An ongoing global energy crisis has created the pressing need for a zero-carbon fuel source with enough power and reliability to transition the world to renewable energy. Now, we have an environment in which nuclear energy is being viewed in a positive light. In 2022, we have witnessed a perfect storm that is highly favorable for a significant increase in global uranium demand:

- The EU included nuclear in Sustainable Finance Taxonomy

- A slew of nuclear power plant restart announcements combined with new builds and existing nuclear power plant life extensions means increased short term, medium term, and long term demand for uranium.

- Russia’s invasion of Ukraine has highlighted the importance of weaning the world off of fossil fuels and creating domestic energy security.

- Russia is one of the world’s largest exporters of uranium and nuclear fuel, which puts that supply in jeopardy of being removed from western markets.

- Countries that have decided to U-turn on nuclear energy and keep nuclear power plants operating include: South Korea, Japan, Belgium, Sweden, and Germany.

- The world is also beginning to realize the benefits of advanced nuclear technologies like Small Modular Reactors (SMR), and plans are underway in parts of the world to convert coal plants to new nuclear facilities. These new SMR’s could result in a major increase in uranium demand.

The International Energy Agency (IEA) recently stated that nuclear energy is set for a big comeback, a “clear” and “strong” comeback to be precise. The IEA report also stated that if the global energy transition to renewable energy sources proceeds with a precipitous decline in nuclear power generation, from 10% of global output to 3% by 2050, the energy transition will be more challenging, more risky and $500 billion more expensive. The IEA warned that any true nuclear buildout will require the industry to lower reactor construction costs by 40%, and for governments to develop frameworks that “facilitate investment” in nuclear power.

Putting it all together, the future is bright for nuclear energy. As a result, the uranium mining sector is in the midst of a renaissance of sorts. The keystone stock of the uranium mining sector, Cameco (NYSE:CCJ, TSX:CCO), has benefited from a surge of interest in the sector. And earlier this month, Cameco doubled down by expanding its commitment to the nuclear energy industry by announcing a strategic partnership with Brookfield Renewable Partners to acquire Westinghouse Electric for US$7.88 billion. This deal serves to vertically integrate Cameco in the nuclear power plant servicing business, in addition to its existing nuclear fuel and uranium mining businesses.

The fact that a private equity group like Brookfield is making a multi-billion dollar investment in the nuclear energy industry is a strong sign that the nuclear energy renaissance is still in its early days. In the next phase of this nuclear renaissance, we will likely see increased consolidation in the uranium mining industry with large firms snapping up the best development/exploration stage assets in the best jurisdictions.

To be clear, the nuclear energy industry is set for a multi-decade renaissance that will trickle down across all verticals in the industry. This brings me to the source of nuclear fuel, the uranium mining sector. More specifically, the uranium exploration sector.

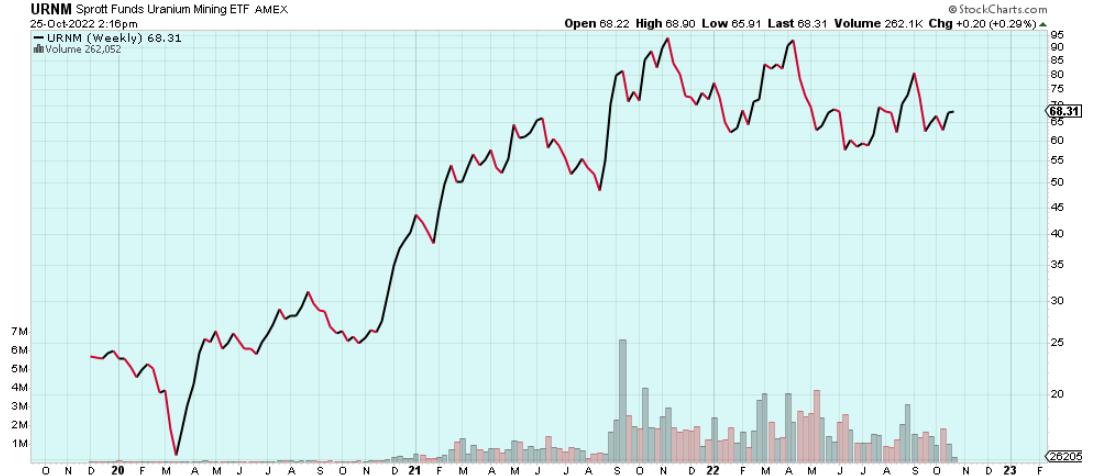

The uranium exploration sector had a powerful bull run from the March 2020 covid lows through its peak in November 2021, which was a 20-month run the sector hasn’t seen since the 2006/2007 bull market:

URNM Sprott Funds Uranium Mining ETF (Weekly Since Inception)

The Sprott Funds Uranium Mining ETF rose more than 500% from the March 2020 low to the November 2021 peak. Since November 2021, the fund is down about 30%, but many individual uranium explorers are down 40%-50% over the same time frame.

