Around this time of year (since 2017) I publish a Tax Loss Silly Season Shopping List of stocks that I believe offer attractive entry points. I do this exercise for myself as much as I do it to benefit my readers. I usually start with 15-20 possibilities, then gradually whittle the list down to the six best ideas. My track record on these annual lists is very good but it’s important to remember that the idea behind the list is not to find stocks that should be held for years. Instead, the idea is to find beaten down and oversold diamonds in the rough that could shine much brighter early in the new year. These are trades, not marriages.

The criteria for this year’s list is the stock must be down year-to-date and well off its highs for the year. Thus making it a candidate for selling that is motivated primarily by individual tax liability considerations (booking losses to offset taxable gains elsewhere) that have little to do with the future opportunity available to shareholders of the company.

The exercise of picking stocks that have had poor performances year-to-date is an interesting one because most of the poor performances have some common themes including:

- Delays (drilling, assay lab results, permits, etc.)

- High expectations at the beginning of the year (high market caps relative to the stage of the companies’ projects etc.)

- Companies that are pointing to next year, thus creating a situation in which many investors don’t see much risk of missing out by selling and waiting 31 days

While narrowing the list down, I focused on companies with high-quality management teams that had simply experienced some bad luck in an impatient market environment in 2021. Each one of the companies in this year’s list has a legitimate chance of delivering huge returns over the next 12 months. However, each one is also dealing with varying levels of investor disappointment (and the resulting overhead share supply overhang) that will need to be reversed by delivering strong results and meeting key milestones on time in 2022.

The annual tax loss silly season shopping list is not intended to offer an exhaustive analysis of each company. Instead, the focus is getting to the salient points that make these stocks attractive propositions at their current market valuations. Think of it as a list of ideas that might prompt you the reader to dig deeper, schedule a meeting with the CEO(s), or add some symbols to a watchlist.

I have spoken with the CEO of each company in this year’s list during the last few weeks and a few probably wondered why I was so interested in their company. Based upon my CEO interactions, I also gained confidence in each one of the companies in this year’s list. Insider buying and strong insider ownership only added to that confidence. It’s also no accident that four of the companies on this year’s list have projects in Nevada and Arizona (the #1 and #2 mining jurisdictions globally according to the 2020 Fraser Institute Mining Investment Attractiveness Index).

Without further ado, here is my Tax Loss Silly Season Shopping List for 2021….

Angold Resources (TSX-V:AAU, OTC:AAUGF) – Angold is not even a year old as a public company. AAU raised C$8 million at $.40 at the end of 2020 and the company subsequently began trading on the final day of 2020. Since reaching an all-time high of $.53 in the first few trading days of 2021, it has been tough sledding for Angold. A combination of high expectations and drilling delays at AAU’s Iron Butte Project in Nevada has resulted in a steady share price decline:

AAU.V (Daily – 2021)

At today’s price of $.135, investors are able to buy Angold shares at a 69% discount to the investors who participated in Angold’s last financing, the $8 million raised at $.40 with no warrants in late-2020.

While Angold may have not met investors’ high expectations in 2021, the company is better positioned to deliver for shareholders than it was 10 months ago when its share price was more than double what it was today.

If we were to judge a company on its management and advisors alone, then Angold would have to be near the top of any list in the junior mining sector. CEO Adrian Rothwell has over 25 years of experience in the mining industry including founding, operating and selling many junior mining ventures. Rothwell is the former executive of Goldcorp and KORE Mining, and current Chairman of Lucky Minerals. Advisors Craig Parry, Doug Ramshaw, and Michael Konnert also bring a wealth of experience and a track record of success in the junior mining sector to Angold.

Angold has four projects spread out across Canada, Chile, and the USA. Success at any one of these projects would more than justify the current C$11.3 million market cap.

2022 is set to be a big year for Angold with diamond drilling of up to 10,000 meters at Iron Butte slated for the first half of the year. Pre-drilling using an RC rig is already underway at Iron Butte, making the diamond core drilling more efficient and cost-effective.

Iron Butte is located in a low-sulphidation epithermal (LSE) environment just outside of the Battle Mountain Trend of north-central Nevada. To say this is elephant country would be an understatement, some of the largest gold mines in the world are located within 100 miles of Iron Butte.

