Ceylon Graphite (TSX-V:CYL, Frankfurt: CCY): A unique opportunity to fuel the surging global electric vehicle industry with the highest quality graphite on earth

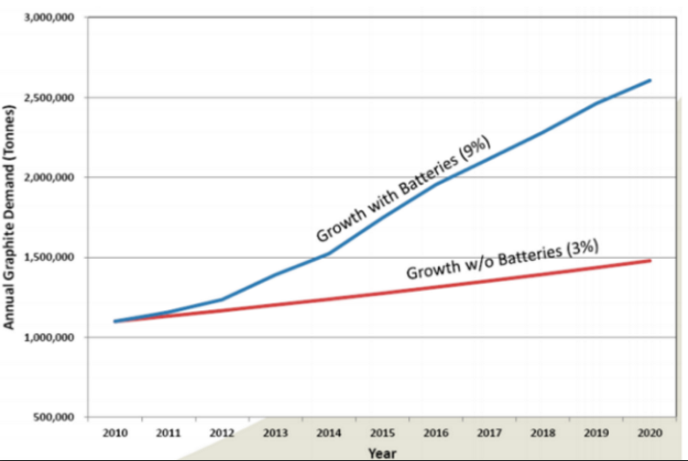

Graphite demand is skyrocketing as a result of the rapidly growing electric vehicle industry. Each Tesla vehicle requires roughly 80 pounds of graphite and graphite demand, especially for high-grade large flake graphite demanded by the electric vehicle industry, is forecast to explode higher over the next few years:

This surge in graphite demand is underpinned by the Chinese government’s plan to have 5 million electric vehicles on the road by 2020. Accounting for the ~625,000 electric vehicles already on the roads in China that still leaves a projected 350 million pounds of graphite demand from China alone over the next four years! While China is the world’s largest graphite supplier the vast majority of its graphite is amorphous lower grade graphite not suitable for electric vehicle batteries.

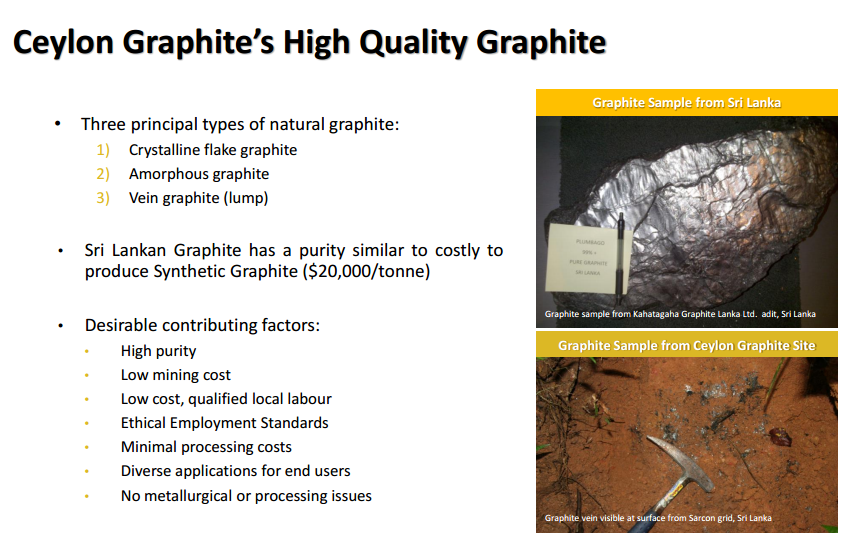

Enter Sri Lanka, a country that used to supply over 50% of the world’s graphite, and Canadian based Ceylon Graphite (TSX-V:CYL, Frankfurt:CCY). Ceylon, founded by Sasha Jacob of Jacob Capital Management, has rapidly acquired most of the past producing graphite properties in Sri Lanka. Sri Lankan graphite is the purest, highest grade naturally occurring graphite globally. It is pure lump vein graphite at grades of over 90%. To add some perspective as to what we are talking about in terms of the absolutely unique quality and abundance of Sri Lankan graphite, the government owned mine has been producing from the same vein since the late 1800s and they are down to around 2000 feet today.

Ceylon finds itself in an enviable position with Sri Lankan grade graphite currently demanding ~US$1500/tonne while Ceylon’s average mining cost is less than US$100/tonne. Due to a shortage of natural graphite globally most battery manufacturers are planning to use synthetic grade graphite which costs many times more, usually over $7,000/Tonne. This puts Ceylon in a unique position; producing the highest grade natural graphite on earth at 90%+ profit margins.

