In the murky junior resource sector in which missed timelines are the norm and disappointments are abundant, it is refreshing when a company exceeds expectations and advances a project rapidly. Such is the case with Fireweed Zinc (TSX-V:FWZ), a Yukon zinc resource developer that has rapidly advanced its Macmillan Pass Zinc Project (comprised of the ‘Tom’ and ‘Jason’ deposits) since its shares began trading on the TSX-Venture last June.

Under the leadership of CEO Brandon Macdonald, Fireweed conducted a highly successful 2017 drill program that served to outline a larger resource than the market had previously anticipated. The company rapidly moved to release an updated 43-101 compliant resource estimate in January, which blew away expectations with 11.21 million tonnes indicated grading 9.61% zinc-equivalent and 39.47 million tonnes inferred grading 10.00% zinc-equivalent. This resource estimate puts Macmillan Pass into the world class category of projects boasting 50+ million tonne resources. Now Fireweed is putting the finishing touches on its maiden PEA for Macmillan Pass, and the best part is that there’s a good chance the project is even bigger than the resource estimate being used for the PEA.

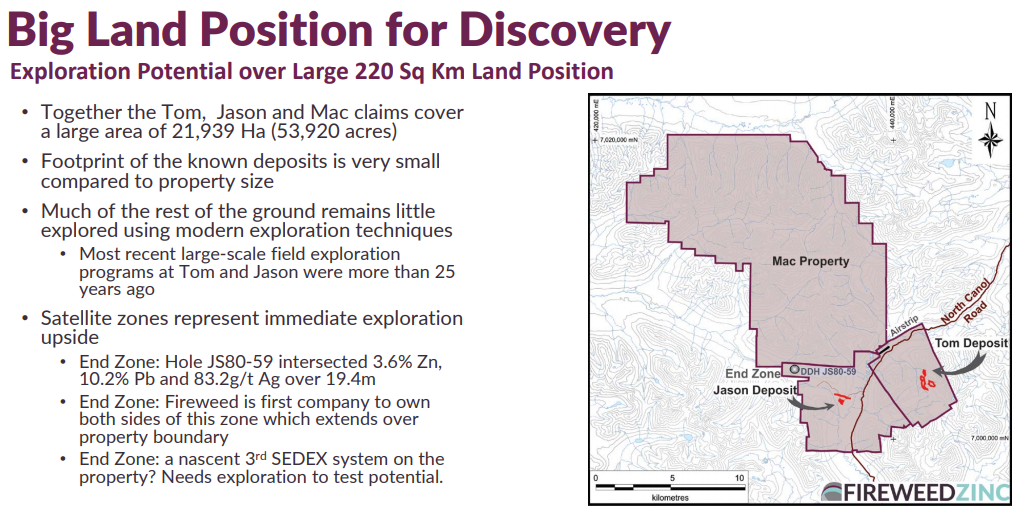

While Fireweed had a sensational exploration program in 2017 by all accounts, there is still substantial blue sky potential as the footprint of the known deposits is very small compared to the total property size.

CEO Macdonald doesn’t hold anything back when he makes it clear that he is optimistic that Fireweed will find more mineralized zones over its 114,000 acre property package.

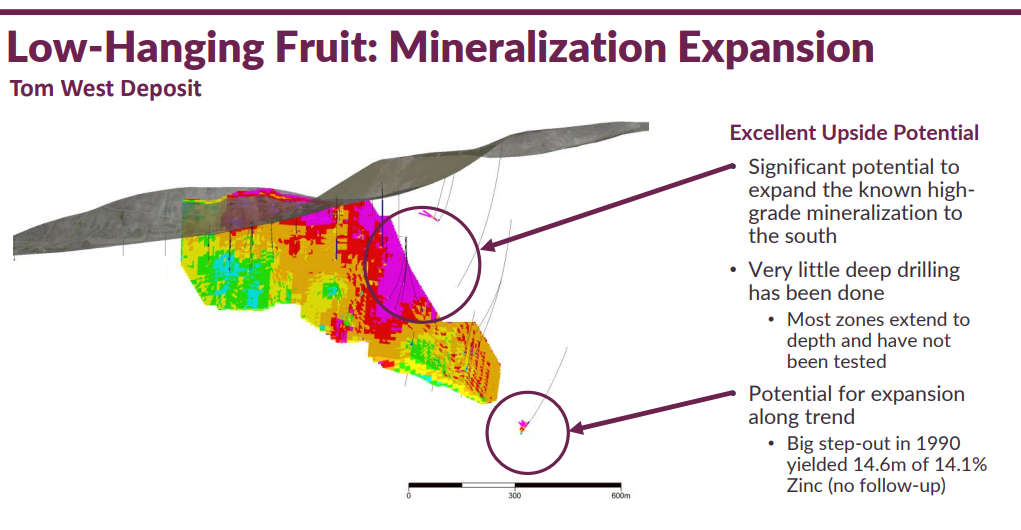

At the Tom West Deposit, there is excellent potential to expand the known high-grade mineralization to the south, and according to Macdonald, “The great thing about Tom West is that as big as it is it’s not really sterilized in any direction.”