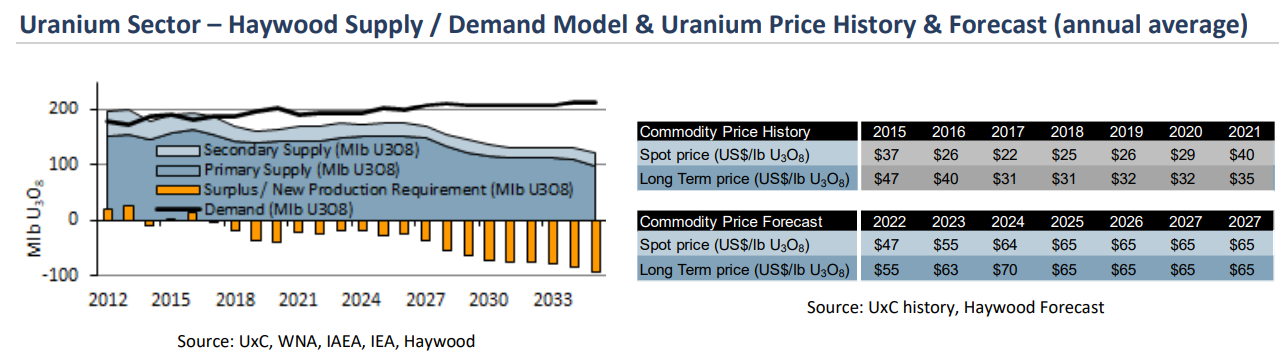

Because of this, the uranium sector is in the midst of significant bull market correction at a time when the world is increasingly open to nuclear energy fueling the energy transition for the next several decades. According to five different analyst groups (UxC, WNA, Haywood, IAEA, IEA), the uranium market is currently undersupplied, and that supply/demand gap is set to increase significantly over the next decade:

The world needs more uranium to be extracted from the Earth, and the only way to do that is to build more mines and make more economic uranium discoveries. This creates a fertile environment for companies with highly prospective projects in good jurisdictions.