Ceylon expects to enter into off-take discussions shortly, however, the ultimate goal is to establish a JV with a battery manufacturer to produce anodes directly in Sri Lanka. The majority of graphite is from China, and consumers are demanding that companies consider the entire supply chain of their products. China’s environmental track record is troubling for many buyers especially for “green” products like EVs and storage which gives Ceylon a potential advantage in enrolling customers.

Ceylon undoubtedly has considerable potential for upgrading its high quality graphite material and adding considerable value to its already robust margins. Hence, the company is looking to establish a JV with a battery manufacturer to produce anodes. In addition, Ceylon would look to upgrade its material directly to 99.9% pure graphite in order to supply the anode manufacturing and any other customers.

Value add could occur as follows:

-

Mining highest grade, lowest cost graphite

-

Upgrading material

-

JV with battery co to manufacture anodes

-

Graphene or other technologies utilizing pure graphite

The company believes that Graphene, at any reasonable commercial scale, is some time away. When the technology is at the appropriate stage, Ceylon would certainly look to partner with companies to produce graphene. Since Ceylon is beginning with the highest purity, lowest cost graphite material globally, they will have a significant advantage over any other sources.

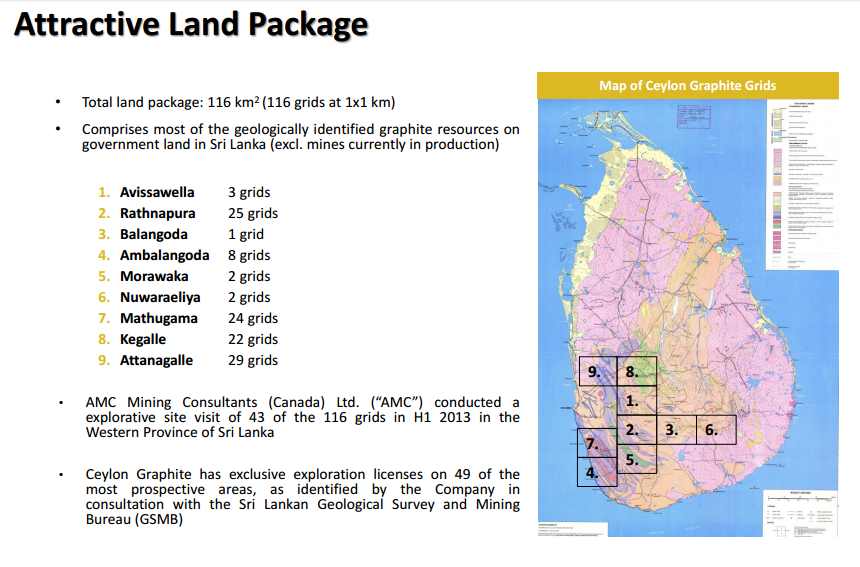

Ceylon has accumulated an attractive land package in the Western Province of Sri Lanka comprising 116 ‘grids’ which are 1×1 km each:

It is estimated that each grid will yield 150-300 tonnes per month. The cost to put each grid into production is very low, approximately $250,000-$500,000 per zone. A drill rig and VLF equipment will be shipped over, which will allow the Ceylon team to have continuous resource data on the sites allowing Ceylon to prioritize production areas.

The Ceylon team is now preparing detailed reports including history, infrastructure (such as roads and power), shaft and adit locations, etc. in order to prioritize the first ten sites. The first two have been confirmed and Ceylon expects production to begin within 6 months. The permitting process for Ceylon is as straightforward as anywhere in the world; the company simply informs the Sri Lankan government where they will be working and permits are typically received 4-8 weeks later.

