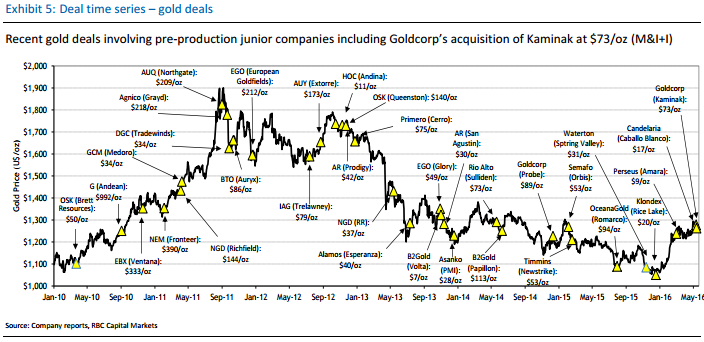

The gold mining sector is emerging from a five-year bear market that saw valuations collapse by nearly 90%. During the last few years, companies slashed exploration budgets and M&A within the sector dropped off substantially. Most gold miners were focused on surviving rather than growing or expanding their reserves.

We are beginning to see signs that M&A is heating up in the gold space. Notable deals include Endeavour Mining snapping up True Gold, Tahoe acquiring Lake Shore, Goldcorp buying Kaminak and Fortuna picking up Goldrock Mines.

Senior producers need to replace the reserves that they are continuously depleting. With the average grade of gold mines dropping substantially in the last decade and a global dearth of exploration activity, that’s becoming an increasingly challenging proposition for mega gold producers. This dynamic of dwindling reserves among the major producers, declining ore grades, and relatively low valuations across the sector has created a perfect storm for a new mergers & acquisitions cycle.

We have scoured the universe of mid-tier producers and top-quality junior explorers to generate a list of the top 10 takeover candidates that senior producers simply won’t be able to pass up in the next leg of the secular gold bull market. We used a few criteria (above a rising 50-day moving average, above C$50 million market cap, liquid stock with average daily trading volume above 250,000 shares) to narrow down the universe of junior/mid-tier gold explorers & producers before using our own fundamental analysis of a company’s resources and quality of management to generate a list of the top ten gold mining takeover prospects.

Without further ado, here is our top 10 list, in no particular order:

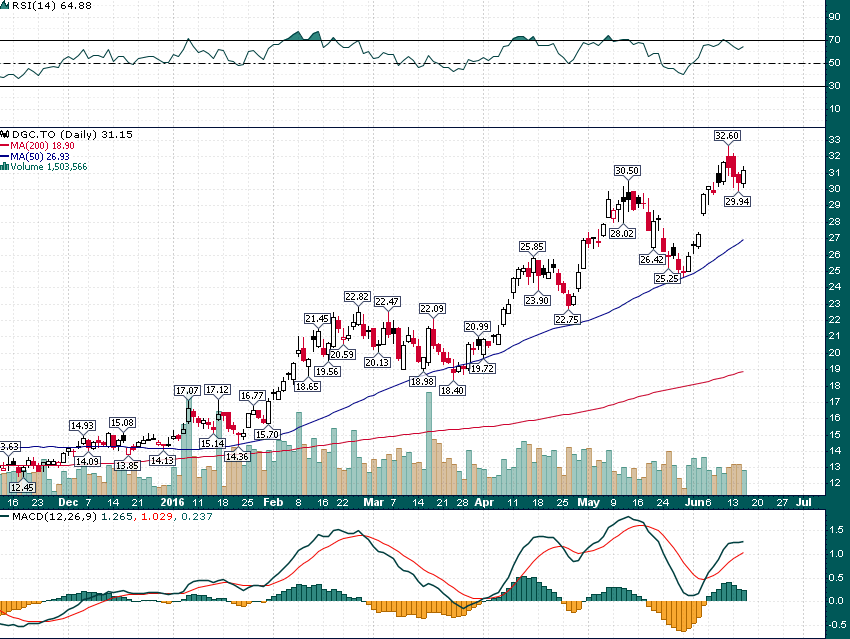

Detour Gold (Market Cap: C$5.4 billion) – Over 16 million ounces of gold reserves in the best mining jurisdiction on Earth, with estimated 2016 gold production of 550,000 ounces+ at all-in sustaining costs below US$900/ounce. If a senior producer wants to move the needle in terms of reserves and annual production, Detour will certainly be at the top of their list.

DGC.TO (Daily)

Beautiful uptrend with stair-step higher since November.

