Jericho Oil (TSX-V: JCO, OTC: JROOF) continues to execute on its strategy of utilizing strategic acquisitions to build a formidable mid-tier Oklahoma focused oil producer. On Wednesday (September 6, 2017) Jericho closed its largest acquisition to date, an acquisition that gives Jericho an interest in more than 9,000 acres right in the heart of the STACK (a prolific area of energy-development interest in Oklahoma which stands for Sooner Trend Anadarko basin Canadian and Kingfisher counties). Once again Jericho pulled off its latest acquisition by tapping into its team of strong financial backers (Breen Family, Sam Belzberg, Mike Graves) without spending a penny on finder’s fees or commissions. Energy & Gold was able to speak with Allen Wilson (President, Jericho Oil) and Adam Rabiner (Director Corporate Communications, Jericho Oil) last week to get the full scoop on the deal and some excellent insights as to where Jericho is heading over the next several months.

Scott Armstrong: Please tell us about this latest acquisition by Jericho which looks to be quite exciting and potentially transformative for the company.

Allen Wilson: We are excited because we’ve been working all year on it. I think we’ve looked at, in the last 15 months, about 25 acquisitions. But we’re pretty disciplined, so if we get to the finish line and they’re not what we need it to be, the expression is: ’Know when to hold them. Know when to fold them.’ You’ve got to fold. The emphasis around this is, currently in the United States, two big plays. There’s the Eagle Ford and Permian basin in Texas and the SCOOP and STACK in Oklahoma.

The way we’ve built Jericho so far over the past couple of years is buying production, building up our revenue, building up our value, showing we can make money and building a team. That’s all well and good, and obviously it actually makes sense, but investors are also looking for a little more sex appeal- a pot of gold at the end of the rainbow. And working into a bigger play like the STACK, it offers that for shareholders. But, you’re gonna do better if you spend a couple of years building your company and have the team to execute on it.

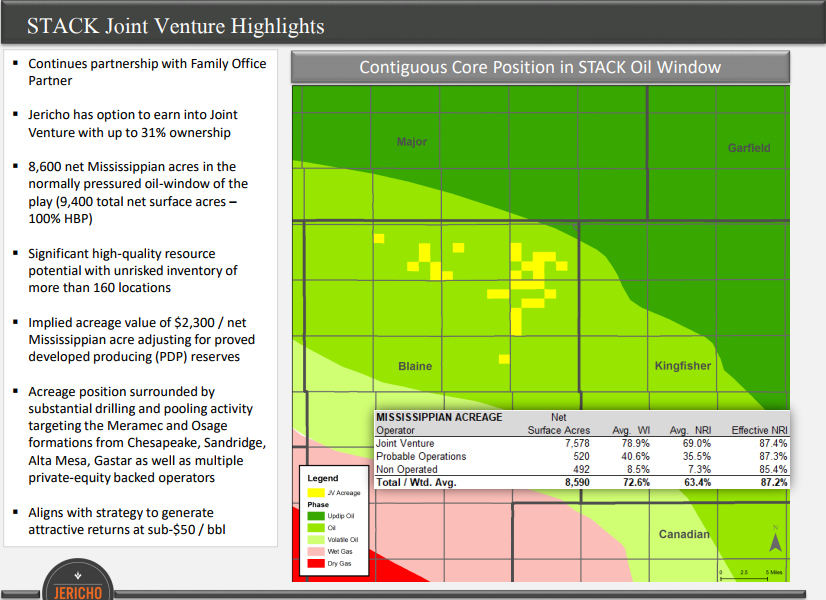

So this deal, which the full details of everything will be announced when we close (the deal closed Sept. 6, 2017). We had looked at the deal for a number of months, and we think we’ve negotiated a super price on it. For example, one company has just gone public on a $16,000 per acre evaluation, and the going price for acreage is around $10,000 an acre. So, for us to be able to secure a decent chunk of land at $2,300 an acre, it’s gonna represent really good value.

There’s a ton of activity in the area; and importantly for us, this particular piece is good for a junior company because of two reasons. The first thing is the whole acreage package is held-by-production from legacy wells. Why is that important? Some of the other packages we looked at had leases expiring in 2017 and 2018, so it means we’ve got to do work on them and spend a bunch of money on them- Which is fine. You don’t want to be scared of that, but services are at a premium right now and it’s hard to get drillers. So you don’t want that kind of pressure, that kind of gun to your head, as a small company. So, held by production.

