One of the best and biggest junior mining deals of the last couple of years was First Cobalt’s C$149 million acquisition of U.S. Cobalt. U.S. Cobalt was originally a company called Scientific Metals which started with humble beginnings and a C$.03 share price in early 2016, two years later the stock would trade above C$1.30 giving early investors a 4300% return on their investment (Energy & Gold began following Scientific Metals in mid-2016 and covered the story all the way through acquisition in early 2018). It doesn’t get much better than that!

The man at the helm of U.S Cobalt was Wayne Tisdale, a man who has a track record of generating significant value for shareholders through accretive transactions and timing market cycles as well as anyone. Mr. Tisdale has been instrumental in founding several highly successful companies, including Rainy River Resources (purchased by Newgold) and Ryland Oil Corporation (purchased by Crescent Point). He has also raised more than $2 billion of equity and debt financing throughout the course of his career.

Mr. Tisdale has a passion for the resource exploration business and he simply enjoys finding and putting together attractive projects and then advancing them to a stage where they will be bought by a larger mining company. With the electric vehicle revolution in full swing Tisdale decided to form 21C Metals (CSE:BULL) an exploration company focused on the acquisition and development of deposits of production grade metal which are critical components to current and future vehicle technology. Cobalt, copper, and palladium are all strategic metals that are experiencing supply deficits that are poised to get worse over the next decade.

With an eye towards finding highly prospective cobalt, copper, and palladium projects It didn’t take Tisdale long after U.S. Cobalt was acquired to come up with his next project idea. Through a Czech prospector friend named Otto Janout, Tisdale came across a project called the Tisova Project in the Czech Republic.

The Tisova Project has an interesting story behind it that dates to the 1300s when there was mining for copper. In 1898 miners built a headframe and some adits for underground mining. However, all mining operations ceased shortly before World War I and did not resume again until the Soviet Union controlled Czechoslovakia and East Germany. Under the Czech state mining company limited mining operations were carried out which only extracted 500,000 tonnes of ore. Tisova then sat until 1994 when it was formally shuttered (bars over the entrances to underground adits).

The Tisova project is located on the Czech/German border hosted by the Kraslice Sequence, a Cambrian-age continental rift of sediments and volcanics. There is a long history of mining in the area, making the logistics for exploration straightforward. In addition, the regulatory environment has a long established regime, which makes permitting straightforward. Tisova hadn’t had any modern scientific work done on it until this year when Tisdale got a hold of the project and gave his head geo a hefty budget in order to decide if this was a project that was worth spending some real money on.

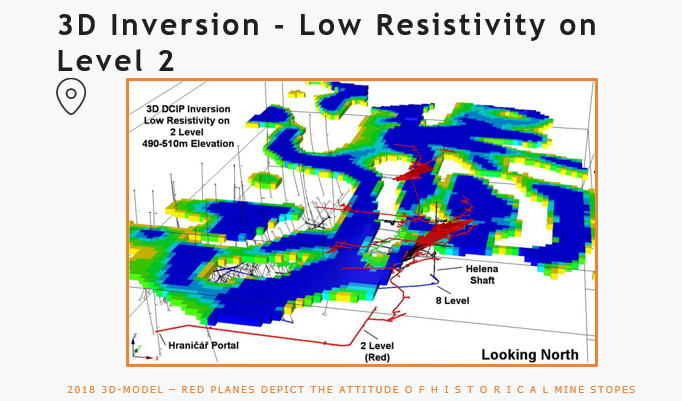

21C’s geologists were able to determine that Tisova is a VMS system (Volcanogenic massive sulfide ore deposit) that has been tentatively identified as existing over 1.9 kilometers down dip and 2.0 kilometers along strike. Within the Kraslice Sequence, discrete copper/cobalt bearing VMS horizons appear to occur within a 100 meter thick assemblage termed the Tisova Horizon. 21C Metal’s geologists, working with recognized world experts in VMS deposits, have developed a preliminary exploration signature for copper/cobalt on the property. 21C also ran a 3D IP (induced polarization) geophysical survey across the entire property and it “lit up like a christmas tree” according to 21C President and Founder Wayne Tisdale.

It is currently thought that there may be be as much as a prospective 32 km belt with copper-cobalt-gold mineralization occurring in pods that contain between 300,000 and 500,000 tonnes of high-grade ore. Tisdale explained that early miners mined these pods, that were roughly the size of cathedrals, in stopes.