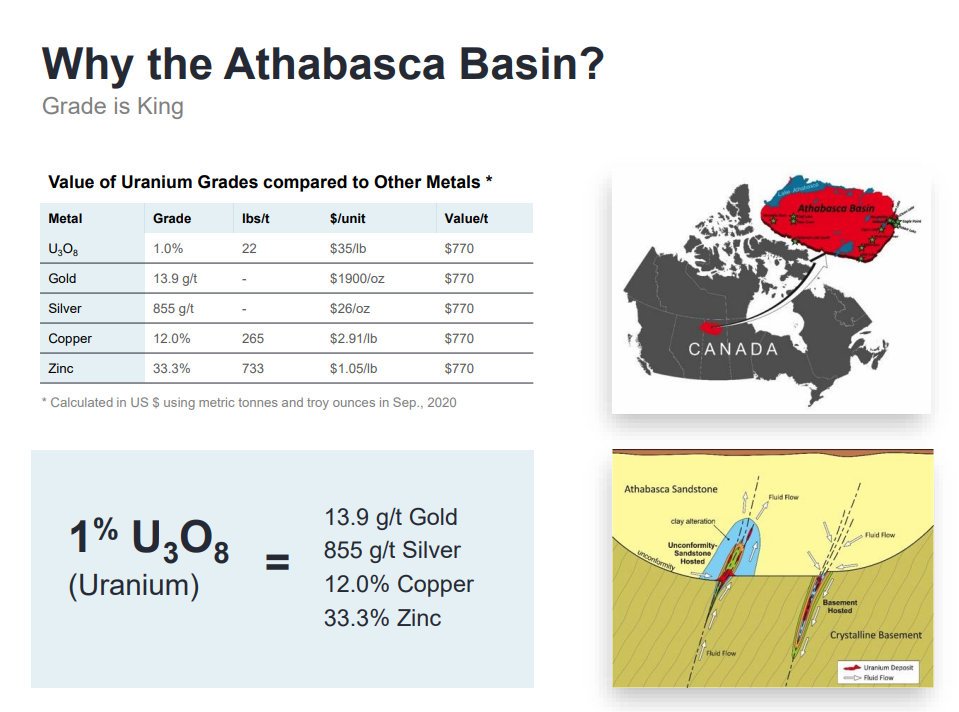

There is no better jurisdiction for uranium exploration than Saskatchewan, ranked as a top 3 mining jurisdiction globally by the Fraser Institute. Saskatchewan is also home to Cameco’s corporate headquarters and largest mines (Athabasca Basin), as well as NexGen Energy’s Arrow Deposit. NexGen’s Arrow Deposit is the premier development stage uranium asset in the world with a resource totaling more than 600 million pounds U3O8 in all categories, grading an average of more than 3% U3O8.

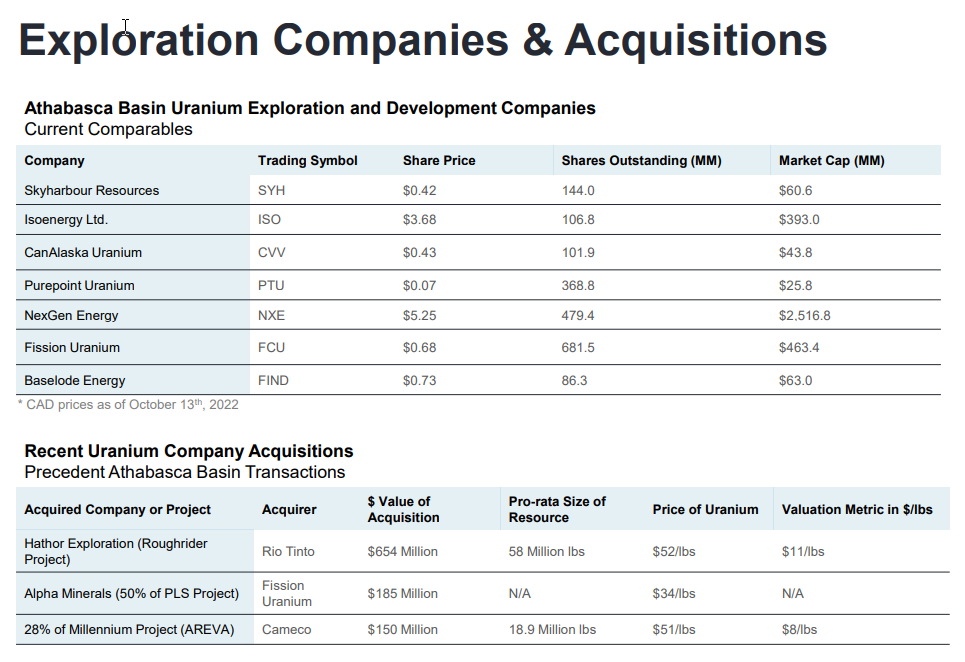

NXE’s US$2.5 billion market cap is an example of what kind of valuations are possible when a company delivers unprecedented exploration success in a tier-1 jurisdiction. Arrow is a unique ore body with average grades that have never been seen before across such a large area. Twenty years ago, many people thought that there would never be another major uranium discovery in the Athabasca Basin. Both Hathor Exploration and NexGen quickly proved the naysayers wrong by making major discoveries during the 2009-2015 time frame. I find it especially notable that the major discovery period for Arrow was 2014/2015, both terrible years for the uranium and junior mining sectors.

Skyharbour Resources (TSX-V:SYH, OTC:SYHBF) is a high-grade uranium explorer that also uses the project generator model to acquire and advance a large portfolio of prospective uranium assets in Saskatchewan. Skyharbour is committed to making one of the next major uranium discoveries in Saskatchewan. In addition to focused exploration of its core projects, the company utilizes the project generator model to more effectively share in the upside potential of numerous exploration projects while keeping expenses at a reasonable level for a company of its size (~US$50 million market cap).

Skyharbour has a strong shareholder base that includes significant institutional backing. SYH is also a component of the two most liquid uranium focused ETFs, URA and URNM:

Skyharbour is focused on the Athabasca Basin due to its prolific endowment of high-grade uranium deposits and the fact that it is one of the best mining jurisdictions to operate globally.