The other beautiful thing from an economic standpoint on this acquisition are that the royalties on it are 87.5%. In the old-school days of the ’70s and ’80s it was always a 12.5% royalty. In the modern world, if you look around, you see most people are paying in the 20% range and in the 17.5% range. That 8% difference is huge. So, here we have we’ve picked up a really sizeable parcel of land, it’s all held-by-production, and the NRIs are low in one of the hottest plays in North America. We really couldn’t be happier. I think when we get on the road after Labor Day, the holidays, into the summer and people start realizing it, we’re gonna generate a lot of interest. If you look around, there are very few juniors that are in the STACK, and I think you’ll see us grow our profile in the STACK because we’re not done here. I want to make at least two more acquisitions in the stack, and we’re pretty close on a couple of them.

To finance it, I intended to raise US$5 million, but as people saw what we’re doing you’ll see me raise about US$8 million, and it’s gonna be done by a handful of our subscribers — including three insiders. So, we’ve got three big players in our deal. You’ll see in the early warning report on the last financing where it’s held by a Mike Graves. The Graves family is extremely well-known in Oklahoma. The last company they built (Calumet Oil), they sold to Chaparral for US$510 million. They were looking to sink their teeth into something and it just so happened that some of the people I’ve been hiring over the past couple of years were involved in quite a few successful transactions that they were involved in. So, they like our team, and they wanted to get involved. They’re gonna become around a 17% holder of the company, which is great for us. Especially from an Oklahoma standpoint, it’s excellent.

The Breen family, our existing backers, are investing in this round as well and it will be a seven-figure number that they’re investing. And Sam Belzberg, another very supportive shareholder, is investing a significant amount as well. So, again, we are blessed. We’ve got a great shareholder base. They’ve always been there for us, and we want to close the deal. Everything will be wrapped up and closed in early September.

So, our goal going forward now would be to add on one more acquisition. NAPE is in February, which is the big annual conference. Like the PDAC is for junior gold stocks, this is the energy industry’s big conference. I really want to get our name out there billed as a STACK player. We expect to do one more acquisition in the Play this year and I think it gives us the next emphasis. Which is, from a marketing standpoint, to move from the venture to the TSX because if we get of size we want to get ourselves in the index, so I’ll probably, eventually have to take care of it and do appropriate financing (brokered).

So far we’ve done everything amongst the team here, which has been great. We saved a lot on commissions, and I think that’s beneficial to the shareholder. But, ultimately, the thing we lack is liquidity. It’s been a tough market for juniors, but if we are in a higher profile situation, being in the higher profile play, high profile exchange, people look at our record and financings, and look at what we’ve accomplished over the last two years with all the acquisitions we’ve made, I think we’ll get a lot of credit as our name gets out there. I think this is a big transformation for Jericho.

CEO Technician: How did Jericho come across this package, and can you give us a little color for people who are not super experts in the oil and gas industry, especially in the Oklahoma area. What is the STACK and why is it so important?

Allen Wilson: Firstly, although I started the company in Vancouver and we do have offices in Vancouver, where we do regulatory accounting, our main focus is Tulsa, Oklahoma. We’ve got over 40 people down there. So, we really are an Oklahoma company. We are in the area and sort of in every negotiation and every play, so our name is known. This particular play came to us. There’s a couple of ways you can find these. You can find these properties through auctions, which this wasn’t. There are also websites that put up property and people just list the property for sale, sort of a craigslist for oil companies essentially.

The other way is to be invited to the process. Because we have closed five or six transactions, our reputation is that although we’re small we’ve closed on every transaction we’ve been a successful bidder on. That indicates that we’re a real player; a lot of people get there,and then they can’t get financing at the end, and it falls apart. So, we got invited into this process by being there for a couple of years, and I think our local presence is the key. You have to be local to get into these deals.

The STACK is the Sooner Trend and Anadarko basin, Canadian and Kingfisher Counties. It’s a long way to say it, but the STACK play is especially important for economics because, as oil dropped from 95 down to 30, people were looking for truly STACK plays. What a STACK play means is that when you drill a well, you’re going through multiple zones. If you drill a well, you’ve got four, five, or six chances to make that well work. You’re not just going after one single target.

