As the cyclical bull market in U.S. oil & gas which began in January 2016 progresses, mid-tier and major producers will need to replace their depleted reserves. In addition to shuttering a sizable chunk of existing production, the severity of the June 2014 – January 2016 cyclical bear market in the energy sector caused oil companies to bring new drilling exploration to a halt.

The huge drop in the rig count (from over 1,500 to below 400 in the continental U.S.) helped to rebalance the oil supply & demand dynamic and we are now beginning to see the global oil market move into deficit and the oil price has responded accordingly:

WTI Crude Oil (Weekly)

The 2+ year head & shoulders bottom is in the process of being completed with a breakout above the $54-$55/barrel area targeting a much larger move all the way up to the $70s. If this oil price recovery plays out investors who are well positioned stand to generate enormous returns.

The tremendous drop in exploration activity over the last couple of years combined with reduced care & maintenance budgets puts oil producers in a challenging situation as the oil price continues to firm up. In order to replace dwindling reserves oil producers will need to look to the market in order maintain production as their legacy wells move into the decline phase. It is far cheaper to purchase barrels of oil on the stock market than to drill for a new discovery and move it into production (drilling is costly and moving a new discovery into production can take years).

In 2017 shrewd energy investors will want to position themselves to get ahead of the game by owning shares in smaller oil e&p companies that will potentially become targets of larger firms when they begin the scramble to replace production & reserves. I have dug deep to find a handful of top notch small cap energy names that investors should seriously considering add to their portfolios to profit from the oil resurgence. This post highlights the first company on our list.

During a year in which most oil firms were downsizing, shuttering wells, and doing whatever it took to survive. One Canadian listed oil e&p junior, Jericho Oil (TSX-V:JCO) was completing several acquisitions while aggressively growing its production and proved reserve base, in partnership with a private family office.

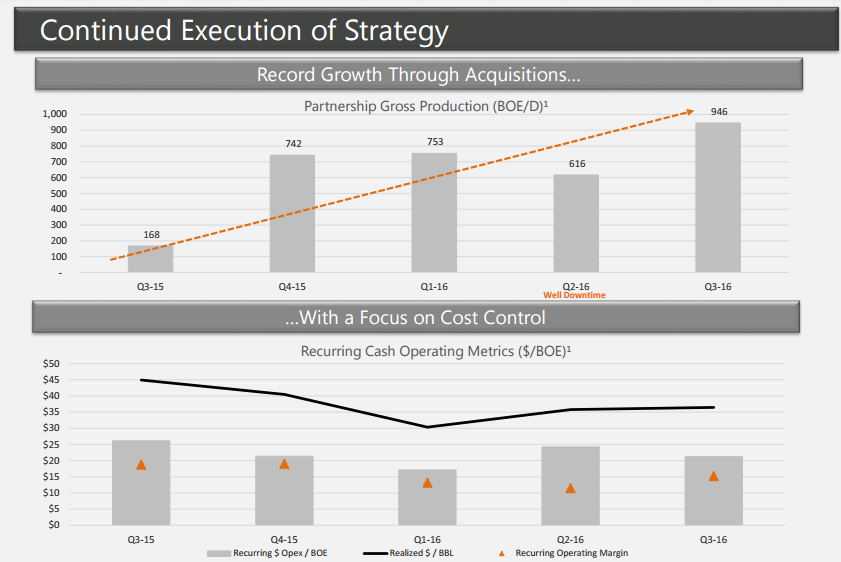

Jericho is an Oklahoma focused oil e&p company that completed a transformative year in 2016 in which the company successfully closed several acquisitions and significantly increased production (from less than 200 gross partnership boe/day in Q3 2015 to nearly 1,000 boe/day currently):

Jericho also secured a USD$30 million joint credit line at extremely favorable terms from East West Bancorp in a strong vote of confidence in the company’s health and management team from a thorough and rigorous financial institution.

Earlier this month Jericho raised C$5.39 million in a private placement which the company will use to continue expanding its Oklahoma operations in addition to putting the company in a position to close on a large acquisition which could vault JCO over the 1,000 boe/day producer threshold.

The question that most investors reading this article might ask is, why should I care about a sub-1,000 boe/day oil producer in Oklahoma? And that would be a fair question.

The answer is that Jericho Oil isn’t just any typical small cap oil e&p name. The company is strongly positioned with the strongest group of shareholders of any sub-C$50 million market cap company i’ve ever seen. In Jericho’s most recent equity raise (C$5.39 million) Samuel Belzberg, a legendary investor and an Officer of the Order of Canada and the Order of British Columbia, became the latest large investor backing Jericho with a seven-figure investment.

A couple of Jericho’s other significant stakeholders include:

-The Ryan D. Breen Trust which owns ~13.5% of JCO and is the sole 10%+ reporting holder. Ryan Breen is Jericho’s Director, M&A (Ryan’s father Edward Breen, is CEO & Chairman, DuPont; Director, Comcast; Director, Tyco)

-The Leo Group LLC (New Jersey based wealth management firm)

Since 2014, the company has raised ~C$24 million in private placements with no finder’s fees or commissions, which is a testament to Jericho’s strategy and the integrity of its management team.