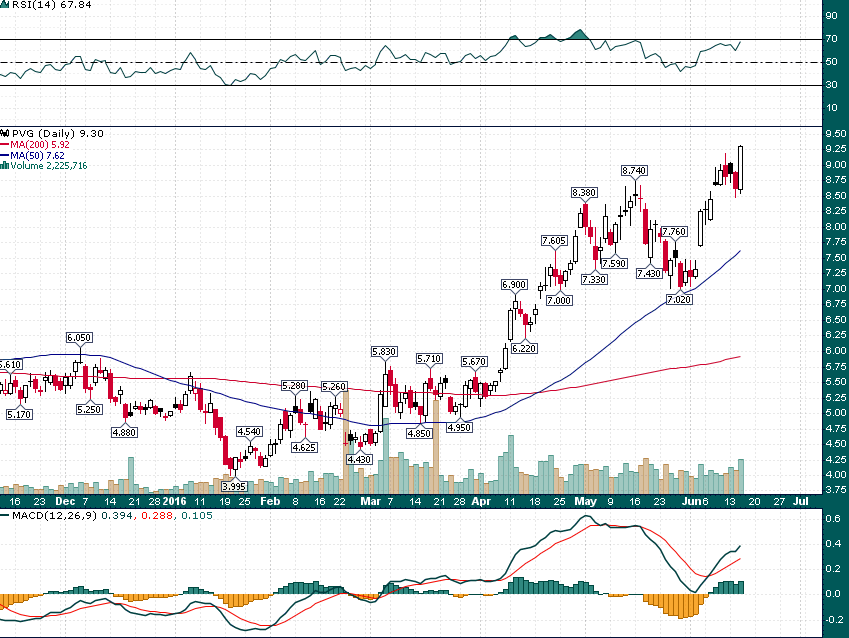

Pretium Resources (Market Cap: US$1.65 billion) – All eyes are on Pretium’s Brucejack Project in the Valley of the Kings in Canada’s ‘Golden Triangle’. Brucejack is a super-high-grade nuggety resource which is on schedule for commissioning in mid-2017. The only thing that seems to have prevented Pretium from already getting snapped up by a major is uncertainty around the continuity of the resource. That question should be put to rest with the current underground in-fill drill program. It’s clear that Brucejack is a mine and Pretium is on track to bring it into commercial production in 2017.

PVG (Daily)

Charts don’t get much nicer than this one – PVG is making multi-year highs on heavy volume. Textbook pullback to rising 50-day moving average in late-May found aggressive buying.

Sabina Gold & Silver (Market Cap: C$380 million) – High-grade open pits in Canada and one of the best cost profiles of any up-and-coming mid-tier producer; targeting 200,000+ ounces of annual production at an all-in sustaining cost of US$620/ounce. Sabina’s Back River project has district-scale exploration potential too. Expecting approvals from the Nunavut Impact Review Board around June 15. At that point, permitting becomes a formality.

Update: Sabina’s flagship Back River gold project has been stalled by a decision by the Nunavut Impact Review Board (“NIRB”) to recommend Sabina’s Back River gold project not move forward to the licensing and permitting phase until more information is provided, particularly with respect to caribou and climate change.

SBB.TO (Daily)

SBB has been undergoing a healthy consolidation on relatively light volume since staging a parabolic rally on heavy volume at the end of April.

Continental Gold (Market Cap: C$415 million) – Aiming to be in the lowest cost quartile of gold producers and further delineate a 10-million-ounce gold resource at Buriticá with a 20+ year mine life. The CNL story is all about permitting. CNL has one of the highest-grade gold resources in the world at its Buriticá Gold Project in Colombia, with grades north of 10 g/t gold.

CNL.TO (Daily)

Parabolic move in April gave way to multi-week consolidation. Didn’t even test rising 50-day moving average during pullback, looking to take out early May high.

Red Eagle Mining (Market Cap: C$155 million) – Colombia’s nearest-term producer. Red Eagle’s San Ramon mine is fully funded and permitted with initial production due to begin later this year. One of the cheapest targeted all-in sustaining cost structures in the sector at US$670/ounce all-in, set to reach full payback at San Ramon in under two years. Trading cheap relative to the peer group due to the smaller size of the San Ramon resource. However, significant exploration upside exists and the company has a second advanced-stage asset next in line in development.

RD.V (Daily)

More than tripled from January to May, pullbacks have consistently found support at rising 50-day moving average.

Torex Gold (Market Cap: C$1.72 billion) – Torex is targeting production of a massive 400,000 ounces of gold per year at an impressive US$616/oz all-in with an 8.5 year mine life at its El Limon Guajes mine in Mexico. In addition Torex has identified a second mine (Media Luna) on the same property with an inferred 7.4 million ounce resource. The scale of production at El Limon Guajes and potential upside offered by Media Luna makes Torex an interesting target. Recent violence and cartel activity in the region add a note of caution on this name, however.

TXG.TO (Daily)

Solid stair-step higher since January. Some signs of distribution (high volume down days) in the last week is something to keep an eye on.

Newcastle Gold (Market Cap: C$116 million) – ~5 million ounce gold resource in California. Newcastle is targeting 183,000 ounces of gold production per year at an all-in sustaining cost of US$855/oz.

