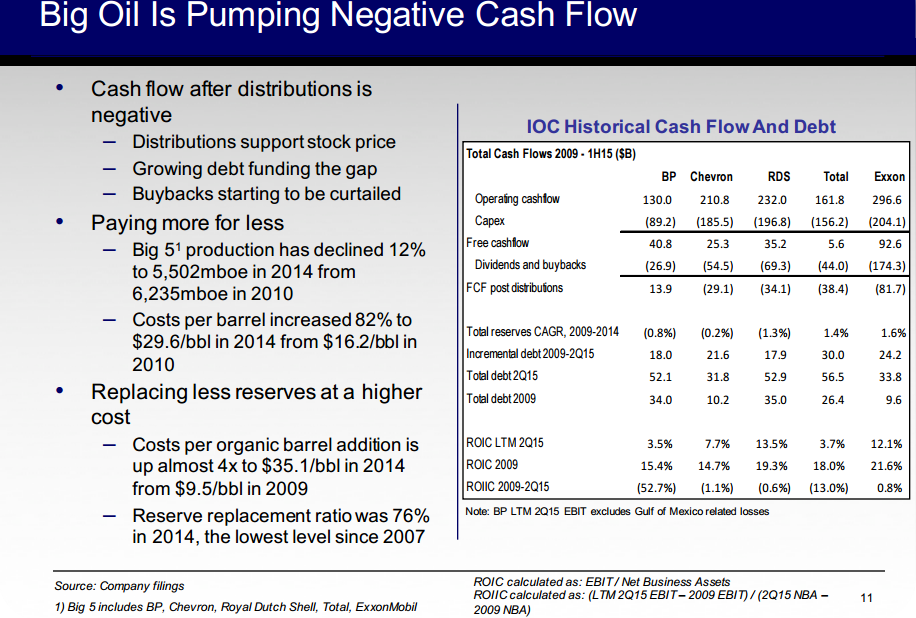

Famous hedge fund manager and short seller Jim Chanos of Kynikos Associates recently made a presentation at Grant’s Fall 2015 Conference titled “Energy Investments After The Fall: Opportunity Or Slippery Slope?”. A couple of key points among many that Chanos highlights are that oil e&p companies are paying more and more per barrel of oil for organic growth with companies now paying over $35 per organic barrel addition. Considering that WTI is currently meandering near $40/barrel this means that organic growth is hardly profitable and emphasizes the challenges facing the oil & gas services companies such as Haliburton (HAL) and Schlumberger (SLB). Moreover, production from the super majors is in decline and the Big 5 oil majors (BP, Chevron, Shell, Total, ExxonMobil) are paying more for less production as they piled on debt during the last 5 years as ROIC (return on invested capital) declined:

My main takeaways are that the crude oil price is well supported in the $35-$40/barrel area simply because a huge amount of supply would quickly no longer be available if prices fell much further. And perhaps the most important takeaway is to steer clear of any oil & gas company that is not well cashed up and/or holding a substantial amount of debt. The winners will be separated from the losers over the next 6 months and while there might not be many winners in the oil & gas space, companies that are well positioned to snap up existing production at fire sale prices will do very well.

Click over to read all the slides from the presentation – Energy Investments After The Fall: Opportunity Or Slippery Slope?