IDM Mining is committed to moving forward one of Canada’s highest grade and most economic gold resources to production

-

Targeting 100,000+ ounce (gold equivalent) of high-grade gold production in Western Canada’s most prolific gold district

-

Permits expected by Q1 2017

-

Quick payback, low capital cost, low operating cost, and attractive NPV (especially with weak Canadian dollar)

-

Significant exploration upside; glacial retreat opens up multiple high-grade prospects within 16-km long regional hydrothermal system

Energy & Gold had the opportunity to connect with IDM Mining President & CEO Rob McLeod earlier in the week. IDM is moving its flagship high-grade Red Mountain project forward to production and Mr. McLeod expects permits in hand this year. The project has compelling economics — particularly the quick payback timeline. Higher metals prices and/or future exploration success would be icing on the cake for IDM investors.

CEO Technician: What is IDM Mining?

Rob McLeod: We are focused on our flagship project, which is the high-grade Red Mountain underground gold project. Red Mountain is an advanced-stage project which is currently mid-way through the British Columbia permitting process. We’re also commencing a feasibility study which will outline an affordable (less than C$100 million capex) 1,000 tonne/day bulk minable mining operation in a great political jurisdiction: the ‘Golden Triangle’ of Northwestern B.C.

Red Mountain is a unique project in this type of market. First of all it’s in Canada and Canadian producers are benefiting from the major increase in the US dollar relative to the Canadian dollar, which has made mining projects in Canada tremendously more economic. So one year from now we expect to be commencing construction on a project that has the potential to produce more than 100,000 ounces of gold per year with rapid payback (a year or less) and phenomenal exploration upside. We just released news that contemplates a year-round operation, rather than seasonal mining as contemplated in our 2014 PEA.

CEO Technician: What kind of exploration upside do you see possible at Red Mountain?

Rob McLeod: This is the richest area in Western Canada for gold and it is famous for spectacularly high-grade deposits. I believe Pretium’s Valley of the Kings is going to be one of the richest mines in the world; the grades there are exceptional and unique on a global basis. There really isn’t anything like it. Nearby is the past-producing Eskay Creek mine, which was probably the richest mine anywhere in the world in the modern era. It produced a little over 9 million ounces gold equivalent from slightly over 1 million tonnes of ore. This area is well-known for pretty exceptional high-grade gold deposits.

CEO Technician: Red Mountain is an extremely high-grade mine that is economic even at lower metal prices. From my understanding your main challenges are the fact that it’s an underground mine and a 7-kilometre access road needs to built to access the project — is that correct?

Rob McLeod: There’s an existing road that gets to about 7 kilometres away from the deposit, so there is a little more road that needs to be built. We also have the benefit that there’s about 2,000 meters of production-size underground development already in place, put in during the 1990s. There are 3 en-echelon ore bodies and the first zone, which is called the Marc Zone, is the highest grade body with about 10 grams/tonne on average and it’s already accessed with three cross cuts.

CEO Technician: Where are you at in the timeline of permitting and moving the project into production?

Rob McLeod: Our most recent PEA (preliminary economic assessment) was published in July 2014. Imminently we will be announcing an updated resource estimate that will include a parallel zone to the three ore bodies, called the 141 zone. We are going to take the updated resource estimate in addition to a change in the scope of the project and issue a new PEA. At the same time we have also commenced our feasibility study and in early fall, we will submit our environmental application to the federal and provincial regulators in B.C. That triggers a 180-day maximum legislated review process where they have to give a thumbs-up or thumbs-down. After that we will have our environmental certificate, which allows us to commence construction. So we will have the feasibility study done by the end of this year and we hope to have our permits by the first quarter of 2017. Then we will have a shovel-ready project.

As an intermediate step we are doing an underground drilling program this spring, in order to upgrade the last little bit of inferred resource into the indicated category. We can also do a little bit of step-out drilling to add further resources along strike and to get a bit more material to refine our metallurgical process.

CEO Technician: How much capital will IDM require to advance to the shovel-ready stage early next year?

Rob McLeod: We currently have about C$1 million in the treasury and we will need about another C$7 to 10 million to get to the stage where we can begin construction at Red Mountain. We are exploring various options to raise this amount.

CEO Technician: What is the total estimated cost of all the infrastructure build-out required to bring Red Mountain up to full production?

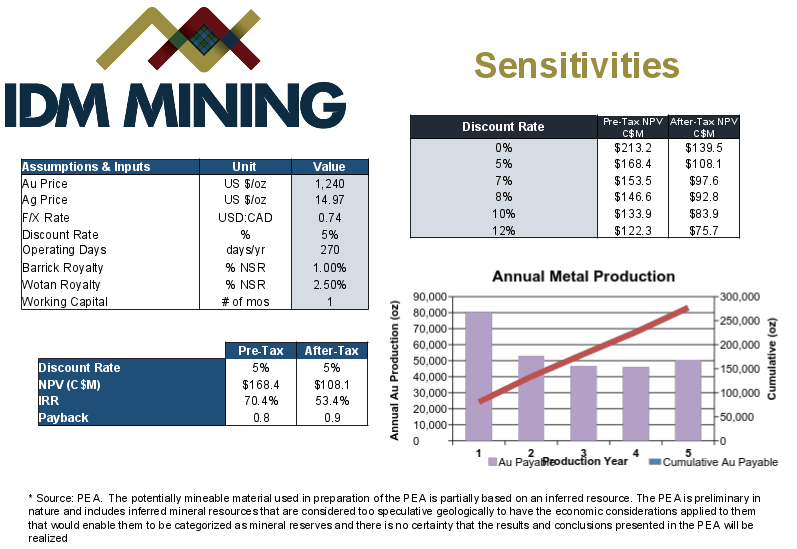

Rob McLeod: Based on the 2014 PEA the estimated capex is C$76 million; however, there could be some increased costs given the weaker Canadian currency (sourcing certain infrastructure from the U.S. such as mills, mining fleet, etc.). We still foresee a total capex below C$100 million.