And also, the STACK is really nice because it is very oil rich. When you drill for oil, you tend to get water, and it’s a big deal what the water to oil ratio is. The STACK is very oil rich. What this ultimately means is, economically, if oil is in the $40-45 price range you can still make money out of it, and that’s why you can get companies in there. Newfield, Marathon, and Devon are the big players in the SCOOP and the STACK, and they have big, massive acreages.

CEO Technician: Tell us about your existing property packages and what you’re doing with the stuff you acquired last year? How would you summarize this latest acquisition in the SCOOP?

Allen Wilson: We bought over 40 horizontals in the last couple of years, and what we’re going to do, and what we’re currently doing, (the first one is being fracked at the end of next week) is we’re going there and we’re simulating, or refracking them. If we’re successful on all those tests, then basically, it would validate everything we’ve been doing. So, we’re building that business in terms of building production.

This acquisition isn’t about production. It’s about building the drilling target’s acreage base and getting into a highly prolific, in terms of economics, place to be. So, we will be doing some sort of test well, or adding acreage to build a package. But, with the amount of activity there, what we’re gonna see is people drilling beside us as well.

Adam Rabiner: Devon put out a press release on July 11th. One of their STACK wells gets 6,000 barrels a day IP, just to put it in perspective how big these monster wells can be. And, their stock went up based on one well, even though they’re a very large company.

Allen Wilson: We’re already looking at a date for drilling a well, but on the interim, as I said, the news gets out we’ve been approached by one of our neighbors who wants to do a well. So, we’ll do some activity that will add value to our package, but we’ve also become very cognizant of what’s happening around us.

Scott Armstrong: How would you say this strategic partnership with the big three investors that you have — Breen, Graves and Belzberg — has sort of shaped how you have approached this year and maybe how you’re going to go forward over the next 6-12 months?

Allen Wilson: Structure is critically important when building a junior company. By having these family offices invested, it gives you the deep pockets and the time you really need to build the company. It’s not short-term money. Family offices invest for generations, and the first two investor’s viewpoint was that anything under a dollar was considered seed stock. That’s not the world I come from, but that was great to hear.

It’s shown over time that over these last two years one could say, “Okay, you guys aren’t very liquid.” But, in a time when everyone else is getting hammered, it shows what having those quality investors has meant. Every financing we’ve done has been an up round (higher share price than the previous financing). Shareholders don’t like to average down. To be able to deliver them slightly higher pricing, we gave them C$.45 last month, and we’re doing C$.48 this month. So, what it’s given us is tremendous ability to buy deals and withstand a downturn.

So, conversely, as we move forward and we talk about the future, we leverage that. We continue to bank on their support, and they’ve invested in multiple rounds. But as they become bigger shareholders, you know, your shareholders are your best promoters. The world that they can get us into, the doors they can open up for us, is incredible.

Because of Ed’s (Edward Breen) stature; he’s currently merging Dow and DuPont and he’s a director of Comcast. —If we get to a senior exchange (TSX), I think we can leverage his blue chip credibility to give us that little extra step up, and I’ve used our shareholders’ credibility in transactions. You know, I’ve phoned banking deals that Marathon was in, or a big name was in, that they wouldn’t take our call. We’re a little two-year TSX company and to be able to use our shareholder’s names, to be able to get that door open, has been helpful. So, we’ll get to leverage that.

These shareholders have all invested for one reason; For example, Mike Graves. Let’s say he owns 17% of the company, he’s gonna have, let’s just call it, 17 million shares. Our stock does 30,000 shares a day volume. He needs to do what he did back in ’06 and ’07 and help us get bought. So, having guidance from someone who’s done it multiple times, and the pockets to do it, it’s a unique position for a junior. We’re very fortunate where we’re at.

CEO Technician: To be clear, you’re gonna do horizontal wells on this new STACK play, right? And if so, how much will it cost you? What’s the average cost to do a horizontal well in Oklahoma right now?

Allen Wilson: So, I could tell you we can do one on our existing properties for $2.5 million dollars right now, but some of these wells in the STACK have been as high as $6 or $7 million. So, I can’t give you a definitive answer until I tell you what well we’re gonna drill.

CEO Technician: I think that’s a great point that you’ve made about you guys haven’t had to go to the market and use a broker to finance anything so far. And in a way, that’s a huge positive. Saves you a lot of fees. And in a way, it explains a little bit how the shares are trading, because if you don’t do a placement with a broker, they have no interest in backing your company and pumping you up and getting their clients involved in the stock, etc. And now, as you said, within the next six to 12 months, you see a vision of going to a larger exchange, going to the big board (TSX), and maybe doing a placement with a broker so you get the institutional backing. How else can Jericho build per share value for shareholders over the next year?