Skyharbour is in good company in the Athabasca, as one can see the market cap potential for companies that are able to make significant discoveries in this premier uranium jurisdiction:

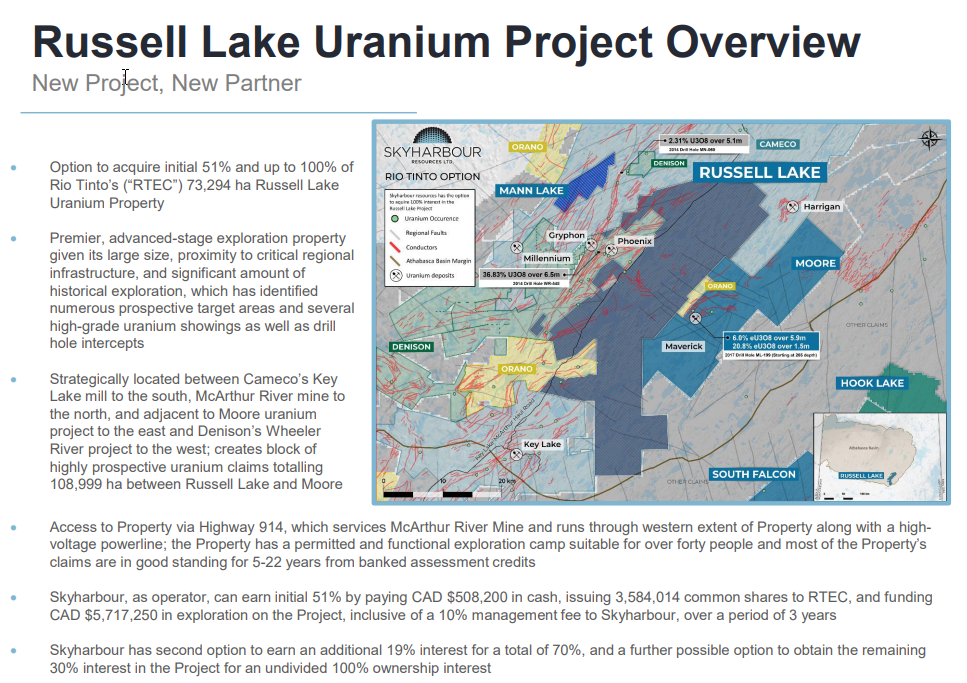

Skyharbour holds a portfolio of 15 projects in the Athabasca, of which there is or will be active drilling on six (Skyharbour’s Russell Lake and Moore; partner funded projects East Preston, Hook Lake, Mann Lake and Yurchison). Of Skyharbour’s 100% owned projects (including options to acquire 100%), both Moore and Russell Lake boast very high-grade uranium intercepts with grades north of 3% U3O8 in previous drill holes.

The Russell Lake Project is particularly interesting because Skyharbour was recently able to option the project from mining giant Rio Tinto. The option agreement gives Skyharbour the option to acquire an initial 51% interest in Russell Lake with the ability to earn 100% of the 73,294 hectare Russell Lake Uranium Property. Russell Lake is a large, advanced-stage uranium exploration property that has had a meaningful amount of historical exploration carried out on the project, but with most of it conducted prior to 2010.

Russell Lake will be Skyharbour’s main focus over the next year with a substantial drill program currently being planned. Details for Skyharbour’s maiden drill program at Russell Lake will be released shortly, and I expect this to be a noteworthy winter drill program at a highly prospective Athabasca Basin uranium project:

Russell Lake’s strategic location is a huge positive for Skyharbour; it is adjacent to Skyharbour’s Moore Lake Project to the east, and sandwiched between Cameco’s Key Lake Mill and McArthur River Mine (the largest producing uranium mine in the world).

This is a rough timeline of key news flow that investors can expect from Skyharbour over the next 12 months:

- Basin Uranium is currently completing a 3,000 – 4,000 meter program at Mann Lake (phase 2).

- Azincourt is planning 6,000 meter of drilling starting in December at East Preston.

