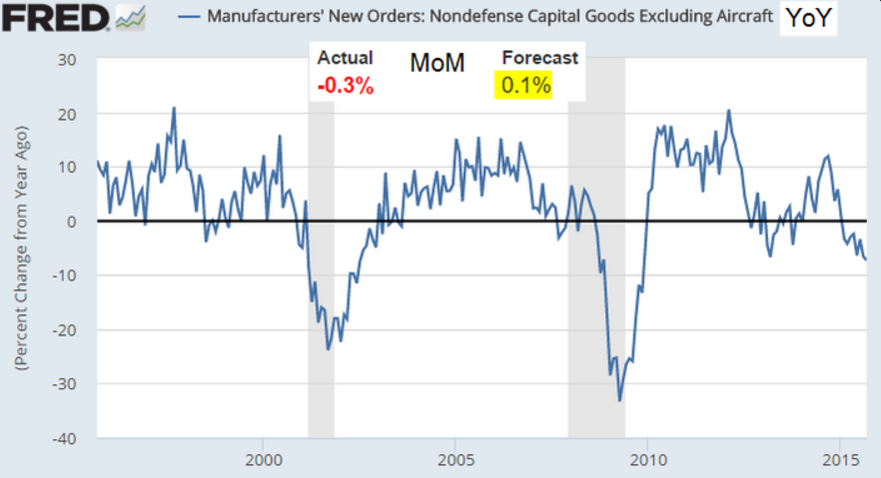

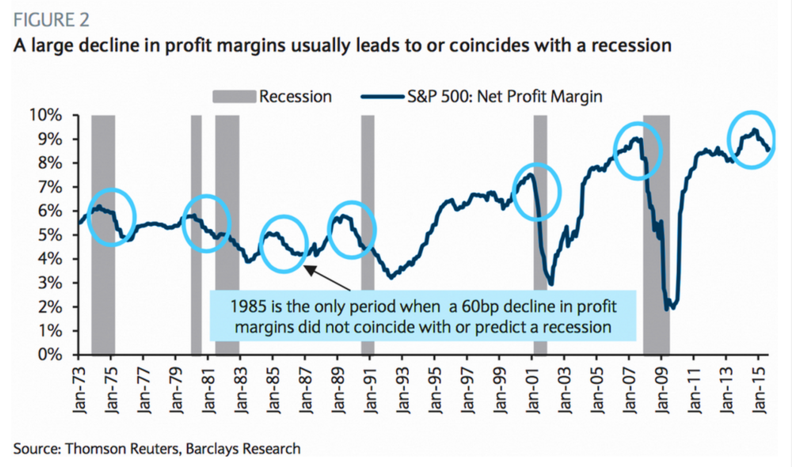

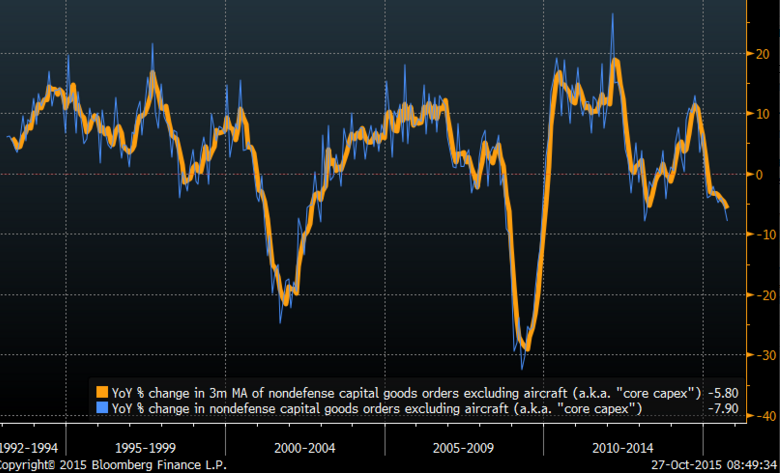

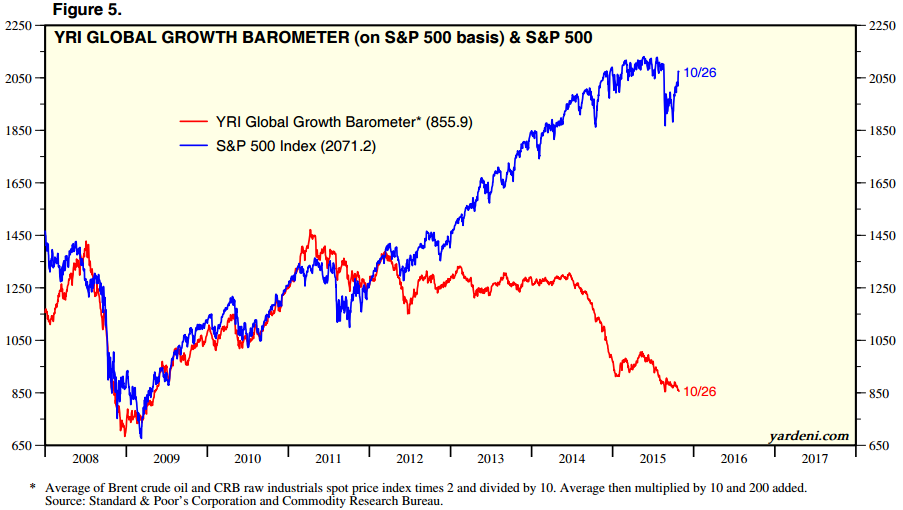

The recent trend in economic data is, to put it nicely, poor. Factory orders, new home sales, corporate profit margins, and various indicators of global growth are all trending lower with many reaching lows not seen since 2009:

Factory orders (ex-aircraft)

S&P net profit margin with recessions (grey)

McCulley Indicator (lowest level since 2009)

Yardeni Global Growth Barometer (lowest level since 2009)

Many of the same macroeconomic challenges that were present when gold rose above $1900/oz in 2011 are still present, and quite a few new challenges have also appeared. The gold bull run from $250/oz in 2001 to $1923/oz in 2011 was largely built upon the potential decline of the US dollar the world’s reserve currency and rampant central bank monetary policy interventions/easing.