Allen Wilson: Sure. First of all, talking about timelines, that brokered financing, I would envision being in October. That’s the timing where we think that we can get in there in the fall so that it sets us up for a Q1 transition. The other thing I’ve been doing, if you’ve ever been involved with a company that’s moved to a senior exchange, you only do it when you’re ready and it’s gonna provide value. Because you lose some things. Being on a senior exchange is more expensive; the fees are higher and accounting is a big deal. Especially for a company as active as ours. Currently, as a junior, we get to file our quarterly in 60 days and our annuals in 120 days. When we go to the big board, the quarterlies are 45 days. So, this last quarter which we filed on August 15th, I’ve already got the team filing on the TSX schedule because we can’t misstep. We’ve got to make sure we’re there. The plan is well in place for that.

For us to add more value, we need to make more acquisitions, number one. We need to increase our land bank and drilling. And then the actual book value in terms of reserve reports, we need to develop our reserves and develop our company in such a way that increases the value of our reserves. Your reserves are how analysts may value you and also how anyone looking at you if they want to partner with you or buy a project will do so. Every year that we filed a reserve report, we have done that. We’ve increased our reserves dramatically. We will do some work on this STACK play that will give us reserves.

The three short-term ways are: 1. A brokered financing with the move to the exchange 2. further acquisitions 3. Building the core business to increase revenue.

We’re not at a stage where we’re gonna be declaring dividends. So, the revenue is important. It’s important to show we can make money at $40 and $35 oil, which we’ve been able to do. But most importantly, it’s to continue to prove up our land package, to validate our acreage position. We started with 2,000 acres. This acquisition will take us up to where we’ll have an interest in 79,000 acres. And we’ve done that in only two and a half years. I want to get to 250,000 acres, because then what happens, I ultimately believe oil prices will go higher, that has to be the premise of being an oil company (higher oil prices).

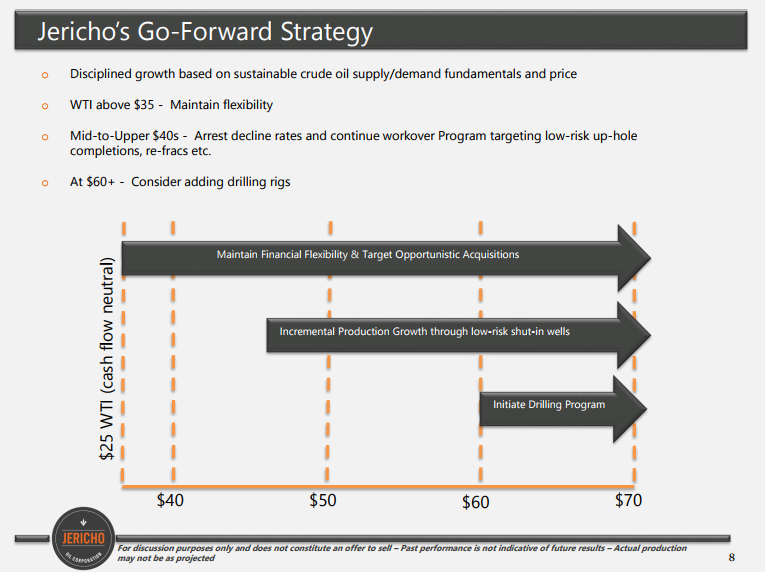

We build for $40 oil, but at $55 oil, two things happen; at $50 we drill because we figure that’s our entry point. And we’re not the only ones out there who think like this because as we get above $50/barrel the drilling rigs become hard to come by.

At $55 and $60 oil, what will happen is that these projects will not be available to be purchased. So it’s very important to buy them when the price is down here because people will then overpay for the drilling target. And we’re better to have those in our inventory. So, those are the things that we’re doing to add to shareholder value. That’s our strategy. We’re ultimately a land bank.

CEO Technician: What are your thoughts on oil here and the outlook for prices over the next 6 months? I saw some analysis the other day showing how the inventories in the US have dropped off quite sharply in the last couple of months while the price of oil has been fairly stable. Also, the rig count has sort of dropped again. This research was basically forecasting oil (WTI) to move up towards the high $50s over the next six months or so because of these facts. Do you have anything else you’d like to add on that?

