A couple of weeks ago I made a blog post on Treasury yields which was published on 321gold. The main premise of this post was that sentiment for rising bond yields (and in turn lower bond prices) was at an extreme and a tipping point was close at hand which would, at the very least, result in some mean reversion which would help reset market expectations. The day after this post was published yields spiked (10 basis points on the 10-year) and I received emails stating that I was “dead wrong” and that of course bond yields were headed “much higher.”

Since December 15th yields have consolidated within a tight range and then at the end of last week we began to see the first signs that a mean reversion was underway:

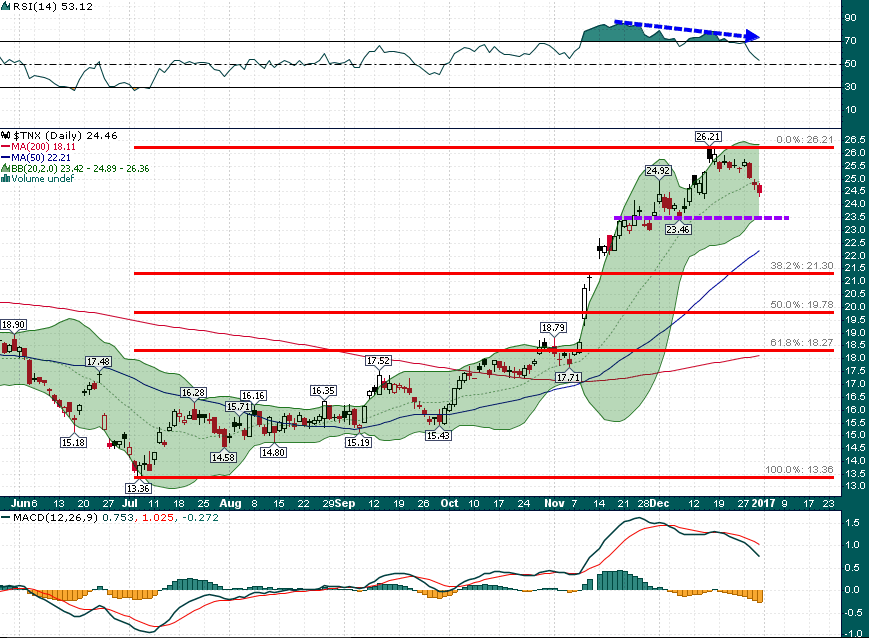

10-year Treasury Yield (Daily)

2.35% is the first downside reference point of interest, then 2.20% and the ‘gap fill’ and 38.2% Fibonacci retracement at 2.13%.

The November/December yields rally (+80 basis points on the 10-year UST yield since election day) priced in a big chunk of rising inflation expectations and economic growth under the incoming Trump administration. Moreover, when markets reach the sort of overwhelmingly one-sided sentiment such as we witnessed in the Treasury (interest rate) complex in mid-December the ‘hangover’ can be quite significant and prolonged.

Treasury markets may have entered a “show me” phase during which economic data will need to confirm that inflation is indeed rising and that President Trump’s economic proposals really do have teeth to them. The 2.62% yield level on the 10-year is now an important upside reference point, whereas, a breakdown below 2.35% would place the gap fill at 2.13% firmly in the sights.

DISCLAIMER: The work included in this article is based on current events, technical charts, and the author’s opinions. It may contain errors, and you shouldn’t make any investment decision based solely on what you read here. This publication contains forward-looking statements, including but not limited to comments regarding predictions and projections. Forward-looking statements address future events and conditions and therefore involve inherent risks and uncertainties. Actual results may differ materially from those currently anticipated in such statements. The views expressed in this publication and on the EnergyandGold website do not necessarily reflect the views of Energy and Gold Publishing LTD, publisher of EnergyandGold.com. This publication is provided for informational and entertainment purposes only and is not a recommendation to buy or sell any security. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SEDAR.com for important risk disclosures. It’s your money and your responsibility.