The last mining at Tisova occurred in 1973 when then Czechoslovakia was under Soviet rule. The mine was shuttered and nothing happened with the project for several decades until Czech prospector Otto Janout was able to put the Tisova Project claims package together into one property.

While mining ended in 1973, exploration and underground development (access drives for underground drilling) continued for a further 10 years via continued underground development from between 200 meters to 400 meters below surface. Tisova boasts over 30 kilometers of underground mine development in the footwall of the sulphide blanket which gives any future operator a tremendous amount of value-added infrastructure that is already in place.

An Australian explorer called Auroch Minerals took over the Tisova project beginning in 2016 and moved slowly before completing a limited four hole drilling program in late 2017. Auroch chose to not renew their option on the project after reviewing the assays for the four holes it had drilled. Auroch’s drilling at Tisova missed the thicker sections because they drilled off the key trends after a cursory review of historical data. Auroch even drilled into the underground workings at Tisova, and before choosing to not renew the option on the project Auroch Chairman Glenn Whiddon added the following:

“…analysis of the drill core versus the previous grab samples suggest a different origin for the two sets of samples within the large Tisová deposit. We believe this to be a logical explanation for the drilling results based upon the historical mining, dating back to 1600’s. This implies that there remains a cobalt rich portion of the orebody that was not tested by our initial four drill holes and further investigation is warranted.“

Tisova was a non-core project for Auroch and the company chose to focus its attention and all of its resources on its South Australia projects. Auroch’s decision to walk away from Tisova opened a window of opportunity for 21C founder and CEO Wayne Tisdale, at a time when Mr. Tisdale was looking for the next project with big opportunity. 21C has integrated Auroch’s data with all of the other historical data and it has served to increase 21C’s confidence in the prospectivity of Tisova. 21C believes it knows exactly where to drill in order to find copper-cobalt-gold mineralization that was never exploited by historic mining activity. 21C will begin drilling at Tisova in May and the first assays could start to come back as early as mid-June.

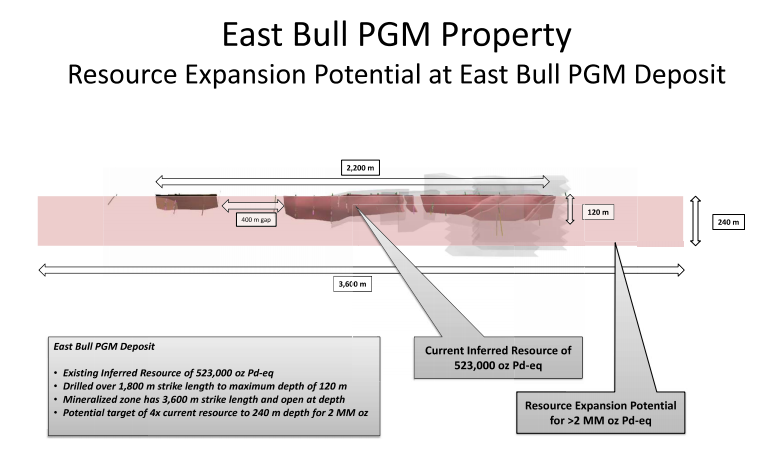

21C’s other project, The East Bull Palladium Project, is located in Ontario, Canada not far from the famous platinum group metals haven, Sudbury. East Bull boasts a 43-101 compliant resource estimate of 11.1 million tonnes of ore at a grade of 1.46g/t palladium-equivalent for a total of 523,000 ounces of Palladium. Due to low palladium prices and challenges in putting together all the claims into one property package, East Bull was never advanced to the development/production stages.

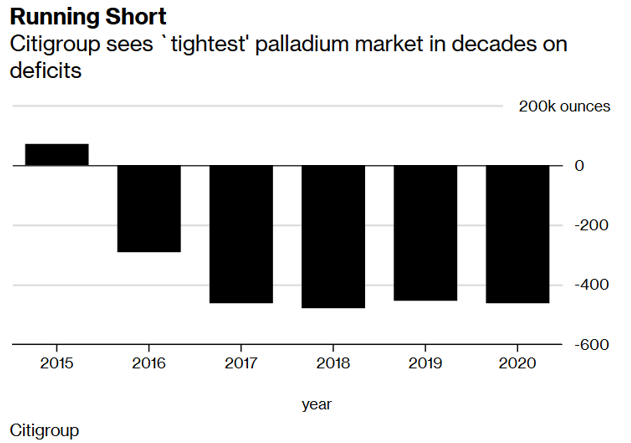

Fade the scene to May 2019 and palladium is trading north of US$1,400 per ounce and the white metal is in a supply deficit for the fourth consecutive year:

The outlook for palladium looks better than ever due to tight supply with a limited number of sources globally (90% of palladium production comes from Russia and South Africa). While many make a big deal of the electric vehicle revolution, it’s important to remember that even by 2030 the vast majority of vehicles on the road will either still be internal-combustion engines (ICE) or hybrids (cars that have both ICE or EV option):

This means that global demand for palladium isn’t going to fall anytime soon. In fact, it is likely to actually increase along with automobile production and global population growth.

