Fiore Exploration made quite a splash two weeks ago when it announced it had entered into a combination deal with GRP Minerals to form a new company named Fiore Gold. This is a transformative deal for Fiore Exploration in that the company moves from a Chile focused explorer (with its Cerro Tostado and Pampas El Penon projects) to a multi-continent producer/explorer with a goal of becoming a 150,000 ounce producer within the next couple of years while maintaining, and adding to, an impressive portfolio of exploration projects.

Energy & Gold caught up with Fiore Exploration CEO Tim Warman to get the real story on the deal and his new vision for Fiore Gold.

CEO Technician: How did Fiore come across the GRP deal and what made you so attracted to these assets?

Tim Warman: Fiore has been looking for a substantial, more advanced asset really since we started the company in the summer of 2016. I’ve been literally all over Central and South America and we’ve reviewed 50 or 60 projects over the last year. When we came across the Pan asset (GRP’s flagship gold project) a couple months ago we really liked the look of it based upon a couple of things. As you know it had been an asset that was part of Midway Gold, a company that had poured first gold on it in March of 2015 and by June of 2015 had gone bankrupt.

We looked at it and said “What happened back in the 2015 time period that didn’t work?” The more we looked into it, we got some of our experts in, one of our guys who’s the ex-COO of Gold Rock David Keough and we got another guy Tim Scott of KCA in Reno who ran Gold Fields Tarkwa heap leach mine in Ghana. So we have two guys who are very familiar with heap leach operations. The more we looked at it the more we realized that this was a mine that had gotten into trouble at ramp-up. Things didn’t go according to plan for Midway and due to the shortage of working capital they weren’t able to get over that hurdle, particularly during a time in which the gold price was fairly soft.

With a small injection of capital these assets have the potential to be the basis for a growing producer. It was this evaluation that was the real genesis of the Fiore/GRP transaction.

CEO Technician: Can you explain how Fiore decided to shift to North America? It wasn’t exactly a mandate to be focused on South America and it seemed like that was the focus for Fiore.

Tim Warman: The asset came to us from one of our colleagues in Vancouver, the guys from GRP had come in to see them and our colleagues in Vancouver thought these assets might be of interest to Fiore. We met the GRP guys a couple months ago and so that’s how we came across the GRP deal. From a geographic focus we have obviously been focused on Chile given that our flagship projects to date have been in Chile. We have also looked at some projects in Chile including a project with small scale production on the order of what GRP will have at Pan, but at the end of the day we felt the GRP deal was more compelling. We aren’t looking to head off to Africa or Asia but we are comfortable operating across both North and South America.

CEO Technician: What’s the value opportunity Fiore sees here? And how does this management team effectively manage what is now a pretty broad portfolio of projects including an operating mine?

