Nevada is home to some of the world’s richest mineral resources. However, when you think of Nevada you probably think of gold, not lithium. Well it might be time to think again – Cypress Development just released a maiden resource estimate at its Clayton Valley, Nevada lithium project that will put Nevada on the map for lithium for a long time to come.

This resource estimate stands out because it shows a total mineral resource of 6.4 million tonnes of lithium carbonate equivalent (LCE) grading nearly 900 ppm Li (parts per million lithium). This is a large, high grade lithium resource located in one of the best jurisdictions and geographic locations that a lithium resource could possibly be located. To put the size of Cypress Development’s Clayton Valley Project into perspective, using a US$11,000/tonne LCE price and an 80% recovery (as outlined in the CYP resource estimate) the total market value of the total amount of lithium defined in Cypress’ resource estimate is more than US$56 billion. While there will be many factors that will greatly reduce the net present value of that figure, it’s still a tremendously valuable resource for a company that currently has a C$20 million market cap.

Another aspect that many investors might be overlooking is that Cypress has favorable mineralogy which means that conventional recovery methods can produce high-purity lithium carbonate. Additional leach testing is currently being conducted by Hazen Research Inc, and preliminary results have confirmed high lithium extractions for new mineral zones. Because the Clayton Valley claystones at Cypress’ Project are amenable to conventional recovery methods, Cypress may be able to fast-track production without having to do a pilot plant – this potential shortcut will save Cypress millions of dollars and up to 24 months of construction and project development time.

The situation is fairly straightforward as Cypress begins to move towards its maiden PEA before the end of the year:

-

More metallurgy testing with updates throughout the summer.

-

Prepare maiden PEA with objective of publishing PEA during Q4 2018.

-

Infill drilling to upgrade the inferred portion (3.683 million tonnes) of the resource to the indicated category – Cypress believes that it can upgrade the inferred portion to the indicated category with 30 additional drill holes.

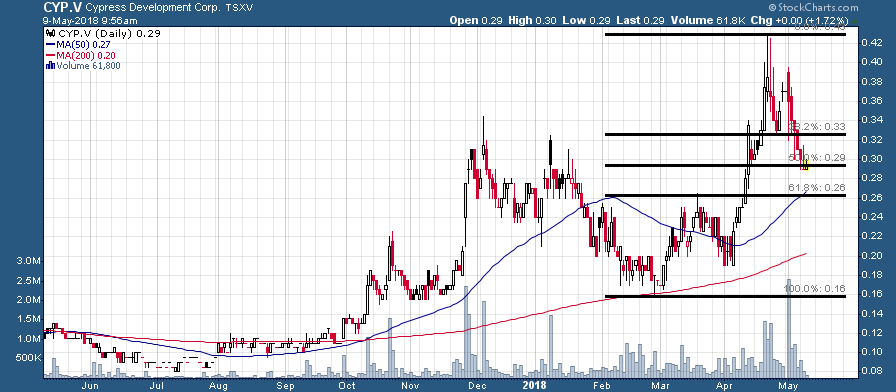

At its recent share price of C$.30 Cypress has a C$17.5 million market cap – CYP’s current market cap is 1/10th of lithium development peer Bacanora Minerals (TSX-V:BCN), which has a C$187 million market cap. Bacanora’s clay-held lithium project is at the BFS stage (bankable feasibility study) and it is slightly larger than CYP’s project, however, the valuation gap is simply enormous. Cypress is in a superior location/jurisdiction (Nevada) compared to Bacanora’s project (Mexico) and CYP shareholders can look forward to CYP shares bridging the current valuation gap as the company advances towards the BFS stage over the next year (it’s quite possible that Cypress could be in the bankable feasibility stage by the 2nd half of 2019). Proving the value of the project’s mineralogy will be a huge step towards producing a positive PEA with compelling project economics. Buying near C$.30 (previous resistance and 50% retracement of February-April rally) following the “selling on the news” after the resource estimate announcement might be an attractive entry point as Cypress embarks upon what could be the most critical year and a half in the company’s history:

CYP.V (1 Year)

Disclosure: Author is long CYP shares at time of publishing and may buy or sell at any time without notice. Do your own due diligence, it’s your money and your responsibility.

Disclaimer:

The article is for informational purposes only and is neither a solicitation for the purchase of securities nor an offer of securities. Readers of the article are expressly cautioned to seek the advice of a registered investment advisor and other professional advisors, as applicable, regarding the appropriateness of investing in any securities or any investment strategies, including those discussed above. Cypress Development Corp is a high-risk venture stock and not suitable for most investors. Consult Cypress Development Corp’s SEDAR profile for important risk disclosures.

EnergyandGold has been compensated for marketing & promotional services by Cypress Development Corp so some of EnergyandGold.com’s coverage could be biased. EnergyandGold.com, EnergyandGold Publishing LTD, its writers and principals are not registered investment advisors and advice you to do your own due diligence with a licensed investment advisor prior to making any investment decisions.

This article contains certain forward-looking information and forward-looking statements within the meaning of applicable securities legislation (collectively “forward-looking statements”). Certain information contained herein constitutes “forward-looking information” under Canadian securities legislation. Generally, forward-looking information can be identified by the use of forward-looking terminology such as “expects”, “believes”, “aims to”, “plans to” or “intends to” or variations of such words and phrases or statements that certain actions, events or results “will” occur. Forward-looking statements are based on the opinions and estimates of management as of the date such statements are made and they are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed by such forward-looking statements or forward-looking information, standard transaction risks; impact of the transaction on the parties; and risks relating to financings; regulatory approvals; foreign country operations and volatile share prices. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Actual results may differ materially from those currently anticipated in such statements. The views expressed in this publication and on the EnergyandGold website do not necessarily reflect the views of Energy and Gold Publishing LTD, publisher of EnergyandGold.com. Accordingly, readers should not place undue reliance on forward-looking statements and forward looking information. The Company does not undertake to update any forward-looking statements or forward-looking information that are incorporated by reference herein, except as required by applicable securities laws. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SEDAR.com for important risk disclosures. It’s your money and your responsibility.