When David Einhorn speaks, I listen:

“Bottom-up: Short candidates are easy to find, but as noted above, the opportunity set on the long side is quite constrained. Most of the investment theses we have reviewed over the past several months can at best be described as late-cycle opportunities, with valuations that often ignore historical economic sensitivity. The operating (and in some cases activist) execution needed to achieve target results has to be rated at Triple Lindy difficulty level.”

Simply stated this market is stretched and the smart money has significantly pared back long exposure in recent months. Einhorn stated that during the 1st quarter Greenlight (his hedge fund) reduced net exposure from 30% to 14%. It is this reduction in net exposure and reduction of long positions by large hedge fund managers which also helps to explain some of the churning we have witnessed in US equities in recent months:

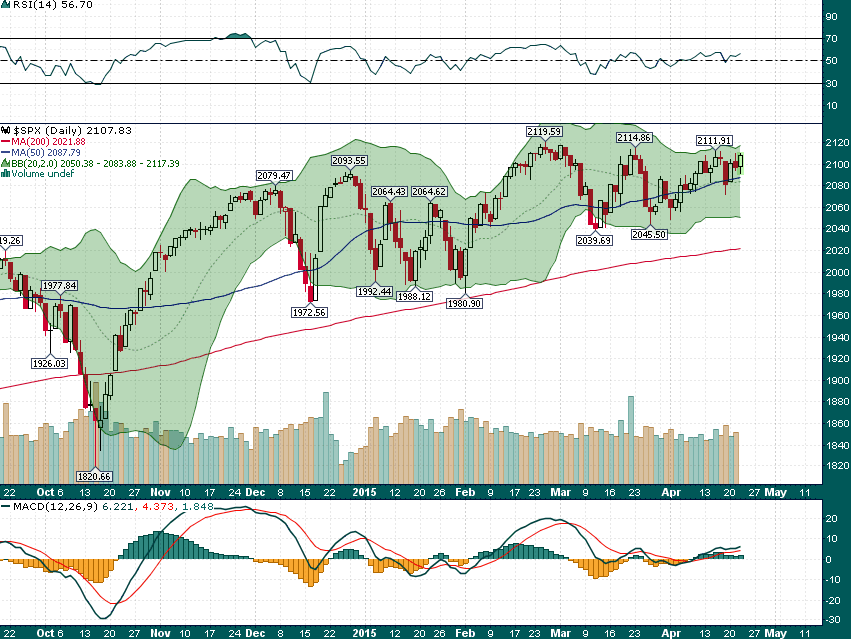

Since the beginning of the year the S&P 500 has essentially gone no where while churning within a 7% total range

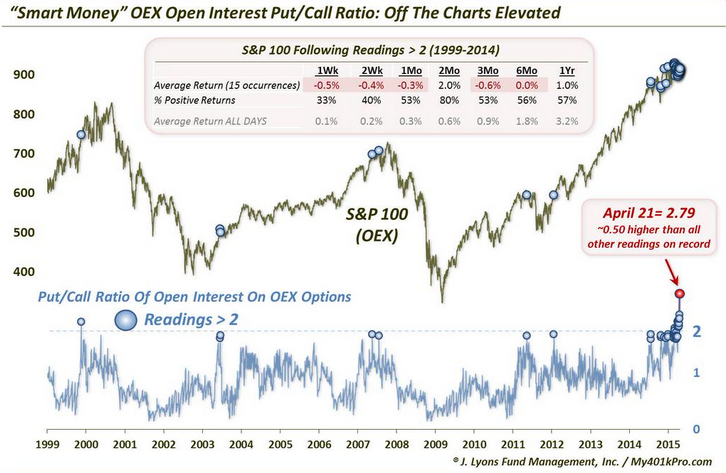

We are also seeing persistently high record levels in the OEX put/call ratio (the so called ‘smart money put/call ratio’):

While previous readings above 2.0 in the OEX put/call have often occurred near major market pullbacks/corrections, this ratio has proven to be far from an accurate short-term timing indicator. The recent cluster of extremely high OEX put/call readings is clearly off the charts and indicative of portfolio managers (PMs) remaining tightly hedged in anticipation of a market correction.

These PMs are likely to be right soon enough but just as they were in 2007, they are early. Get ready for an interesting summer…