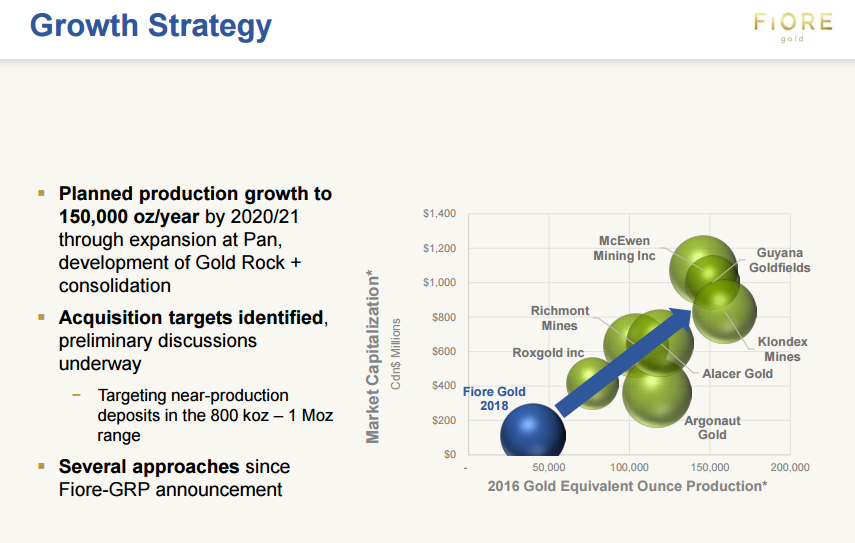

Tim Warman: We see the value proposition pretty clearly. The GRP portfolio has 2 key assets, one of which is Pan which is currently producing and which we think we can ramp up within a year (targeting 40,000 ounces of production in 2018, and 50,000 within a few years), the second key asset is the Gold Rock operation; Gold Rock is about 200 square kilometers of contiguous exploration ground and it’s anchored by a historical resource centred on the “Easy Junior pit” that was in production intermittently in the late 90’s by Echo Bay – there’s a historical resource estimate of 340,000 ounces Au indicated and 400,000 ounces Au inferred. We think that with some drilling we can update that resource estimate and add ounces there fairly quickly.

The EIS record of decision which is one of the key permitting milestones for Gold Rock is expected in Q4 2017. That’s continued to move forward so you can see that if we can get up to that 750,000-1,000,000 ounce resource over at Gold Rock we will have a very real scenario for another 50,000-75,000 ounce producing asset. So very quickly we would be moving up above 100,000 ounces of total annual Au production. We are also looking for another asset in that 50k-75k production range and if you look at companies which are producing in the 150,000 ounce range it’s not hard to find a bunch of companies in the $800 million to $1 billion market cap range.

So to us that’s a very logical way for us to add value for our shareholders. Of course it’s going to take a lot of exploration success for Fiore to move up to a $1 billion market cap. You know I think the last time anybody has done that was when we were at Aurelian back in 2008.

CEO Technician: In layman’s terms can you explain the Fiore/GRP deal to investors? What is Fiore receiving in this transaction and how much is Fiore paying?

Tim Warman: The terms are approximately .265 of each “New Co” share for each Fiore (F.V) share which values the GRP assets at about US$50-US$60 million. Now if you look at the NPV of those assets using a US$1275 gold price and a 5% discount you get about a US$50 million valuation on Pan alone which is a pretty attractive valuation for a project that’s already up and running. Fiore shareholders are getting a fully permitted and operating mine along with one of the largest contiguous exploration land packages in Nevada at 200 square kilometers on the Battle Mountain/Eureka Trend. For example Gold Standard Ventures (GSV.V) has a $500-$600 million market cap with the same size land package on the Carlin Trend so we think there’s a lot of upside there. Moreover, there is a lot of potential upside with the assets in Washington State (historical resource with 1.7 million ounces Au indicated) which are located 10 km from Kinross’ Buckhorn Mine & Mill Complex.

CEO Technician: The Buckhorn Mine & Mill Complex are moving into care and maintenance as we speak unless Kinross is able to source some feeder ore from a nearby project. This appears to be a very interesting opportunity for Fiore Gold.

Tim Warman: We’ve already had some preliminary discussions with Kinross about their Buckhorn Mill and Gold Eagle (the GRP asset in Washington State) is easily within truckable distance to Buckhorn. Gold Eagle is a bit land constrained which means it probably doesn’t work as a stand-alone asset without that mill, however, there is also some Hecla land surrounding Gold Eagle which they aren’t getting any value for. So I see a win/win/win scenario in which Hecla’s land, our Gold Eagle asset, and the Buckhorn Mill can work together to create value for all parties involved. This would be a longer term plan for Fiore Gold and it will require some discussions by those 3 companies involved. We also have good relations within Kinross because of the connection through Aurelian.

CEO Technician: Fiore Gold stands to be a much bigger company than Fiore Exploration was, how do you build out your management team and is Fiore Gold ready to optimize this much larger project portfolio?

Tim Warman: The first thing we obviously get to do is to get the deal done and that’s going to take a couple months as we work through the financing and the shareholder approvals and what not. In the meantime the GRP guys have a very good operating team at the mine site and a CFO who is very familiar with the US environment. I think there’s going to be a lot of good people out there who are going to be attracted to this kind of project and this kind of growth story. We’ve already had some guys call us up to express interest in working together, including some very talented people currently with the major producers. .