- Valor is planning another phase of drilling in the new year at Hook Lake

- Medaro is planning its first phase of drilling in the new year at Yurchison

- Recently announced option partners Yellow Rocks Energy and Tisdale Clean Energy will be working at the Usam/Wallee and South Falcon East Projects; drilling is expected in 2023 at South Falcon East

- Skyharbour is funded for 10,000 meters of drilling over the next 12 months most of which will be at Russell Lake and a small amount at Moore

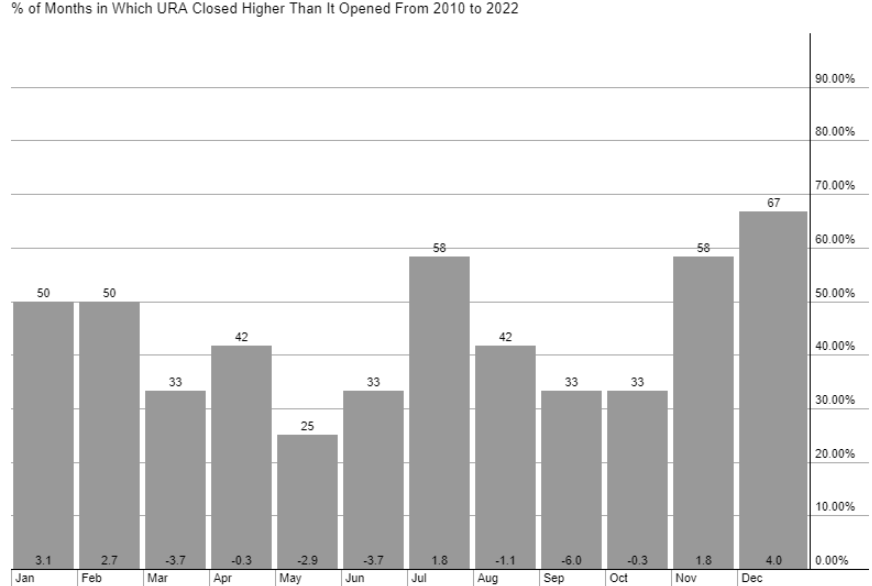

I view Skyharbour to be an attractive way to express a bullish long term view of the nuclear energy industry and the price of uranium. Skyharbour offers many ways to achieve exploration upside through its extensive Athabasca Basin portfolio. SYH shares also benefit from uranium sector flows due to its role as a component of both the URNM and URA uranium ETFs. I have added SYH.V shares to my portfolio in recent weeks, and I look forward to the details of the drilling program at Russell Lake. Not to mention the bullish year end seasonality for the uranium sector (the URA has generated an average return of 6% during November/December since its inception in 2010):

Disclosure: Author owns SYH.V shares at the time of publishing and may choose to buy or sell at any time without notice.

______________________________________________________________________________________

Disclaimer:

The article is for informational purposes only and is neither a solicitation for the purchase of securities nor an offer of securities. Readers of the article are expressly cautioned to seek the advice of a registered investment advisor and other professional advisors, as applicable, regarding the appropriateness of investing in any securities or any investment strategies, including those discussed above. Skyharbour Resources Ltd. is a high-risk venture stock and not suitable for most investors. Consult Skyharbour Resources Ltd.’s SEDAR profile for important risk disclosures.

EnergyandGold has been compensated for marketing & promotional services by Skyharbour Resources Ltd. so some of EnergyandGold.com’s coverage could be biased. EnergyandGold.com, EnergyandGold Publishing LTD, its writers and principals are not registered investment advisors and advice you to do your own due diligence with a licensed investment advisor prior to making any investment decisions.

This article contains certain forward-looking information and forward-looking statements within the meaning of applicable securities legislation (collectively “forward-looking statements”). Certain information contained herein constitutes “forward-looking information” under Canadian securities legislation. Generally, forward-looking information can be identified by the use of forward-looking terminology such as “expects”, “believes”, “aims to”, “plans to” or “intends to” or variations of such words and phrases or statements that certain actions, events or results “will” occur. Forward-looking statements are based on the opinions and estimates of management as of the date such statements are made and they are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed by such forward-looking statements or forward-looking information, standard transaction risks; impact of the transaction on the parties; and risks relating to financings; regulatory approvals; foreign country operations and volatile share prices. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Actual results may differ materially from those currently anticipated in such statements. The views expressed in this publication and on the EnergyandGold website do not necessarily reflect the views of Energy and Gold Publishing LTD, publisher of EnergyandGold.com. Accordingly, readers should not place undue reliance on forward-looking statements and forward looking information. The Company does not undertake to update any forward-looking statements or forward-looking information that are incorporated by reference herein, except as required by applicable securities laws. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SEDAR.com for important risk disclosures. It’s your money and your responsibility.