Moreover, the joint $30 million credit line with East West Bancorp, a tier 1 bank, at extremely favorable terms (prime + 75 basis points) is a validation of Jericho’s financial strength; there aren’t many, if any, small cap oil e&p companies that have received credit facilities at such favorable terms in the last couple of years.

Jericho has a clear and focused strategy which seeks to acquire assets with “option value” through stacked–pays that become economic at higher prices or that have the potential to become economic at current prices through efficiency realizations. Moreover, the laser like focus on Oklahoma during one of the worst downturns in the oil sector during the last few decades has allowed JCO to develop considerable knowledge and expertise in this region while putting together a top notch team of talent.

“My goal is to not just get to 1,000 barrels, it’s 1,000 barrels and beyond.” ~ Allen Wilson, Jericho Oil, President & CEO

In a conversation with Jericho CEO Allen Wilson last week Wilson made several key points:

-

Wilson emphasized that Jericho continues to be patient and methodical in its strategy, however, the reason for owning the stock now is that there is likely to be a transformative event (large accretive acquisition, large move up in the oil price, discovery, etc.) that will generate a rapid move higher in the share price. This could happen in 2017.

-

Jericho has grand ambitions. 1,000 boe/day is just the first major milestone and Jericho is committed to eventually reaching a much larger scale (several thousand barrels per day) at which point JCO will become much more attractive to a mid-tier or major producer.

-

JCO is building a world class team that has unparalleled expertise in the areas of Oklahoma in which JCO is focused.

-

JCO’s land package offers tremendous exploration potential:

“We focus or purchase price on the PDP value of the asset, but we always consider the quality and number of potentially productive formations that underlie the acreage. Each of our assets has several stacked productive horizons including the Caney, Mays, Sycamore and Woodford. All of which are some of the up and coming plays being developed horizontally in Oklahoma.” ~ Allen Wilson

-

The incoming Trump administration in the U.S. is extremely favorable to the U.S. oil & gas industry, which offers a tailwind to the oil e&p sector as a whole.

As an investor I want to be exposed to the most potential possible at the cheapest possible price. At C$.47/share JCO shareholders are investing alongside some of the largest and most successful investors in the world in an oil junior that is cash flow neutral at $20 WTI. JCO’s sub-C$50 million market cap may not last long as the company grows production while continuing to optimize its legacy wells and drill some of the most attractive targets it has identified throughout its sizable land package.

JCO (Weekly)

At a relatively low valuation and with multiple ways in which shareholders can win JCO is an attractive speculation on the U.S. oil patch. The fact that JCO is also an opportunity to invest alongside successful world class investors is a bonus that is hard to pass up. As a trader and portfolio manager I also know that given JCO’s relatively light trading volume the stock could easily double or even triple with relatively modest buying (a few million shares) from investors who are motivated to accumulate a position.

Disclaimer

The article is for informational purposes only and is neither a solicitation for the purchase of securities nor an offer of securities. Readers of the article are expressly cautioned to seek the advice of a registered investment advisor and other professional advisors, as applicable, regarding the appropriateness of investing in any securities or any investment strategies, including those discussed above. Jericho Oil Corp. is a high-risk venture stock and not suitable for most investors.. Consult Jericho Oil Corp’s SEDAR profile for important risk disclosures.

EnergyandGold has been paid C$18,000 to cover Jericho Oil Corp. and so some information may be biased. EnergyandGold.com, EnergyandGold Publishing LTD, its writers and principals are not registered investment advisors and advice you to do your own due diligence with a licensed investment advisor prior to making any investment decisions.

This article contains certain forward-looking information and forward-looking statements within the meaning of applicable securities legislation (collectively “forward-looking statements”). Certain information contained herein constitutes “forward-looking information” under Canadian securities legislation. Generally, forward-looking information can be identified by the use of forward-looking terminology such as “expects”, “believes”, “aims to”, “plans to” or “intends to” or variations of such words and phrases or statements that certain actions, events or results “will” occur. Forward-looking statements are based on the opinions and estimates of management as of the date such statements are made and they are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed by such forward-looking statements or forward-looking information, standard transaction risks; impact of the transaction on the parties; and risks relating to financings; regulatory approvals; foreign country operations and volatile share prices. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Actual results may differ materially from those currently anticipated in such statements. The views expressed in this publication and on the EnergyandGold website do not necessarily reflect the views of Energy and Gold Publishing LTD, publisher of EnergyandGold.com. Accordingly, readers should not place undue reliance on forward-looking statements and forward looking information. The Company does not undertake to update any forward-looking statements or forward-looking information that are incorporated by reference herein, except as required by applicable securities laws. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SEDAR.com for important risk disclosures. It’s your money and your responsibility.