While not much has changed with regard to global central banks, a brief respite for the dollar between 2013-2015 caused quite a tumble for gold. However, there are a growing number of signs that gold may put in a bottom during the summer and the specter of global deflationary pressures and recession fears could incite the latest round of monetary stimulus from central banks. Gold would likely be a big beneficiary in another round of monetary policy easing and the negative real interest rates that would likely reappear as central banks pump more liquidity into a deepening liquidity trap.

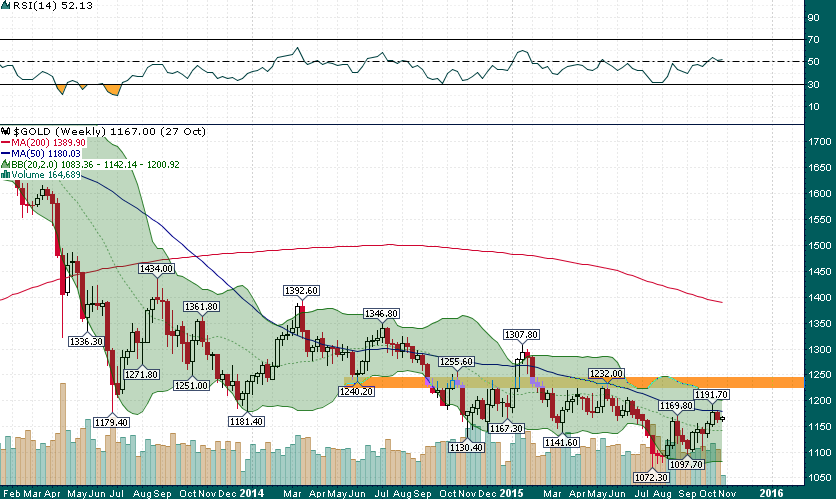

From my estimation a breakout above important support/resistance near $1230-$1240 would signal that all systems are a go for gold and that the July low was indeed a long-term bottom and the likely end of the 2011-2015 cyclical bear market in gold:

Gold (Weekly)

However, gold may not be the best way for investors to play a resumption of the gold bull market. After years of cost cutting and leaning down the once bloated and inefficient gold miners are ripe to profit from a rising price of gold. The average all-in sustaining cost (AISC) for the largest gold producers has declined from $1208/oz in 2014 to a projected $950/oz this year.

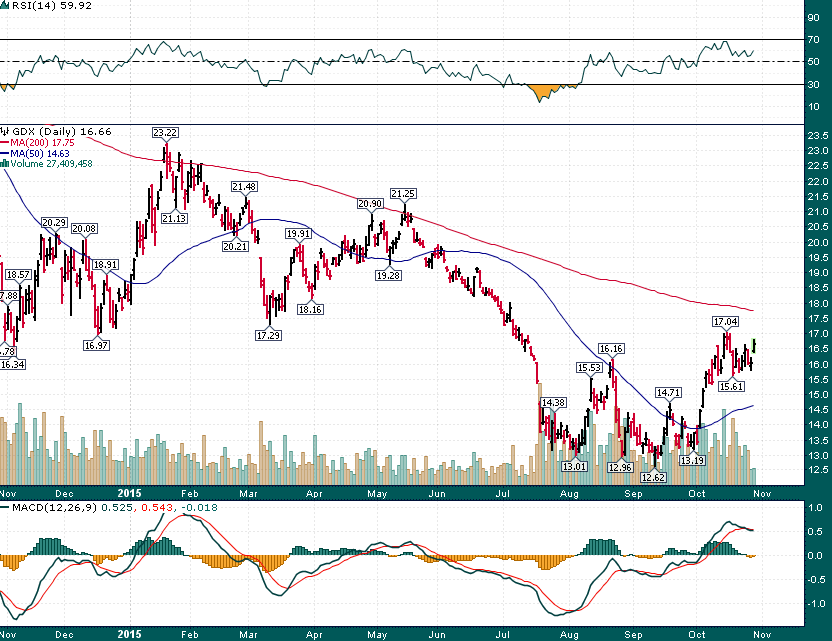

After spending the summer putting in a bottom, the gold miners (GDX) are finally showing some signs of life. A ~20% rise thus far during the month of October has GDX once again threatening to test its downward sloping 200-day simple moving average (red), something which seemed to stop the rallies in January and May of this year:

GDX (Daily)

A breakout above the recent range (~$17) and an eventual move above the 200-day moving average would also trigger a series of technical green lights that the bottom is in and that a nascent uptrend is underway in the goldies. It should also be noted that November is the 2nd most bullish month of the year (August is the most bullish) for the gold mining sector historically.

For GDX the key levels to keep an eye on are $17 then the 200-day moving average and previous support near $17.75-$18.00. On the downside a break back below ~$15.50 would be a bearish sign.