The week after crude oil reached $26/barrel in February 2016, I had my first conversation with Allen Wilson of Jericho Oil (TSX-V:JCO, OTC:JROOF). At the time, Jericho was already several months into its strategy of acquiring high quality producing oil assets in the mid-continent region of the United States. While Allen laid out Jericho’s unique strategy for picking up oil assets that could be operated profitably at oil prices less than $30/barrel, I was wondering how they would make this strategy work as a publicly traded company (public company shareholders can be impatient and want to see quick progress). Jericho’s strategy seemed more like a private equity type of strategy, however, the company’s unique financial backing ensured that Jericho could implement this strategy patiently and effectively.

Fast forward over two years later, crude oil is back near $70/barrel and Jericho’s strategy of rolling up distressed and undercapitalized oil assets in 2015/2016 looks like a stroke of genius. However, in February 2016, with the oil industry in the steepest part of its downturn, it took a great deal of foresight and financial fortitude to be a buyer of oil producing assets. Jericho has now built a 70,000 gross acre position at an enviably low cost basis.

Jericho Oil Stock Snapshot:

Shares Outstanding – 127.1 million

Recent Share Price – C$.92

Market Cap (undiluted) – C$117 million

Warrants (C$.60 exercise price) – 25.2 million

Options – 7.7 million

Year-end 2016 2P Reserves: US$52 million

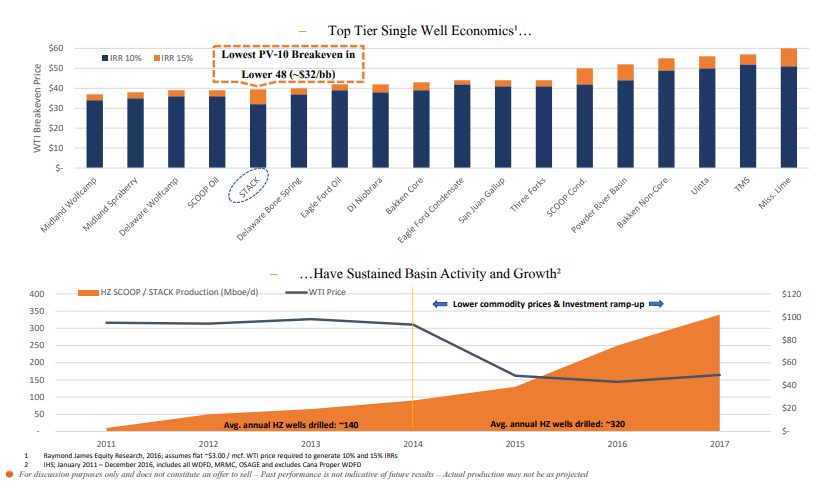

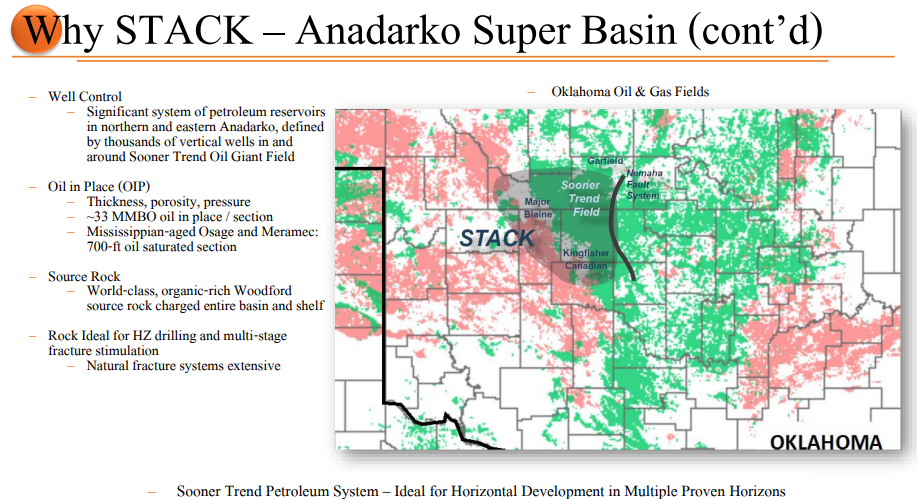

Jericho’s patient strategy came to fruition in a big way in August 2017, when the company was able to quickly close an opportune acquisition of approximately 9,400 net surface acres in the oil window of the Anadarko Basin STACK play in Oklahoma in a STACK Joint Venture (Jericho purchased an initial 31% interest a that time, with its private family partner acquiring the balance). The STACK JV paid roughly $2,300 per acre for its August 2017 acquisition, a price that may have ‘bottom-ticked’ the market (WTI was trading around $47/barrel at the time). In the last couple of months there have been several transactions in the STACK at more than $10,000 per acre (Chaparral Energy was recently pleased to close a $60 million STACK acquisition at $8,500 per acre, while Silver Run Capital’s acquisition of Alta Mesa was priced at ~$17,000 per acre).

The STACK has become a highly sought after oil producing basin with the best economics in the continental United States:

“We expect the SCOOP/STACK to provide the highest oil production CAGR for the rest of the decade among all major oil basins.” ~ Goldman Sachs

The first well Jericho’s STACK JV drilled, in partnership with Staghorn Petroleum, has brought online in the STACK play achieved a peak 24-hour rate of 957 oil-equivalent barrels per day (68% oil) at 211 Boepd per 1,000 feet – the projected 30-day normalized rate (IP30) for this 4,518 ft perforated lateral well is 770 BOE per day (67% oil).

Jericho’s STACK JV plans to now complete another 4-5 more wells in its STACK play in 2018 (with Staghorn and another top tier STACK operator). In addition, Jericho is on the hunt for “tuck-in” acquisitions which will complement its current property package. Another positive catalyst for Jericho over the coming months is an anticipated move to the “big board” (TSX listing).