CEO Technician: Where are you looking to source the funds for the capex build-out?

Rob McLeod: It’s a lot easier to raise the amount of money to build a mine than to raise money to explore in this market. The payback on this project is very quick so it can probably stand a pretty high level of debt. We can debt-finance a certain portion of it; we have looked at various debt alternatives during the pre-development stage and received numerous term sheets but until the project is fully de-risked — which means permits in hand — we aren’t interested in signing a financing deal (because of the much higher cost). Why raise debt when you can raise equity at this stage?

CEO Technician: How are the economics of the Red Mountain project at current precious metals prices?

Rob McLeod: In our July 2014 PEA the inputs we used were US$1,250 gold, US$20 silver, and the big one is the USD/CAD exchange rate of .95. Currently the USD/CAD is about .74 so the economics are much better than the numbers in our PEA. We’ve seen a lot of Canadian producers such as Claude Resources, Richmont Mines, and Lake Shore Gold get taken out in the last couple of months because of that exchange rate difference.

CEO Technician: What is the market missing? IDM is trading at about an C$8-million market cap and the after-tax NPV of the Red Mountain Project is over C$100 million. What do you think accounts for this valuation gap?

Rob McLeod: I think it has a lot to do with the jurisdiction of British Columbia. So many mining companies are headquartered here and everybody has an opinion on the state of the mining industry in the province. I’ll tell you that it’s one of the best mining jurisdictions; it’s rigorous but it’s an expedited process to get mines permitted. In B.C. it’s a 180-day review process after two years of baseline work. I believe we are trading at a bit of a discount due to some of the challenges that have faced other B.C. projects, such as Mount Polley.

The other challenge a lot of people have with the project is that our current resource base isn’t over 1 million ounces. It’s about 380,000 ounces of measured & indicated and another 82,000 ounces of inferred. In addition, our initial mine life is 4-5 years. However, our philosophy is to get the mine built and producing, then we can drill out along strike and expand the resource and mine life.

Geologically, we are very similar to Valley of Kings and Seabridge’s KSM Project. There has been very little modern exploration since 1996 until IDM got involved. Another cool aspect to exploration in this part of the world is that the glaciers are melting at a really tremendous rate here in this part of the world. The glacier called the Cambria Icefield, right next to Red Mountain, has pulled back on the order of 2 kilometers. There is precedent for a discovery to melt out from under the ice — the Valley of Kings only melted out a decade ago. There are a whole bunch of projects in our zone that have recently melted out that we have yet to drill. We believe there is tremendous of upside for exploration discoveries on the Red Mountain property package.

IDM’s Red Mountain Project offers the attractive proposition of a fast path to mine construction, production, and a relatively quick payback. Moreover, the exploration upside in a rich gold district offers investors some sweet potential investment upside. Look for an updated resource estimate in the coming weeks and an updated PEA in the 2nd quarter.

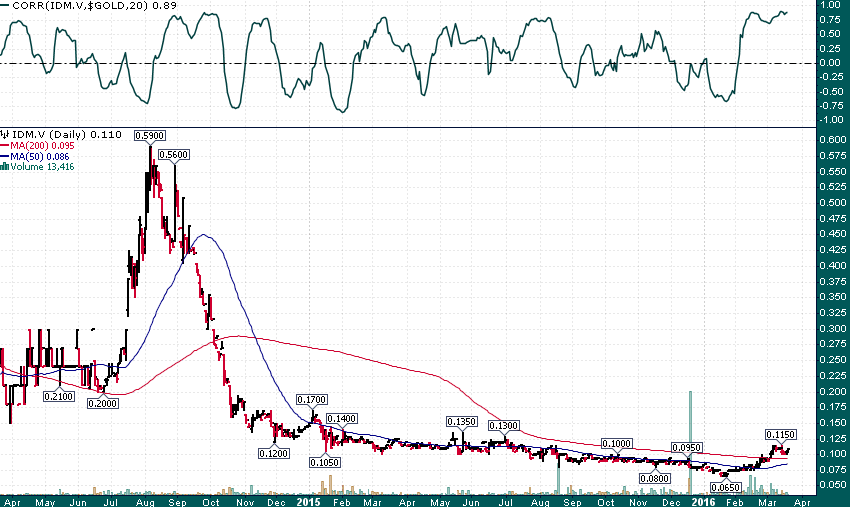

IDM shares have nearly doubled since the January low and the stock is currently trading with a roughly 90% correlation to the gold price:

A move above the C$.13 level would be highly significant given the 18-month bottom that is in place.