The Iron Butte Property has a historic resource (non 43-101 compliant) of 606,186 ounces at an average grade of .62 g/t gold. What makes Iron Butte so interesting to me is that the historic drilling was virtually all done at depths of 250 meters or less. Iron Butte is a low-sulphidation epithermal deposit model, which means the shallow drilling most likely intersected disseminated, lower grade precious metals mineralization. Deeper core drilling to depths of between 300 and 600 meters will target higher grade gold and silver that is typically deposited just above the boiling floor in low-sulphidation epithermal systems.

An MT Survey (Magnetotellurics Survey) conducted by Angold helps to demonstrate the lack of depth to historic drilling and the apparent higher resistivity zone that exists below the limits of the historic resource. The boiling zone has not been tested and Angold is seeing coincident resistivity and conductivity highs right in the place they should be for a textbook intact LSE system.

I have chosen to focus on Iron Butte, but the Uchi Gold Project (Uchi is quickly becoming an emerging Ontario gold district) and Chile projects (Cordillera and Dorado) also hold tremendous potential to unlock value for Angold shareholders. The company is likely to raise capital in the next couple months in order to fund 2022 drilling. However, I view the $.20 share price level (or below) as offering a very attractive risk/reward entry point.

Considering that low sulphidation epithermal gold/silver systems can often carry extremely high grades of 30+ g/t gold near the richest parts of the system (near the boiling zone), Angold’s phase I/II drilling at Iron Butte will be followed closely.

This is a rough timeline of work programs and news flow we can expect from Angold between December 2021 and mid-2022:

- December/January at Iron Butte: Complete and interpret IP (still in the field), soils, rock chip and re-assay program at Iron Butte. Refine drill targets for permitted 10,000 meters program. The re-assay program should save Angold about $2,000,000 in drilling expenses if it comes close to historic assays – if we want to use these results to update a resource after the next drill program (eliminates QA/QC twinning). Permit road capping at Iron Butte (will save so much time and money in the spring/summer for drilling traffic at site).

- December/January at Cordillera (Chile): Complete grid soils in-fill at Cordillera. This is a substantial program that will allow Angold to tightly target (and expand) mineralized zones under cover where it has never been drilled before – there is potential to host a large deposit here. Continue to optimize targets for phase I drill program at Cordillera.

- February/March 2022 at Iron Butte: Road capping – first step of the drill program. In March, Angold will commence drilling at Iron Butte with a Phase 1 core program of about 3,000 meters. Intention is to test both deep targets highlighted in recent MT/IP as well as structural zones connecting North Zone and Red Ridge (+ stepping out at surface to the south of RR and north of NZ).

- Q2 2022: The focus will be on Iron Butte with the potential to carry out a smaller 2,500 meter program at Cordillera (Chile) to expand the footprint there.

While the current treasury of just over C$1 million in cash will need to be topped up soon, I have no doubt that the strong network of Angold’s management team and advisory board will have no problem in filling up any financing early in the new year. Angold is dirt cheap at today’s C$11.3 million market cap and I have used the recent share price weakness to accumulate a significant position in the stock.

Elevation Gold Mining (TSX-V:ELVT, OTC:EVGDF) – Another major disappointment in 2021 has been the performance of the merged Eclipse/Northern Vertex company, Elevation Gold Mining. ELVT owns the Moss Mine in the Walker Lane Trend of NW Arizona, as well as the Hercules Project along the same trend in NW Nevada.

ELVT.V (Daily)

Elevation is producing 30,000-40,000 ounces of gold per year at Moss. While the production and cash flow is nice, the real potential exists in increasing production over the coming years, supported by a 1,000,000+ ounce resource that continues to grow.

The market is currently giving Elevation zero credit for the potential for increased production and exploration success across its 168 square kilometer land package at Moss. Never mind the Hercules Project in NW Nevada, which encompasses another 100 square kilometers.

The risk of combining a huge underexplored/unexplored property package with a producing asset is that the market focuses only on the production profile and gives little credit for the exploration potential in the rest of the portfolio. The good news for investors today is that Elevation’s current market valuation offers one of the best risk vs. reward propositions I have seen in a long time.