CEO Technician: What about the ore at Pan? Midway ran into some challenges there. Are you confident that the ore can be processed efficiently?

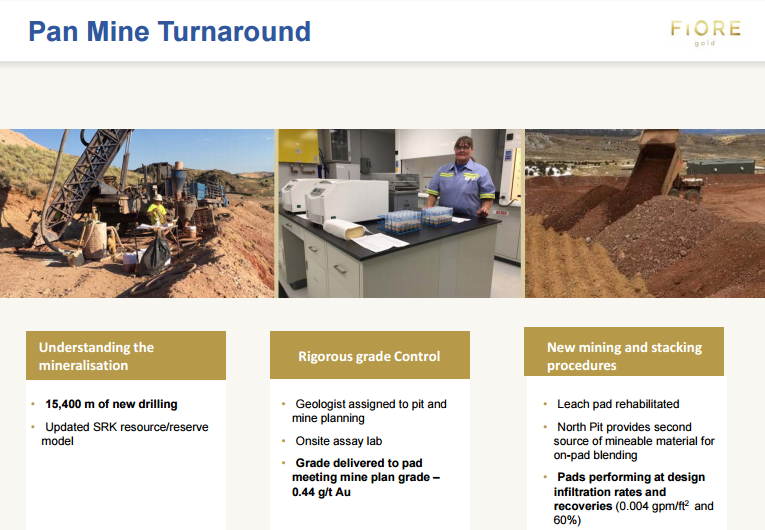

Tim Warman: The ore at Pan is not refractory in the sense that it doesn’t leach. The issue that Midway ran into at Pan was that they really hadn’t characterized the ore body properly. The geologic model and the resource model wasn’t predicting the amount of clay ore that they ran into and that’s a very common issue in the Carlin Trend. In fact it’s a very common issue in many projects across the world. When you have clay ore and you don’t have rocky material to blend it with what happens is if you put that clay material on the leach pad it ends up blinding out the leach pad; the cyanide solution that you’re putting on top of the leach pad can’t infiltrate the leach pad and extract the gold, it just ponds on the surface.

That’s what happened at Midway, they ran into a lot more of this clay ore than they were expecting. They only had one pit open so they didn’t have another source of ore that was more rocky which they could blend with the clay material to increase the permeability and they were also short of working capital. They didn’t have the cash on hand to get over those initial startup hiccups. What’s happened in the interim is that GRP has opened a 2nd mining pit which has very rocky ore material in it and they are blending that in the pad to create a much more permeable material. They started the re-mining and restacking back in March of this year and to date they are performing exactly to their design spec. They’re not getting the ponding, they’re getting good infiltration rates, good recoveries out of it, it’s operating as it was designed to.

GRP has completed a lot of operational improvements including 15,000 meters of new drilling to better understand the ore body which includes 127 new holes. They commissioned SRK to do an updated resource & reserve estimate, and feasibility study which should be coming out in the next couple of weeks. They’ve also done some additional met calculations to show what the leach curves are like on that and what the projected recoveries are like from that. On the operational side they’ve opened up a second mining face so they can get rocky material to blend on the pad. They’ve instituted a rigorous control on the blending strategy and they’ve implemented a much more effective plan to manage grade control; one of the problems which Midway ran into was grade control. I had never heard of a mine without a grade control lab on site, but anyway what Midway was doing was taking their grade control samples and shipping them off to an assay lab spending about $50,000/week on grade control assays and not getting them back in time. So they ended up putting a .3 gram/tonne ore on the leach pad instead of a .44 gram/tonne ore which was in their design. In the interim GRP has commissioned the assay lab, they’re doing the quick turnaround grade control assays. They’ve instituted a much more rigorous sampling procedure and they’ve put a geologist full time in the pit and he’s also on the mine planning team so there is a very good interaction between the mine planning team and the geological team

One of the main questions we had for our consultant at KCA was had they solved the overall grade control and percolation problem and his answer was yes, these new operational controls and strategies have sorted that out.