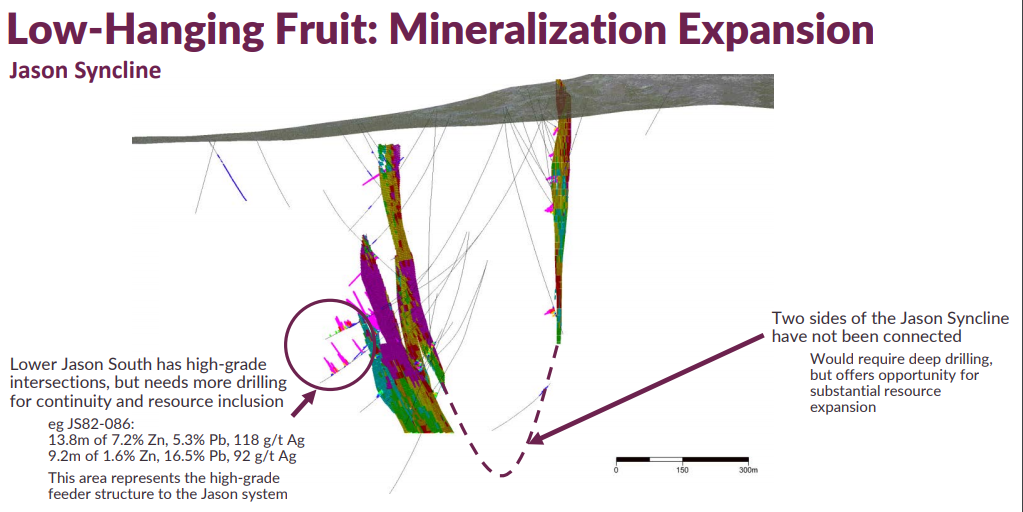

And at Jason South, there is some “low-hanging fruit” mineralization expansion potential, as the two sides of the Jason Syncline have not been connected yet:

Connecting the two sides will require deep drilling, but it could pay off handsomely with substantial resource expansion.

What makes Fireweed so compelling from an investment standpoint is that it is priced at more than a 60% discount to its peer group; zinc juniors are priced at roughly 1.1 cent per pound of zinc in the ground, and FWZ is priced at .32 cents per pound of zinc in its resource estimate. FWZ shares stand to revalue through 4 potential catalysts over the coming months:

-

Release of maiden PEA that will lay out project economics in detail and address concerns around transport costs etc.

-

Infill drilling, which will upgrade a substantial amount of the inferred pounds to the measured and indicated categories. Infill drilling will be important in high grade areas early in the mine life that are currently inferred right now. It’s important for Fireweed to show investors and potential acquirers that the areas that are really driving the economics have been de-risked.

-

Step-out drilling to add tonnes to the total project size, in addition to finding new high-grade zones, which will serve to significantly improve project economics by reducing payback period and reduce marginal cost per tonne produced. The step-out holes will be prioritized by areas that Fireweed feels are higher grade and would replace other, lower grade tonnes early in the mine life i.e. if there is a block of 1M tonnes at 8% ZnEq in the first 10 years of mine life, and FWZ can replace that block with 1M tonnes at 12% ZnEq, they’d want to do that, of course.

-

Exploration drilling – drill new targets and prove up entirely new deposits.

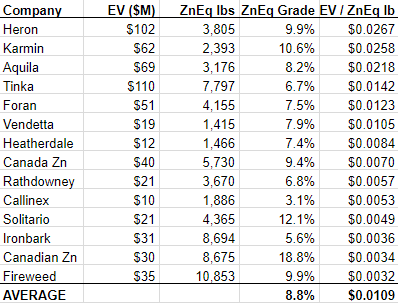

I believe the absurdity of the current Fireweed valuation is illustrated by the table below:

Ironbark Zinc (IBG.AX) is valued at ~10% more than Fireweed based upon the standard enterprise value/Zinc-equivalent pounds in the ground valuation metric. Fireweed has nearly twice the grade that Ironbark has (9.9% vs. 5.6%), more contained metal, and Fireweed’s Macmillan Pass Project is located in a much easier place to work (Yukon vs. Greenland). Yet after all of that Fireweed is still trading at a discount to Ironbark, and virtually every other zinc exploration peer. I believe that 2018 could be the year that FWZ shares bridge a significant amount of this valuation gap.

Another aspect of Fireweed, which I’m not sure many appreciate, is how clean the share structure is; Fireweed was brought to market in a clean IPO in June 2017, and the company barely has 30 million shares issued & outstanding:

After more than 15 years of investing in the junior resource sector, I have come to learn how important share structure can be. Perhaps, more importantly, a company’s share structure speaks to a company’s culture, and how it operates towards either maximizing shareholder value or something else less beneficial for shareholders (running the company only in management’s short term interest i.e. lifestyle companies).