Using a $1757 gold price and $22.10 silver price Moss generates a US$50.6 million after-tax NPV(5%). Those metal prices are below today’s spot prices and this analysis only assumes that the mine life at Moss will extend to 2025 at a mining rate of 11,000 tons of ore per day. Considering that the life of mine plan published earlier this year only includes proven & probable reserves (184,500 ounces of gold and 2.2 million ounces of silver), it is virtually certain that the mine life will extend beyond 2025 (due to the 490,200 ounces of gold and 5.75 million ounces of silver in the measured & indicated category that aren’t in the life of mine plan). In addition, there is also significant potential for the production rate to increase beyond 11,000 tons per day.

A bonus that could bring significant attention to Elevation during the 1st half of 2022 is drilling a brand new target at Florence Hill (bottom right corner of map below):

The Florence Hill and Grapevine areas are of particular interest because there is significant advanced argillic alteration and silica ledges present. The alteration signature of a potential high-sulfidation target is coincident with aeromagnetic geophysical anomalies at Florence Hill. The possibility that the low sulfidation epithermal systems (West Oatman and Moss vein systems) and alteration zonation are vectoring back to the potential mineralization source in the structural intersection represents a significant exploration target for Elevation. Additional ground follow-up exploration is being conducted to assess whether the alteration is associated with a coupled high sulfidation epithermal above a porphyry system or a large-scale low sulfidation system that intersected the palaeo water table.

The exploration targets at Moss offer pure upside from the current bare bones valuation. Achieving operational efficiencies that generate increased production (45,000 ounces of gold per year) and lower costs would be enough to see significant upside in Elevation shares from current levels.

Elevation is about as cheap as I have seen a combination of a producing Arizona/Nevada gold asset plus a huge, highly prospective exploration package. I think it’s important to add that this is a management team that knows how to win and create value for shareholders. As cheap as I think Elevation is at $1.04 per share, I would really like to see insiders step up and show some conviction in the value of the shares after a nearly 70% decline in 2021.

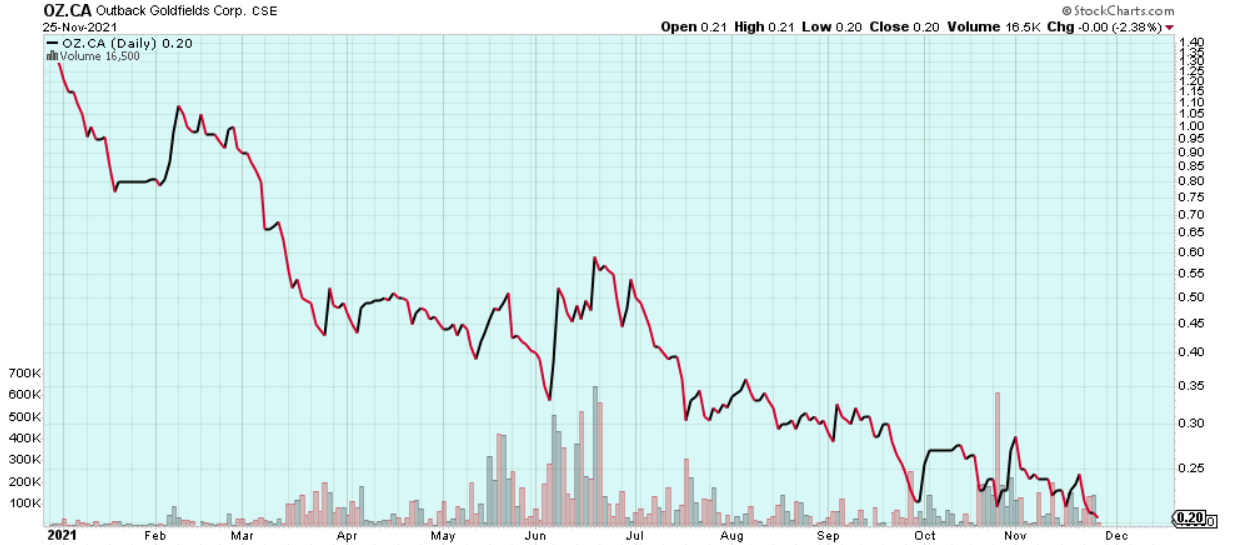

Outback Goldfields (CSE:OZ, OTC:OZBKF) – While Angold has certainly had a disappointing year, Outback’s challenges in 2021 probably take the cake. Similar to Angold, Outback launched in December 2020 amid quite a bit of fanfare. Drilling delays and pandemic related challenges in Australia led to quite a bit of shareholder disappointment in 2021 for Outback.