The STACK shale oil play is particularly attractive due to the potential for achieving oil flow from multiple formations spanning a 700 feet thick pay area (Chester/Manning, Meramec, Osage, Woodford) from the same horizontal well; moreover, the rock is ideal for multi-stage fracture stimulation.

2018 is poised to be the year that Jericho steps onto a bigger stage after spending the last 2 ½ years building a firm foundation as a mid-continent focused oil E&P junior.

Disclaimer

The article is for informational purposes only and is neither a solicitation for the purchase of securities nor an offer of securities. Readers of the article are expressly cautioned to seek the advice of a registered investment advisor and other professional advisors, as applicable, regarding the appropriateness of investing in any securities or any investment strategies, including those discussed above. Jericho Oil Corp. is a high-risk venture stock and not suitable for most investors.. Consult Jericho Oil Corp’s SEDAR profile for important risk disclosures.

EnergyandGold has been compensated to cover Jericho Oil Corp. and so some information may be biased. EnergyandGold.com, EnergyandGold Publishing LTD, its writers and principals are not registered investment advisors and advice you to do your own due diligence with a licensed investment advisor prior to making any investment decisions.

This article contains certain forward-looking information and forward-looking statements within the meaning of applicable securities legislation (collectively “forward-looking statements”). Certain information contained herein constitutes “forward-looking information” under Canadian securities legislation. Generally, forward-looking information can be identified by the use of forward-looking terminology such as “expects”, “believes”, “aims to”, “plans to” or “intends to” or variations of such words and phrases or statements that certain actions, events or results “will” occur. Forward-looking statements are based on the opinions and estimates of management as of the date such statements are made and they are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed by such forward-looking statements or forward-looking information, standard transaction risks; impact of the transaction on the parties; and risks relating to financings; regulatory approvals; foreign country operations and volatile share prices. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Actual results may differ materially from those currently anticipated in such statements. The views expressed in this publication and on the EnergyandGold website do not necessarily reflect the views of Energy and Gold Publishing LTD, publisher of EnergyandGold.com. Accordingly, readers should not place undue reliance on forward-looking statements and forward looking information. The Company does not undertake to update any forward-looking statements or forward-looking information that are incorporated by reference herein, except as required by applicable securities laws. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SEDAR.com for important risk disclosures. It’s your money and your responsibility.