada) and Robber Gulch (Idaho).

Given the state of the junior mining sector (challenging financing environment), this strategy gives Ridgeline the best opportunity to participate in a discovery without blowing out its share structure. It’s also important to note that Ridgeline CEO Chad Peters has been very selective in partnering with larger companies. So far, Peters has done well by inking an exploration earn-in agreement with Nevada Gold Mines (Barrick/Newmont Nevada partnership). NGM can incur a minimum US$20 million (US$4 million guaranteed) in qualifying work expenditures over an initial five-year term to earn an initial 60% interest in the Swift gold project.

While NGM works hard to make a discovery that would benefit Ridgeline shareholders, RDG just completed a drill program at its 100% owned Selena Project. Selena drill results are expected to be received beginning in January and I am particularly intrigued by some of the breccia mineralization that Ridgeline has encountered at its Broken Egg Target (Selena).

Risks: The biggest risk for Ridgeline is financing risk. Drilling in Nevada can be expensive and dilution can happen fast when a relatively small company tries to drill multiple projects at the same time. Ridgeline investors are betting that CEO Chad Peters will be a good steward of shareholder capital while carefully deploying drilling dollars.

Share price and market cap at time of publishing: C$.24 (C$16 million market cap)

Cash Position as of 9/30/2022 = C$2.8 million

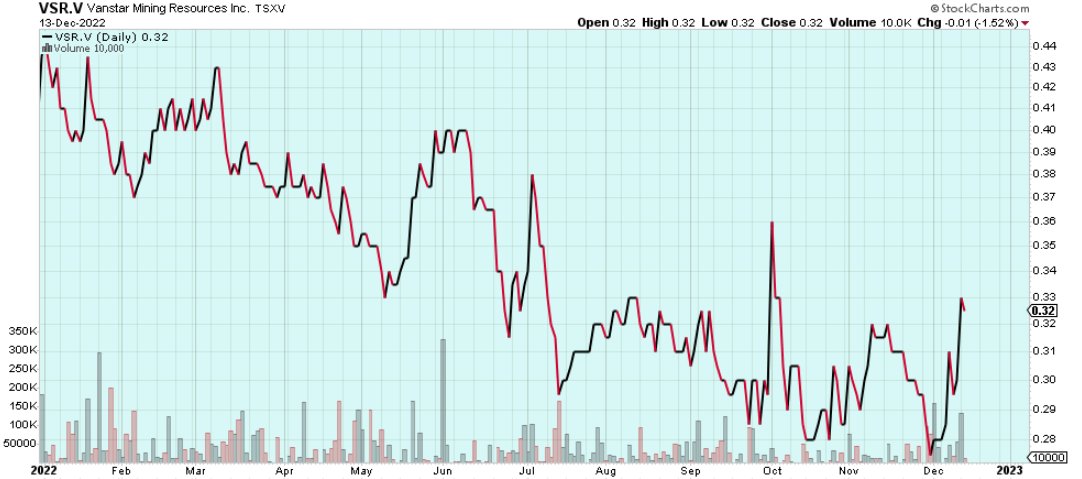

Vanstar Mining Resources (TSX-V: VSR, OTC:VMNGF) – Vanstar shares are down ~25% in 2022, a fairly modest decline for a gold junior this year.

VSR.V (Daily – YTD)

Vanstar is in a unique position for a junior mining company due to its 25% non-contributory carried interest on the multi-million ounce Nelligan Gold Project in Quebec. IAMGOLD (NYSE:IAG) is an NYSE listed mid-tier gold producer that holds the majority interest (75% with option to earn up to 80% once a feasibility study is completed) in the Nelligan Project.

Nelligan is an intrusion-related gold project that boasts 3.2 million ounces (inferred) at an average grade of 1.02 g/t gold. IAG produced the maiden resource for Nelligan in 2019, and drilling in 2020 and 2021 has continued to expand the mineralized zones along strike to the west and at depth. IAG is expected to release an updated resource estimate including infill drilling from 2020/2021, as well as resource expansion drilling that has been completed since the 2019 MRE (drilling in 2020 and 2021 extended the deposit at least 700 meters beyond the constraints of 2019 MRE).