Outback Goldfields (Daily)

The hiccups of 2021 are in the rearview mirror and by my estimation the market has extremely low expectations for Outback in 2022. Some of my favorite trade setups in the juniors are when the market has extremely low expectations for an otherwise strong management team and project portfolio.

Outback just completed a phase 1 drill program at its Yuengroon Project and it will be following up with a phase 2 program at Yuengroon in January/February. This will be followed in March by drilling at one of Outback’s crown jewels, the Ballarat West Project.

In total, Outback has four properties in the Victorian Goldfields of Australia (the Victorian Goldfields have produced more than 80,000,000 ounces of gold historically). The Victorian Goldfields are a prolific gold district in southern Australia that is undergoing a bit of a modern day gold rush. The success of Kirkland Lake’s Fosterville Mine, in addition to other exploration successes such as this year’s bonanza grade intercept drilled by E79 Resources at its Happy Valley Property, has brought a renewed focus to an area of Australia that has had millions of ounces of placer gold mined from its earth over the last century.

Outback has a strong management team led by CEO Chris Donaldson and Chairman Craig Parry. The company has more than half of its current market cap in cash in its treasury. This cash will largely go into the ground in the first half of 2022 via drill programs at Yuengroon, Ballarat West, and Silverspoon. I expect the maiden drill program at Silverspoon, adjacent to Kirkland Lake’s Fosterville Gold Mine, to begin in mid-2022.

It’s important to stress that Outback does not need to raise money at the current low share price levels. In addition, shareholders can expect steady news flow over the coming months including:

- Diamond and RAB drill results from Yuengroon (drilling finished in October)

- Phase 2 drilling at Yuengroon (January/February)

- Maiden drill program at Ballarat West (March)

Steady insider buying from Outback management in the last few months helps to add confidence in the value available at recent depressed share price levels:

A C$12 million market cap does not do justice to the potential of Outback’s project portfolio and the quality of its management. While there is still a chance that Outback falls flat on its face again in 2022, from my vantage point buying Outback shares at $.20 is about as close to stealing as it gets and it is still legal.

Ridgeline Minerals (TSX-V:RDG, OTC:RDGMF) – Ridgeline was one of the sexy new gold stories that was introduced to the market in 2020. Ridgeline boasts an impressive Nevada precious metals exploration portfolio that includes the aptly named Carlin East Project next door to Barrick Gold’s massive multi-million ounce Carlin and Goldstrike Mines. Ridgeline shares have been in a precipitous decline since peaking at $.77 in June of this year:

RDG.V (Daily)

I believe the current valuation (C$17.5 million market cap) does not adequately value the potential that exists across Ridgeline’s project portfolio and its partnership with the two largest gold miners in the world (Barrick/Newmont JV called Nevada Gold Mines), the gold giants of Nevada, Barrick Gold (NYSE:GOLD, TSX:ABX) and Newmont (NYSE:NEM).

It doesn’t take a PHD geologist to understand that Ridgeline’s four Nevada projects are strategically located in ‘elephant country’ along two of the most prolific gold trends in North America; The Battle Mountain Trend, and the Carlin Trend.

Ridgeline completed a 2,272 meter phase two drill program at Carlin East in October and the company expects results in November/December. Meanwhile, a drill program at Swift ($20 million earn-in agreement with Nevada Gold Mines) is slated to begin any day now with Ridgeline expecting results to trickle in throughout Q1 2022.