Given that so much palladium comes from South Africa and Russia, secure sources of palladium production in North America are in high demand. The East Bull PGM (platinum group metals) Project couldn’t be in a better location with abundant infrastructure and roads throughout the area. East Bull is located in Gerow Township, Ontario, Canada which is about 90 km west of Sudbury, Ontario (home to some of the world’s largest platinum group metals mines).

The East Bull Project boasts the following attributes:

-

Defined platinum group metals (PGM) resources with targets for discovery and expansion.

-

Property covers highly prospective portion of East Bull southern marginal series with a 3.6 kilometer trend of mineralized inclusion-bearing zone (IBZ) with associated VTEM anomalies and total magnetic field derivative high.

-

43-101 compliant inferred resource estimate (11.1 million tonnes of ore at a grade of 1.46g/t PdEq for a total of 523,000 ounces of palladium) with significant upside potential.

-

Excellent location with good logistics and infrastructure.

-

Benefits from tested recent drilling, trenching and geophysical data.

-

Permits in place – exploration can start immediately.

Location and infrastructure is absolutely critical in terms of advancing an economic mineral resource. East Bull benefits from a virtually ideal location in an area of Canada that has a long history of mining. Moreover, easy road access and close proximity to supporting infrastructure such as assay labs and lower cost labor make East Bull an attractive project to advance against the backdrop of a palladium bull market.

East Bull has considerable room for resource expansion at depth (historical drilling reached a maximum depth of 120 meters) and several gaps over 3,600 meters in strike length that can be filled in with new drilling:

As one junior mining insider told me last week “21C has the sort of projects that will draw interest from majors if they’re able to score some hits with the drill”. I agree. Location is a big part of the equation in terms of advancing a resource to production and both Tisova and East Bull are ideally located near population centers and infrastructure. The best part for 21C shareholders is that only one of these projects needs to be a success in order to see 21C shares reach multiples of the current share price.

Disclosure: Author is long shares of 21Metals Inc. at the time of publishing and may buy or sell at any time without notice.

Disclaimer:

The article is for informational purposes only and is neither a solicitation for the purchase of securities nor an offer of securities. Readers of the article are expressly cautioned to seek the advice of a registered investment advisor and other professional advisors, as applicable, regarding the appropriateness of investing in any securities or any investment strategies, including those discussed above. 21C Metals Inc. is a high-risk venture stock and not suitable for most investors. Consult 21C Metals Inc.’s SEDAR profile for important risk disclosures.

EnergyandGold has been compensated for marketing & promotional services by 21C Metals Inc. so some of EnergyandGold.com’s coverage could be biased. EnergyandGold.com, EnergyandGold Publishing LTD, its writers and principals are not registered investment advisors and advice you to do your own due diligence with a licensed investment advisor prior to making any investment decisions.

This article contains certain forward-looking information and forward-looking statements within the meaning of applicable securities legislation (collectively “forward-looking statements”). Certain information contained herein constitutes “forward-looking information” under Canadian securities legislation. Generally, forward-looking information can be identified by the use of forward-looking terminology such as “expects”, “believes”, “aims to”, “plans to” or “intends to” or variations of such words and phrases or statements that certain actions, events or results “will” occur. Forward-looking statements are based on the opinions and estimates of management as of the date such statements are made and they are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed by such forward-looking statements or forward-looking information, standard transaction risks; impact of the transaction on the parties; and risks relating to financings; regulatory approvals; foreign country operations and volatile share prices. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Actual results may differ materially from those currently anticipated in such statements. The views expressed in this publication and on the EnergyandGold website do not necessarily reflect the views of Energy and Gold Publishing LTD, publisher of EnergyandGold.com. Accordingly, readers should not place undue reliance on forward-looking statements and forward looking information. The Company does not undertake to update any forward-looking statements or forward-looking information that are incorporated by reference herein, except as required by applicable securities laws. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SEDAR.com for important risk disclosures. It’s your money and your responsibility.