CEO Technician: What does Fiore do with its Chile assets now?

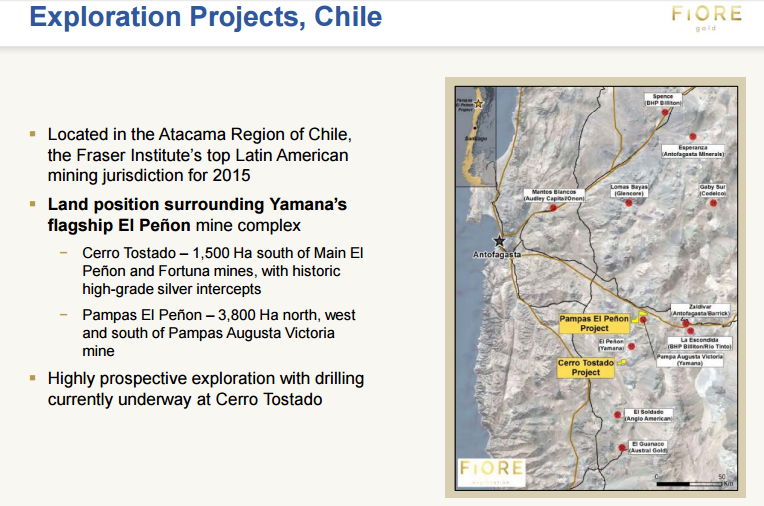

Tim Warman: We are drilling at our Cerro Tostado property in Chile right now, we’re on hole #4 and I’m expecting our first assays any day now. We are following up on some of the high-grade silver intercepts which had previously been drilled by SQM on the property. We will continue to explore our Chilean assets and see a lot of exploration upside there as we also do in Nevada.

The biggest takeaway from the conversation with Tim Warman is the confidence he has that the operational challenges at Pan have been solved. In addition, this is a deal that puts Fiore Gold on the map with a clear road map to eventually becoming a 100,000+ ounce/year producer. The Chile and Washington State assets suddenly become the icing on the cake for a company that will soon be able to fund its exploration budgets out of free cash flow. We would like to thank Tim Warman for his time and for clearly communicating his vision for Fiore Gold with our readers.

Disclaimer:

The article is for informational purposes only and is neither a solicitation for the purchase of securities nor an offer of securities. Readers of the article are expressly cautioned to seek the advice of a registered investment advisor and other professional advisors, as applicable, regarding the appropriateness of investing in any securities or any investment strategies, including those discussed above. Some of the stocks mentioned are high-risk venture stocks and not suitable for most investors. Consult the companies’ SEDAR profile for important risk disclosures.

EnergyandGold.com, EnergyandGold Publishing LTD, its writers and principals are not registered investment advisors and advice you to do your own due diligence with a licensed investment advisor prior to making any investment decisions.

This article contains certain forward-looking information and forward-looking statements within the meaning of applicable securities legislation (collectively “forward-looking statements”). Certain information contained herein constitutes “forward-looking information” under Canadian securities legislation. Generally, forward-looking information can be identified by the use of forward-looking terminology such as “expects”, “believes”, “aims to”, “plans to” or “intends to” or variations of such words and phrases or statements that certain actions, events or results “will” occur. Forward-looking statements are based on the opinions and estimates of management as of the date such statements are made and they are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed by such forward-looking statements or forward-looking information, standard transaction risks; impact of the transaction on the parties; and risks relating to financings; regulatory approvals; foreign country operations and volatile share prices. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Actual results may differ materially from those currently anticipated in such statements. The views expressed in this publication and on the EnergyandGold website do not necessarily reflect the views of Energy and Gold Publishing LTD, publisher of EnergyandGold.com. Accordingly, readers should not place undue reliance on forward-looking statements and forward looking information. The Company does not undertake to update any forward-looking statements or forward-looking information that are incorporated by reference herein, except as required by applicable securities laws. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SEDAR.com for important risk disclosures. It’s your money and your responsibility.