IAG is expected to produce a resource update for Nelligan by the end of the year. This resource update along with 2023 exploration plans at Nelligan could prove to be a significant catalyst for Vanstar. As it stands now VSR’s C$18 million market cap doesn’t seem to adequately value the company’s interest in a multi-million gold deposit in a tier-1 jurisdiction.

Risks: The main risk for Vanstar continues to be the speed with which IAG advances the project. IAG’s main focus is the construction of its Côté Gold Project in northeastern Ontario. Nelligan is thought to be next in line after Côté. If the construction and ramp up at Côté runs over budget and beyond timeline estimates it could negatively affect progress and value creation at Nelligan.

Share price and market cap at time of publishing: C$.32 (C$18.5 million market cap)

Cash position of 9/30/2022 = $2.8 million

Conclusion

I would not be surprised if at least one stock on this list delivered multibagger returns in 2023 (200%+), and I would also not be surprised if a couple of the stocks on this list did not perform well (-50% or more) in 2023. That means one should expect plenty of volatility and opportunities to ‘buy low and sell high’. It’s important to understand that junior mining shares regularly experience enormous swings in valuations and one should never risk money that one cannot afford to lose. This sector is highly cyclical and gyrates from being in favor, to being terribly hated by investors, and then back again.

I recently wrote a blog post stating that I believed we are close to being in the sweet spot for precious metals. If I’m right about that, the tailwinds should be particularly favorable for the companies on this year’s list.

In markets, value is usually generated by buying what others do not see much value in, and buying at relatively low price levels. I have put my money where my mouth is and I have a long position in every company on this list. In many cases the share price today is lower than the level at which I purchased shares.

Please do your own due diligence, it’s your money and your responsibility.

Disclosure: Author owns shares of all six companies on this list (Amex Exploration, Aurion Resources, Blackrock Silver, Pan Global Resources, Ridgeline Minerals, and Vanstar Mining) at the time of publishing and may choose to buy or sell at any time without notice. Author has been compensated for marketing services by Aurion Resources Ltd. and Vanstar Mining Resources Inc.

______________________________________________________________

Disclaimer:

The article is for informational purposes only and is neither a solicitation for the purchase of securities nor an offer of securities. Readers of the article are expressly cautioned to seek the advice of a registered investment advisor and other professional advisors, as applicable, regarding the appropriateness of investing in any securities or any investment strategies, including those discussed above. Blackrock Silver Corp. and other companies discussed in this article are high-risk venture stocks and not suitable for most investors. Consult company SEDAR profiles for important risk disclosures.

EnergyandGold has been compensated for marketing & promotional services by Blackrock Silver Corp. so some of EnergyandGold.com’s coverage could be biased. EnergyandGold.com, EnergyandGold Publishing LTD, its writers and principals are not registered investment advisors and advice you to do your own due diligence with a licensed investment advisor prior to making any investment decisions.

This article contains certain forward-looking information and forward-looking statements within the meaning of applicable securities legislation (collectively “forward-looking statements”). Certain information contained herein constitutes “forward-looking information” under Canadian securities legislation. Generally, forward-looking information can be identified by the use of forward-looking terminology such as “expects”, “believes”, “aims to”, “plans to” or “intends to” or variations of such words and phrases or statements that certain actions, events or results “will” occur. Forward-looking statements are based on the opinions and estimates of management as of the date such statements are made and they are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed by such forward-looking statements or forward-looking information, standard transaction risks; impact of the transaction on the parties; and risks relating to financings; regulatory approvals; foreign country operations and volatile share prices. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Actual results may differ materially from those currently anticipated in such statements. The views expressed in this publication and on the EnergyandGold website do not necessarily reflect the views of Energy and Gold Publishing LTD, publisher of EnergyandGold.com. Accordingly, readers should not place undue reliance on forward-looking statements and forward looking information. The Company does not undertake to update any forward-looking statements or forward-looking information that are incorporated by reference herein, except as required by applicable securities laws. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SEDAR.com for important risk disclosures. It’s your money and your responsibility.