Allen Wilson: Being an oil executive and being in the industry, I ultimately believe in the price of oil. I also understand it’s a cyclical business. Bullish isn’t the word I’d use. I just like the commodity. It’s the best cash flowing business in the world because you can sell your product every day of the year. The negative is, you’re a price taker, not a price maker. You take whatever price is given. If Apple makes a bunch of phones and they can’t sell them, they can drop the price. Not quite the same business. But I do believe in a higher oil price because of historically has been such a lack of reinvestment in existing fields.

And why is that important? Because every day that the oil companies produce oil, they have less oil that they’re gonna produce next year. They’re not replenishing their inventory. If you don’t drill, you don’t have inventory. It’s not endless. And it’s not like a light switch. You can’t just flip it on and start producing oil the next day. It’s a long lead time. Like, years. So, eventually, that’s gonna catch up. And when it catches up, you’ll see a spike in the oil price just like you saw a drop in the oil price. When that is, I don’t know. It does feel close because the fact that you’re pointing to right now.

I think the inventory drawn down though has been pared with dollar weakness because the oil price did stay stable for the last week or so, and then of course, the political tensions. There’s so much going on in the world that these are all your events that it’s hard to put into a model what’s gonna happen. But our model is very simple. We’re a junior company. We need to stick in a market that we know and can control, and the United States is an extremely well-known market. As much as I’m a proud Canadian, our market is a bit of a mess right now with the royalty situation and the governments up here. And say what you will about the US political landscape, I don’t vote in the elections, I don’t really have an opinion, but I can say the way that they voted has been very beneficial for our business, and so we want to take advantage of it.

Oklahoma, really, like Texas, depends on oil. It’s extremely important. And the EPA has historically been very hard on the oil industry in Oklahoma. Donald Trump took Scott Pruitt, former Attorney General of Oklahoma, who took on the EPA many times, and made him head of the EPA when he got in. I don’t know the logic in there, but if you’re an Oklahoman sometimes you take the cards you’re dealt right? And roll with them.

Jericho shares might be in a sweet spot right now as strong bids accumulate just beneath current levels while there are several ways investors can win over the coming months as Jericho ramps up its growth plans.

JCO.V (Daily – 1 Year)

JCO is beginning to break higher as volume builds, above the February peak at C$.74 the next stop for JCO shares will be C$1.00.

Jericho has built itself to be able to make money at sub-$50 WTI, however, a rising oil price will be icing on an already sweet cake for Jericho shareholders. I own Jericho shares and the company continues to be my top junior oil pick.

Do your own due diligence. It’s your money and your responsibility.

Disclaimer

The article is for informational purposes only and is neither a solicitation for the purchase of securities nor an offer of securities. Readers of the article are expressly cautioned to seek the advice of a registered investment advisor and other professional advisors, as applicable, regarding the appropriateness of investing in any securities or any investment strategies, including those discussed above. Jericho Oil Corp. is a high-risk venture stock and not suitable for most investors.. Consult Jericho Oil Corp’s SEDAR profile for important risk disclosures.

EnergyandGold has been compensated to cover Jericho Oil Corp. and so some information may be biased. EnergyandGold.com, EnergyandGold Publishing LTD, its writers and principals are not registered investment advisors and advice you to do your own due diligence with a licensed investment advisor prior to making any investment decisions.

This article contains certain forward-looking information and forward-looking statements within the meaning of applicable securities legislation (collectively “forward-looking statements”). Certain information contained herein constitutes “forward-looking information” under Canadian securities legislation. Generally, forward-looking information can be identified by the use of forward-looking terminology such as “expects”, “believes”, “aims to”, “plans to” or “intends to” or variations of such words and phrases or statements that certain actions, events or results “will” occur. Forward-looking statements are based on the opinions and estimates of management as of the date such statements are made and they are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed by such forward-looking statements or forward-looking information, standard transaction risks; impact of the transaction on the parties; and risks relating to financings; regulatory approvals; foreign country operations and volatile share prices. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Actual results may differ materially from those currently anticipated in such statements. The views expressed in this publication and on the EnergyandGold website do not necessarily reflect the views of Energy and Gold Publishing LTD, publisher of EnergyandGold.com. Accordingly, readers should not place undue reliance on forward-looking statements and forward looking information. The Company does not undertake to update any forward-looking statements or forward-looking information that are incorporated by reference herein, except as required by applicable securities laws. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SEDAR.com for important risk disclosures. It’s your money and your responsibility.