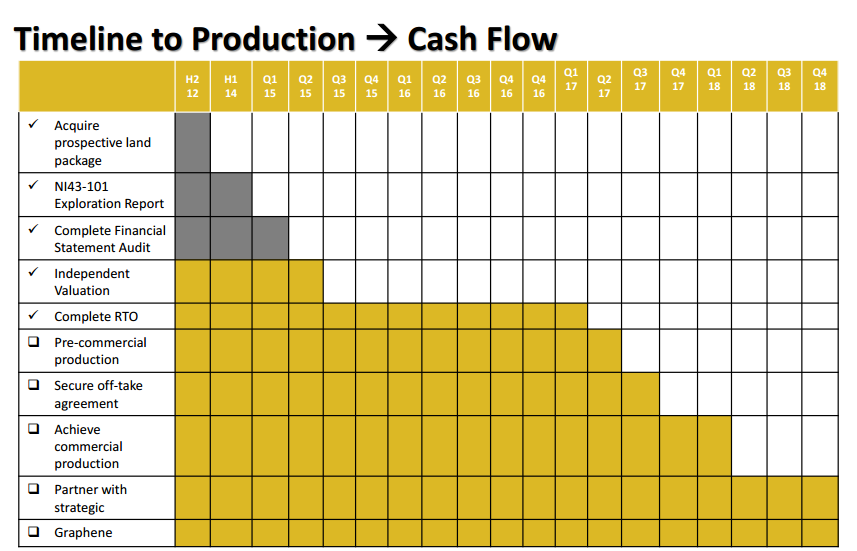

Ceylon’s next big milestones will be to achieve pre-commercial production and then to secure an off-take agreement:

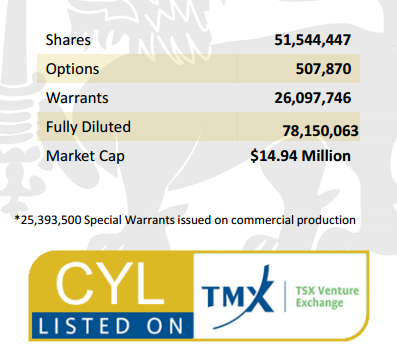

With an eventual goal of reaching commercial production by next year at this time Ceylon has a fast track to large-scale production. Ceylon has identified a production capacity of ~18,000 tonnes of graphite per year – with gross profit margins of ~US$1,400/tonne it’s not difficult to quickly understand the profit potential available to Ceylon shareholders (~US$25 million gross profit at full production); the annual gross profit that Ceylon is staring at is larger than its entire current market capitalization!

Rarely do we come across a company that is literally at the right place, at just the right time, with the right team of people to achieve exceptional success. Ceylon Graphite looks to be that company, uniquely positioned with unparalleled access to the richest graphite mining region on the planet. If Ceylon is able to execute on its timeline and accomplish what it says it will CYL shares should trade up to multiples of current levels. We look forward to following this story with great interest throughout 2017 as this is an exciting time for the suppliers of the global electric vehicle industry.

Disclaimer

The article is for informational purposes only and is neither a solicitation for the purchase of securities nor an offer of securities. Readers of the article are expressly cautioned to seek the advice of a registered investment advisor and other professional advisors, as applicable, regarding the appropriateness of investing in any securities or any investment strategies, including those discussed above. Ceylon Graphite is a high-risk venture stock and not suitable for most investors. Consult Ceylon Graphite’s SEDAR profile for important risk disclosures.

EnergyandGold has been compensated to cover Ceylon Graphite and so some information may be biased. EnergyandGold.com, EnergyandGold Publishing LTD, its writers and principals are not registered investment advisors and advice you to do your own due diligence with a licensed investment advisor prior to making any investment decisions.

This article contains certain forward-looking information and forward-looking statements within the meaning of applicable securities legislation (collectively “forward-looking statements”). Certain information contained herein constitutes “forward-looking information” under Canadian securities legislation. Generally, forward-looking information can be identified by the use of forward-looking terminology such as “expects”, “believes”, “aims to”, “plans to” or “intends to” or variations of such words and phrases or statements that certain actions, events or results “will” occur. Forward-looking statements are based on the opinions and estimates of management as of the date such statements are made and they are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed by such forward-looking statements or forward-looking information, standard transaction risks; impact of the transaction on the parties; and risks relating to financings; regulatory approvals; foreign country operations and volatile share prices. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Actual results may differ materially from those currently anticipated in such statements. The views expressed in this publication and on the EnergyandGold website do not necessarily reflect the views of Energy and Gold Publishing LTD, publisher of EnergyandGold.com. Accordingly, readers should not place undue reliance on forward-looking statements and forward looking information. The Company does not undertake to update any forward-looking statements or forward-looking information that are incorporated by reference herein, except as required by applicable securities laws. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SEDAR.com for important risk disclosures. It’s your money and your responsibility.