NCA.V (Daily)

Phenomenal price action with volume following the trend higher as price continues to make new highs.

Belo Sun Mining (Market Cap: C$323 million) – Brazilian gold explorer on the verge of receiving its construction licence. 17-year mine life with average annual gold production of 205,000 ounces. 3.8 million ounces of reserves at 1.02 g/t.

BSX.TO (Daily)

Incredible rally from January to May with nearly a 500% move has given way to a light volume, low volatility consolidation. Support near C$.80 needs to hold or the open gap from April is likely to get filled.

Sandspring Resources (Market Cap: C$65 million) – One of the cheapest gold explorers on an enterprise value per ounce basis. Sandspring is committed to bringing forward its Toroparu Gold Project in British Guyana (South America) to production. A gold and silver purchase agreement with Silver Wheaton helps to fund and validate the Toroparu Project. Surrounding mining concessions offer substantial potential for exploration upside.

SSP.V (Daily)

Another beautiful chart that has continued to make new highs on rising volume.

Roxgold (Market Cap: C$494 million) – Roxgold’s flagship Yaromoko project is a world-class resource with high grades (over 10 grams per tonne) and good predictability and continuity throughout the resource. Roxgold has begun limited production at Yaromoko (roughly 40,000 ounces per year) while preparing to eventually throttle up to 100,000 ounces of annual gold production in 2017 with an initial 7.4-year mine life.

ROG.V (Daily)

Strong uptrend finding some resistance in the C$1.40s along with some momentum divergences – Support near C$1.20.

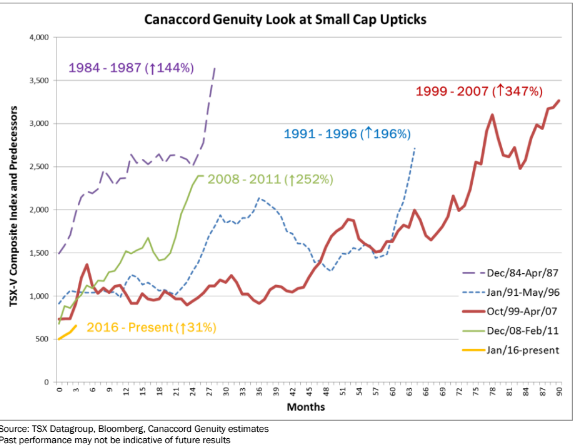

The gold mining sector has finally right sized its cost structure. However, after years of cost cutting and asset divestitures, the senior producers are ill-prepared for a renewed rising gold price environment. Consolidation in the sector is inevitable — it is not a question of “if” but “when”. Looking back at previous rallies in the junior/mid-tier gold space shows that the current rally in the S&P/TSX Venture composite index has not even come close to previous bull market cycles in terms of magnitude:

After yesterday’s Federal Reserve announcement pushing out the probability of rate hikes even farther gold has broken out to nearly 2-year highs above $1300/oz. It’s definitely not too late to raise exposure to a sector that is just beginning to ‘lift-off’!

Read Also: Gold Breaks Out as Fed Walks Back Rate Hikes

Disclaimer

The article is for informational purposes only and is neither a solicitation for the purchase of securities nor an offer of securities. Readers of the article are expressly cautioned to seek the advice of a registered investment advisor and other professional advisors, as applicable, regarding the appropriateness of investing in any securities or any investment strategies, including those discussed above. Some of the companies mentioned in this article are high-risk venture stocks and not suitable for most investors. Please consult a company’s SEDAR profile for important risk disclosures.

EnergyandGold.com, EnergyandGold Publishing LTD, its writers and principals are not registered investment advisors and advice you to do your own due diligence with a licensed investment advisor prior to making any investment decisions.

This article contains certain forward-looking information and forward-looking statements within the meaning of applicable securities legislation (collectively “forward-looking statements”). Certain information contained herein constitutes “forward-looking information” under Canadian securities legislation. Generally, forward-looking information can be identified by the use of forward-looking terminology such as “expects”, “believes”, “aims to”, “plans to” or “intends to” or variations of such words and phrases or statements that certain actions, events or results “will” occur. Forward-looking statements are based on the opinions and estimates of management as of the date such statements are made and they are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed by such forward-looking statements or forward-looking information, standard transaction risks; impact of the transaction on the parties; and risks relating to financings; regulatory approvals; foreign country operations and volatile share prices. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Actual results may differ materially from those currently anticipated in such statements. The views expressed in this publication and on the EnergyandGold website do not necessarily reflect the views of Energy and Gold Publishing LTD, publisher of EnergyandGold.com. Accordingly, readers should not place undue reliance on forward-looking statements and forward looking information. The Company does not undertake to update any forward-looking statements or forward-looking information that are incorporated by reference herein, except as required by applicable securities laws. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SEDAR.com for important risk disclosures. It’s your money and your responsibility.