By most accounts Donald Trump is a billionaire and he often reminds us of this with sentences such as “I’ve done great…” or “I don’t need anybody’s money….i’m really rich.” Most people think that if someone is able to accumulate vast personal wealth that they must understand finance and economics at a very high level. This is a mistaken notion and Donald Trump’s proposed economic policies are all the evidence we need to know that he really doesn’t know how to “make America great again.”

In one sentence Trump says that he will balance the budget and create “millions of jobs” and then in the next he espouses trade tariffs with our largest trade partners and a massive reduction in tax rates for the segment of the country that pays the most in taxes. Simply put it doesn’t add up and many of Trump’s economic proposals are archaic and dangerous.

Trade protectionism (tariffs, quotas, bans, etc.) has been long proven to not work and in fact creates a net economic drain as free trade and the magic of comparative advantages between trading partners are stifled. Before delving into some of the details and potential implications of Trump’s proposals here is some of what you can expect if Trump is elected and able to implement his proposals:

-

The tax preparation industry will shrink considerably (one page form for those who don’t owe any income tax).

-

The government sector of the economy will shrink considerably.

-

Trade wars with our key trade partners (China, Mexico, etc.) will likely break out.

-

The stock market should perform poorly as economic growth grinds to a halt and the labor force shrinks.

-

Deflation has a good chance of taking hold as ¼ of the U.S. economy takes a substantial hit.

-

Trump’s tax proposals (reducing the top federal income tax rate to 25%, reducing the corporate tax rate to 15%, reducing the short term capital gains rate, and eliminating the death tax) greatly benefit the rich.

While Trump’s website claims that his tax proposals are revenue neutral (Trump projects that getting rid of carried interest loopholes, and offering a one-time deemed repatriation of corporate cash held overseas at a significantly discounted 10% tax rate will offset the many sources of revenue losses his proposals will generate) it is difficult to fathom how shrinking the largest sectors of the economy and reducing tax rates on the biggest sources of tax revenue will not have a materially adverse impact upon tax revenues.

Moreover the impact of a Trump Presidency on markets is likely to not be pretty given Trump’s trade proposals which include levying huge tariffs on China and Mexico (trade protectionism reduces growth and can actually result in economic stagnation which crushes equity market valuation multiples). Trump has continually demonstrated a neophyte understanding of economics and how the U.S. government finances itself, the following quote should raise more than a few eyebrows:

“I would borrow, knowing that if the economy crashed, you could make a deal.”

Make a deal?

The US dollar is the global reserve currency because global investors know that US government debt is as good as gold (in terms of being repaid on time, in full, and with interest). In fact the yield on the 10-year US Treasury note is often used in finance as the ‘risk-free rate’ because investing in U.S. Treasury debt is broadly viewed as risk-free; while Treasury debt investors may endure interest rate and currency risk, there is no default risk. The thought of a U.S. President even floating around the idea of a “debt deal” is both reckless and extremely dangerous.

The U.S. is still a long way away from not being able to service its debt repayments and global bond investors have continued to display a voracious appetite for buying ever larger amounts of U.S. Treasury paper. Any notion to the contrary is just plain wrong and irresponsible for a person in high political office (or running for high political office) to utter.

Based upon what is published on Donald Trump’s own website it is my opinion that a Trump Presidency is likely to result in stagflation, and bring forth several headwinds for the economy and in turn the U.S. stock market (and global markets). A combination of greater deficit spending (based on the huge tax cuts Trump is proposing while there are no proposals for substantial spending cuts) and protectionist trade policies is likely to yield stagnant or negative economic growth amid stubbornly high consumer prices (resulting from reduced international trade which will make goods that we have typically imported from China, Mexico, etc. more expensive).

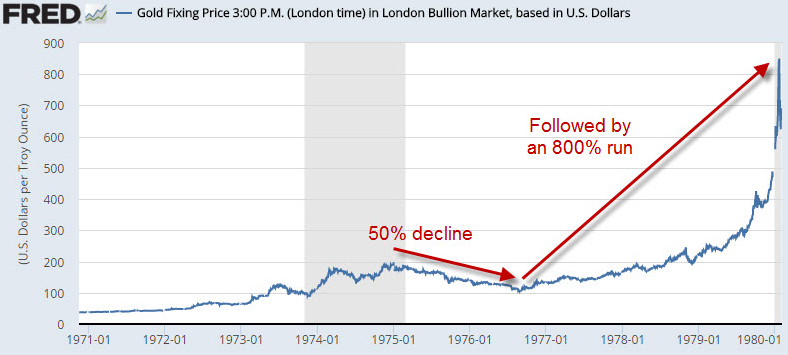

How does one invest in a stagflationary economic environment? We need only look to the 1970s to find out how one might want to invest against a backdrop of stagflation – gold rose more than 800% between 1976 and 1980:

While gold enjoyed its best decade ever in the 1970s, stocks performed poorly on an inflation-adjusted basis and bonds performed terribly as inflation expectations (and bond yields) soared.

While there are numerous factors which affect investors’ demand for precious metals, I envision a scenario in which a Trump Presidency is short term bearish for precious metals (due to a stronger US dollar and rising real yields) while creating a ripe environment for an eventual large rise in precious metals due to increased economic instability, increased geopolitical tensions, more accommodative Federal Reserve monetary policy (to counter Trump’s deleterious economic and fiscal policies), and the decline of the US dollar as the global reserve currency.

In summary, if Trump is elected President of the United States investors will likely want to sell some of their stocks and increase their allocations to gold and select gold mining shares.

DISCLAIMER: The work included in this article is based on SEDAR filings, current events, interviews, and corporate press releases. It may contain errors, and you shouldn’t make any investment decision based solely on what you read here. This publication contains forward-looking statements, including but not limited to comments regarding predictions and projections. Forward-looking statements address future events and conditions and therefore involve inherent risks and uncertainties. Actual results may differ materially from those currently anticipated in such statements. The views expressed in this publication and on the EnergyandGold website do not necessarily reflect the views of Energy and Gold Publishing LTD, publisher of EnergyandGold.com. This publication is provided for informational and entertainment purposes only and is not a recommendation to buy or sell any security. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SEDAR.com for important risk disclosures. It’s your money and your responsibility.