Ridgeline CEO Chad Peters is particularly excited about the CRD (carbonate replacement deposit) potential of Ridgeline’s Selena Project located at the southern extension of the Carlin Trend. 2021 drilling at Selena intersected CRD type silver-lead-zinc-gold mineralization in three different holes including:

- Hole SE21-024: 10.7 meter grading 194.0 g/t grams per tonne silver (g/t), 0.3 g/t gold, 2.0% lead and 1.7% Zinc starting at 191 meters true vertical depth (“TVD”)

- Hole SE21-025: 44.2 meters grading 123.2 g/t silver, 0.17 g/t gold, 1.5% lead and 0.6% zinc starting at 232 meters TVD

The elevated lead and zinc mineralization in multiple holes at Selena is an exciting new development that supports the concept that Selena is host to a large mineralized system with potential to discover multiple deposit types across the more than 35 square kilometer project. Ridgeline believes that the elevated lead and zinc mineralization associated with higher-grade silver in holes 24, 25, and 27 from 2021 drilling may represent a distal metal zonation pattern to the known copper-gold porphyry system located approximately 1 kilometer west of the Selena property boundary.

A 5,500 meter drill program in Q2 of next year will test the conceptual CRD targets at Selena.

CEO Chad Peters tells me that Ridgeline will end the year with C$2.3 million in cash in the treasury. Ridgeline will have to raise money at some point in the 1st half of 2022, but Peters is not in a rush to do so with the share price at its lowest year-to-date levels and potential catalysts lined up at multiple projects over the next six months.

Ridgeline has a prime project portfolio in the best gold mining jurisdiction in the world. A partnership with the two largest gold producers in the world only serves to add validation to the quality of Ridgeline’s assets. I have used the recent share price weakness to begin initiating a position in Ridgeline and I intend to add to this position over the next couple months.

Trifecta Gold (TSX-V:TG, OTC:TRRFF) – Trifecta Gold has exploration stage projects in northern Nevada and the Yukon Territory of Canada. The company is focused on the Yuge Project in Nevada and the Eureka Project in the Yukon. Trifecta is probably the simplest and easiest to understand proposition of the six companies in this year’s list, it is also the least liquid stock of the group with free trading float that is likely less than 30 million shares.

Five months ago, Trifecta closed a C$2 million financing at $.10 per share. That financing price gave Trifecta a market valuation of roughly C$8 million, based on yesterday’s closing share price of $.065 that valuation is down to C$5.2 million.

What has happened in the last five months to drop Trifecta’s market value by 35% you ask?

The answer is nothing that would warrant the decline in valuation. In fact, Trifecta completed surface exploration programs and trenching programs at Yuge and made the discovery of a new gold mineralized zone between the Columbia and Josie Zones at Yuge with a trench result of 17.7 meters of 2.34 g/t gold (including 2 meters of 6.49 g/t gold) in Trench I:

Yuge is a relatively early stage exploration project but Trifecta had impressive results from its maiden drill program in early 2021. Drill results from the maiden program at Yuge included hole YU-21-02 at Columbia, which intersected high-grade gold in multiple intervals including:

- 3.63 grams per tonne gold (g/t Au) over 15.24 meters (including 15.5 g/t Au over 1.53 meters and 6.38 g/t Au over 1.52 meters) from hole YU-21-02;

- 2.89 g/t Au over 9.14 meters (including 6.74 g/t Au over 1.52 meters) also from hole YU-21-02.

Hole 21-02 intersected two zones of gold mineralization associated with arsenopyrite and quartz veining within a broader interval that averaged 2.27 g/t gold over 38.1 m. This hole was 100 meters from the only known historical drill holes on the property, which reportedly graded 9.60 g/t gold over 3.30 meters (DDH C2) and 5.14 g/t gold over 2.13 meters (DDH C3).

Trifecta shares have suffered along with the junior mining sector in recent months, and delays with procuring a drill crew in Nevada have not helped. The good news is that Trifecta has C$1.8 million in its treasury and management is very careful with shareholder capital; Trifecta has a G&A burn rate of roughly C$300,000 per year.

Trifecta CEO Richard Drechsler tells me that Trifecta will be back out at Yuge with a drill crew and an RC rig early in the new year. The plan will be to drill Columbia, Juanita, and also test the new discovery located between these two zones, 500 meters from the nearest drill hole.

Yuge is located in an area of Nevada known for high-grade gold mines (Getchell, Goldstrike, and Marigold). The potential that exists for Trifecta to further delineate the gold zones at Yuge, and then to potentially connect them, offers a very enticing proposition that the market is currently not giving much value. 1+ g/t gold near surface gold zones in northern Nevada are valuable, and in a strong gold price environment, could fetch significantly more value than Trifecta’s current C$3.4 million enterprise value.