I can state emphatically that Fireweed management, led by CEO Brandon Macdonald and Executive Chairman John Robins, cares tremendously about maximizing shareholder value and avoiding the sort of damaging dilutions that end up ruining so many junior mining companies. Due to its clean share structure and small number of warrants outstanding, Fireweed’s share price could potentially soar in the event of strong buying demand, simply due to the fact that there isn’t a large supply of shares available out there.

Management’s interests are directly aligned with shareholders, and in fact the 4,000,000 “performance shares” are to be awarded only when very clear company milestones are achieved, such as:

-

Growing the total resource by 50% or more.

-

Delivering a positive PEA.

-

Delivering a positive PFS or being taken out.

As Fireweed prepares to set out on a busy summer exploration program the maiden PEA, which is set to be announced in the middle of May, could serve to amplify the value of the Summer 2018 drilling program; upgrading priority zones to the measured & indicated categories will be very important as the company moves closer to a pre-feasibility study, and expansion of known zones through step-outs and exploration drilling of entirely new targets will give plenty of potential upside juice.

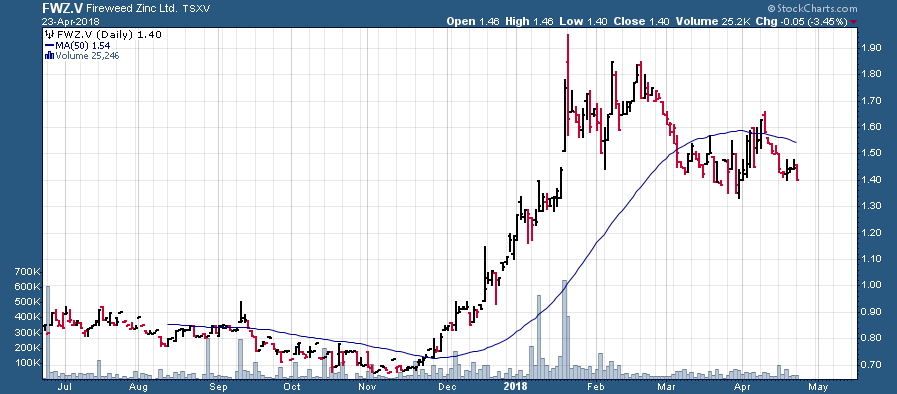

After a ~200% rise from November through January, FWZ shares have spent the last three months consolidating within a relatively narrow range:

FWZ.V (Daily)

This consolidation could be nearing its end as Fireweed gets ready to publish its maiden PEA, followed by a busy summer of drilling at Macmillan Pass. There should be a steady flow of news throughout the rest of 2018, and Fireweed’s modest market capitalization (C$43 million based upon C$1.43 share price and 30 million shares outstanding) has substantial room to revalue upward, as the market begins to appreciate the world class size, grade, and location of the Macmillan Pass Project.

Disclaimer:

The article is for informational purposes only and is neither a solicitation for the purchase of securities nor an offer of securities. Readers of the article are expressly cautioned to seek the advice of a registered investment advisor and other professional advisors, as applicable, regarding the appropriateness of investing in any securities or any investment strategies, including those discussed above. Fireweed Zinc Ltd. is a high-risk venture stock and not suitable for most investors. Consult Fireweed Zinc Ltd.’s SEDAR profile for important risk disclosures.

EnergyandGold has been compensated for marketing & promotional services by Fireweed Zinc Ltd. so some of EnergyandGold.com’s coverage could be biased. EnergyandGold.com, EnergyandGold Publishing LTD, its writers and principals are not registered investment advisors and advice you to do your own due diligence with a licensed investment advisor prior to making any investment decisions.

This article contains certain forward-looking information and forward-looking statements within the meaning of applicable securities legislation (collectively “forward-looking statements”). Certain information contained herein constitutes “forward-looking information” under Canadian securities legislation. Generally, forward-looking information can be identified by the use of forward-looking terminology such as “expects”, “believes”, “aims to”, “plans to” or “intends to” or variations of such words and phrases or statements that certain actions, events or results “will” occur. Forward-looking statements are based on the opinions and estimates of management as of the date such statements are made and they are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed by such forward-looking statements or forward-looking information, standard transaction risks; impact of the transaction on the parties; and risks relating to financings; regulatory approvals; foreign country operations and volatile share prices. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Actual results may differ materially from those currently anticipated in such statements. The views expressed in this publication and on the EnergyandGold website do not necessarily reflect the views of Energy and Gold Publishing LTD, publisher of EnergyandGold.com. Accordingly, readers should not place undue reliance on forward-looking statements and forward looking information. The Company does not undertake to update any forward-looking statements or forward-looking information that are incorporated by reference herein, except as required by applicable securities laws. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SEDAR.com for important risk disclosures. It’s your money and your responsibility.