Clayton Valley lithium explorer Cypress Development achieved a key milestone last week by entering into an agreement with Dajin Resources which could allow Cypress to obtain water rights at Dajin’s Alkali Spring Valley Lithium Property only 12 kilometers away from Cypress’ Clayton Valley Lithium Project. Cypress CEO Dr. Bill Willoughby commented “We look forward to working with Dajin on the exploration of the Alkali Spring Valley Lithium Property, and we appreciate their work to date towards obtaining related water rights. We particularly welcome the prospect to explore synergies with our Clayton Valley Lithium Project, which is only 12 kilometers away.”

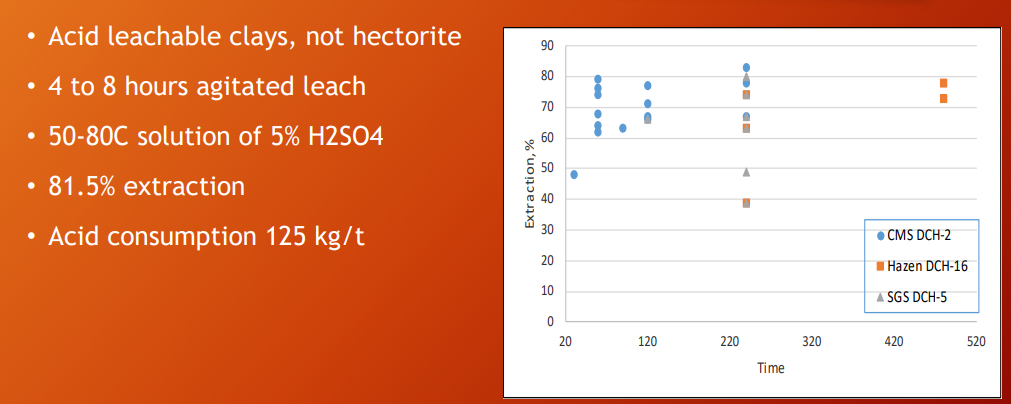

The key catalyst for Cypress over the next six months is the advanced metallurgical work that the company is currently working on. The goal of bench-scale met work over the next few months will be to confirm the US$4,000/tonne lithium-carbonate operating cost number that was used in the Cypress PEA with a higher degree of certainty. So far Cypress’ metallurgical work has generated recovery rates of 81.5% using an agitated leaching process that uses 125 kg of acid per tonne of clays.

The PFS metallurgy will concentrate on looking at the leaching characteristics of each individual geologic unit within the starter pit area and nailing those down. The chemistry is not in question, it is simply a question of the cost to get the lithium out of the clays. Cypress’ goal is to complete a preliminary feasibility study (PFS) by Q1 2019 which will go a long way towards confirming the economic viability of the Clayton Valley Lithium Project. A positive PFS will substantially de-risk the project and take it to the stage at which institutional investors might become comfortable making CYP shares a component of their portfolios.

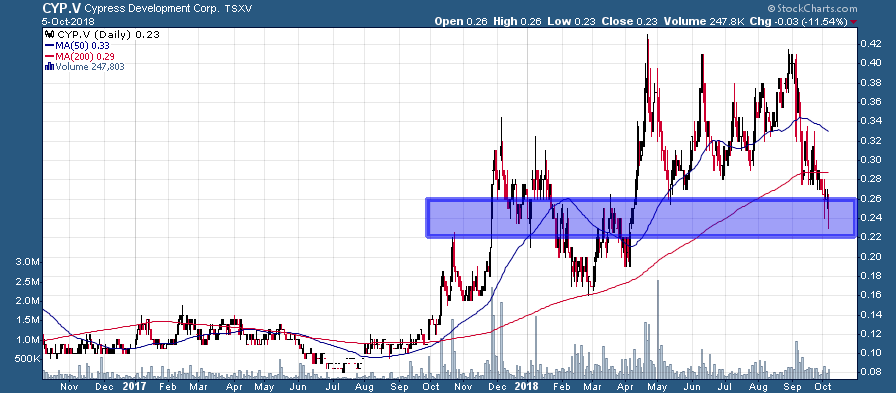

This next step of advanced metallurgy work will cost roughly C$1 million which will not be a challenge for Cypress to raise. After investors “sold the news” following the release of Cypress’ positive PEA, CYP shares have declined to a level of important support/resistance near C$.25:

CYP.V (Daily – 2 Year)

At C$.25 per share Cypress has a modest C$15 million market cap. I believe that this correction has run its course and traders have likely more than ‘priced in’ the coming C$1 million financing. Once the size and terms of the financing are confirmed I can envision a scenario in which CYP shares experience a relief rally. After all, once Cypress has completed a positive PFS the company will be in the final stages of development before mine construction (permitting, feasibility). A sub-$20 million market cap for a company with a $1+ billion project NPV(8) in the final mine development stages would be absurd to say the least.

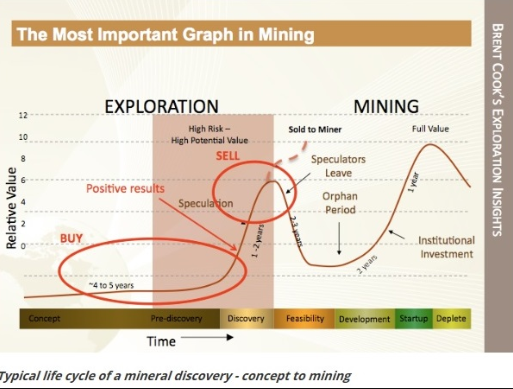

I’ll share “the most important graph in mining” simply as a reminder that Cypress is currently in the so called “orphan period”, but it is this stage of project development that offers some of the best investment opportunities:

Disclaimer:

The article is for informational purposes only and is neither a solicitation for the purchase of securities nor an offer of securities. Readers of the article are expressly cautioned to seek the advice of a registered investment advisor and other professional advisors, as applicable, regarding the appropriateness of investing in any securities or any investment strategies, including those discussed above. Cypress Development Corp is a high-risk venture stock and not suitable for most investors. Consult Cypress Development Corp’s SEDAR profile for important risk disclosures.

EnergyandGold has been compensated for marketing & promotional services by Cypress Development Corp so some of EnergyandGold.com’s coverage could be biased. EnergyandGold.com, EnergyandGold Publishing LTD, its writers and principals are not registered investment advisors and advice you to do your own due diligence with a licensed investment advisor prior to making any investment decisions.

This article contains certain forward-looking information and forward-looking statements within the meaning of applicable securities legislation (collectively “forward-looking statements”). Certain information contained herein constitutes “forward-looking information” under Canadian securities legislation. Generally, forward-looking information can be identified by the use of forward-looking terminology such as “expects”, “believes”, “aims to”, “plans to” or “intends to” or variations of such words and phrases or statements that certain actions, events or results “will” occur. Forward-looking statements are based on the opinions and estimates of management as of the date such statements are made and they are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed by such forward-looking statements or forward-looking information, standard transaction risks; impact of the transaction on the parties; and risks relating to financings; regulatory approvals; foreign country operations and volatile share prices. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Actual results may differ materially from those currently anticipated in such statements. The views expressed in this publication and on the EnergyandGold website do not necessarily reflect the views of Energy and Gold Publishing LTD, publisher of EnergyandGold.com. Accordingly, readers should not place undue reliance on forward-looking statements and forward looking information. The Company does not undertake to update any forward-looking statements or forward-looking information that are incorporated by reference herein, except as required by applicable securities laws. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SEDAR.com for important risk disclosures. It’s your money and your responsibility.