TG.V (Daily)

Trifecta shares closed trading on November 25th, 2021 at a fresh year-to-date low

Trifecta’s Eureka project in the Yukon is at least as exciting as Yuge with the potential for the discovery of the hard rock source of the millions of ounces of placer gold that has been mined historically from gravel in the streams that Eureka surrounds. In 2018, 10,000 ounces were reportedly recovered from a placer pit near the Allen Showing, and in 2021 a 60,000 ounce non-compliant placer resource was estimated on the north side of Eureka Creek by local miners. Results from Trifecta’s 2021 exploration program at Eureka are still pending.

Eureka is located in a prolific placer mining area of the Yukon where there is a lot of gold. The placer gold in the nearby streams came from a hard rock source at a higher elevation. Trifecta believes that source is most likely to exist in the form of epithermal veins near the Eureka Dome on Trifecta’s claims. Eureka has a lot of potential and the fact that it is a #2 project for Trifecta demonstrates the quality and potential of Trifecta’s project portfolio.

Trifecta is a strong buy at anywhere below $.10 per share but I would caution that Trifecta does not have a large trading float and often doesn’t trade a lot of volume. A strategy of steady accumulation on the bid is most likely to work over the next few weeks as those who bought at higher share prices book tax losses.

Vanstar Mining Resources (TSX-V:VSR, OTC:VMNGF) – Vanstar is another stock that is down nearly 70% in 2021. Vanstar holds a 25% interest in the multi-million ounce Nelligan Gold Deposit in the Chibougamau Gold Camp in Quebec. IAMGold (NYSE:IAG) holds the majority 75% interest in Nelligan (IAG can achieve an 80% interest in Nelligan by completing a feasibility study, Vanstar would then have a 20% ownership + a 1% NSR on the original 8 Nelligan claims), and IAG has been conducting a 9,500 diamond drill program at Nelligan that is currently underway.

Nelligan hosts an inferred resource of 3.2 million ounces of gold at an average grade of 1.02 g/t Au. The Nelligan deposit is open along strike to the west and at depth. 2021 drilling by IAMGold is intended to infill some of the known zones at Nelligan, then to step-out to extend the deposit along strike to the west:

Based purely on the fact that Nelligan is a 3.2 million ounce deposit grading above 1 g/t gold in one of the best mining jurisdictions on the planet I would guess that it’s worth at least $300 million, even without a feasibility study or permits. Obviously once a feasibility study is produced and mining permits are received that value could rise substantially (Victoria Gold has a similar size deposit in production in the Yukon at a significantly lower grade and its market cap is roughly C$1 billion).

Based on that limited knowledge, Vanstar’s ownership in Nelligan will likely eventually be worth much more than its current C$24.7 million market cap. Then I can add in an important detail: The 2019 inferred resource was based on a C$1650 gold price, therefore if the cut-off grade is lowered (perhaps from .5 g/t to .4 g/t) the resource could easily be at least 3.5 million ounces of gold. Additional drilling, including from IAG’s 2021 program currently underway, could also obviously increase Nelligan to well beyond the 4,000,000 ounce mark.

Multi-million ounce gold deposits in tier-1 mining jurisdictions are rare and Nelligan is one of these rare deposits. While IAG is in the driver’s seat at Nelligan, it’s important to understand that even if IAG completes a feasibility study Vanstar will be left with a 20% carried interest in Nelligan. This means that IAG will fund 100% of the capex and development expenses up to the commencement of commercial production. A 20% carried interest in a multi-million ounce gold mine with a well funded partner that is aggressively increasing production across its asset portfolio is an enviable asset to have.

Even using a conservative timeline to first production at Nelligan (7 years) I estimate that Vanstar’s ownership interest is worth at least double its current market cap. Not to mention that Vanstar has more than C$5 million cash in its treasury and has been hard at work exploring its 100% owned projects (Felix, Amanda, Frida, and Eva).

I will briefly mention that Vanstar’s Felix Project is on trend with Amex’s Perron Project in Quebec and Vanstar recently completed a 2,000 meter diamond drilling program. This program targeted two strong electromagnetic conductors that had never been drill tested. The results for this drill program are pending and expected to be released in the next month.

While drilling success at Felix would be sweet icing on the cake, the reality is that Vanstar shares offer deep value with only the Nelligan asset. While owning a passive carried interest in a multi-million ounce gold project may not generate the sort of exploration news flow that many junior mining speculators would like to see, the reality is that this sort of asset holds tremendous value and helps to reduce the risk of the rest of Vanstar’s exploration portfolio.

I am a buyer of Vanstar below $.50 per share and I have accumulated a starter position in recent weeks.

VSR.V (Daily)

Conclusion

I would like to remind readers that this list is intended as a list of ideas. All six stocks are trading at what I deem to be attractive valuations after having experienced varying degrees of disappointment in 2021. Judging by investor sentiment and current market valuations, investors have relatively low expectations for all six companies in 2022. The opportunity exists in seeing value where others don’t, and allowing for the possibility that the low expectations of November/December 2021 could give way to a renewed burst of optimism early in the new year. This optimism could be the result of tailwinds for the junior mining sector, or impressive results from the individual companies, or both.

I would not be surprised if at least one stock on this list delivered enormous returns (500%+) in 2022, and I also would not be surprised if a couple of the stocks on this list did not perform well (-50% or more) in 2022. That means that one should expect plenty of volatility and opportunities to ‘buy low and sell high’. Please do not risk money that you can’t afford to lose – it’s important to understand that junior mining shares regularly experience enormous swings in valuations, as the sector gyrates from being in favor to being terribly hated by investors, and then back again.

I see a lot of value on this list and value is usually generated by buying what others do not see much value in, and buying at low price levels. I have put my money where my mouth is and I have a long position in every company on this list. In many cases you will be able to buy at lower prices than I have bought.

Do your own due diligence, it’s your money and your responsibility.

Disclosure: Author owns shares of all six companies on this list (Angold Resources Ltd, Elevation Gold Mining Corp, Outback Goldfields, Ridgeline Minerals Corp, Trifecta Gold Corp, and Vanstar Mining Resources) at the time of publishing and may choose to buy or sell at any time without notice. Author has been compensated for marketing services by Trifecta Gold Ltd.

______________________________________________________________

Disclaimer:

The article is for informational purposes only and is neither a solicitation for the purchase of securities nor an offer of securities. Readers of the article are expressly cautioned to seek the advice of a registered investment advisor and other professional advisors, as applicable, regarding the appropriateness of investing in any securities or any investment strategies, including those discussed above. Angold Resources Ltd., Elevation Gold Mining Corp, and other companies discussed in this article are high-risk venture stocks and not suitable for most investors. Consult company SEDAR profiles for important risk disclosures.

EnergyandGold has been compensated for marketing & promotional services by Angold Resources Ltd. and Elevation Gold Mining Corp. so some of EnergyandGold.com’s coverage could be biased. EnergyandGold.com, EnergyandGold Publishing LTD, its writers and principals are not registered investment advisors and advice you to do your own due diligence with a licensed investment advisor prior to making any investment decisions.

This article contains certain forward-looking information and forward-looking statements within the meaning of applicable securities legislation (collectively “forward-looking statements”). Certain information contained herein constitutes “forward-looking information” under Canadian securities legislation. Generally, forward-looking information can be identified by the use of forward-looking terminology such as “expects”, “believes”, “aims to”, “plans to” or “intends to” or variations of such words and phrases or statements that certain actions, events or results “will” occur. Forward-looking statements are based on the opinions and estimates of management as of the date such statements are made and they are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed by such forward-looking statements or forward-looking information, standard transaction risks; impact of the transaction on the parties; and risks relating to financings; regulatory approvals; foreign country operations and volatile share prices. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Actual results may differ materially from those currently anticipated in such statements. The views expressed in this publication and on the EnergyandGold website do not necessarily reflect the views of Energy and Gold Publishing LTD, publisher of EnergyandGold.com. Accordingly, readers should not place undue reliance on forward-looking statements and forward looking information. The Company does not undertake to update any forward-looking statements or forward-looking information that are incorporated by reference herein, except as required by applicable securities laws. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SEDAR.com for important risk disclosures. It’s your money and your responsibility.