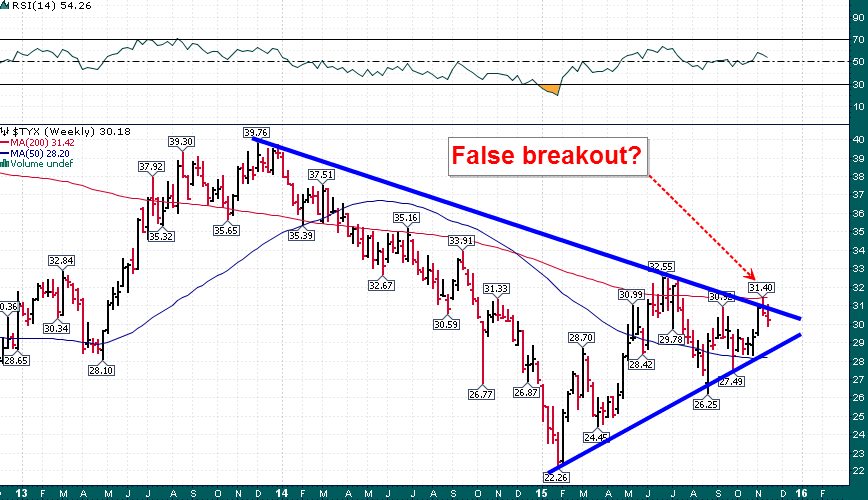

While the market is intently focused on whether the Federal Reserve will raise rates at its December meeting, the real action is taking place at the long-end of the Treasury yield curve. Two weeks ago the yield on the 30-year Treasury Bond rose as high as 3.14% before falling back down to 3.02% at the end of last week:

30-year U.S. Treasury Bond Yield (Weekly)

A potential failed breakout from the large triangular consolidation – from failed moves often come fast moves in the opposite direction.

While the Fed may be on the verge of raising the Fed Funds Rate, the technical backdrop and market participant positioning in Treasury Bond futures suggests that the Treasury yield curve is about to flatten further (long rates decline as short rates rise):

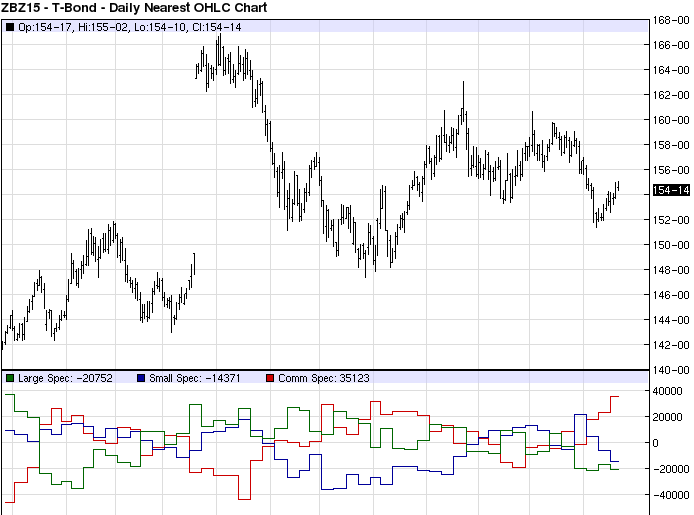

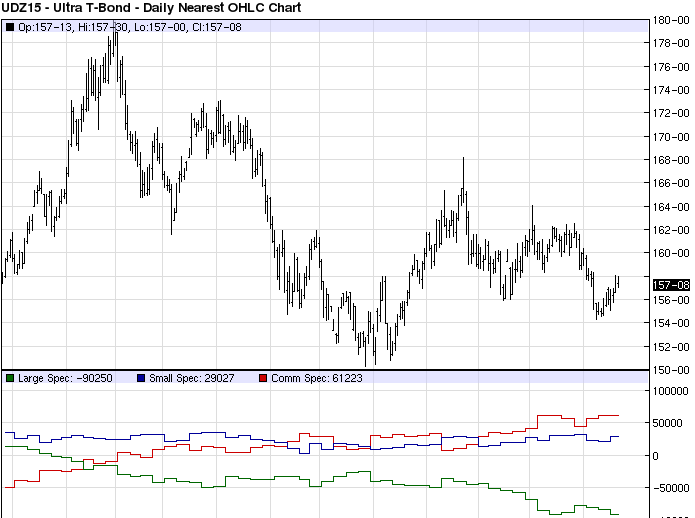

Commercial speculators in Treasury Bond futures (both the 30-year and Ultra) are at their largest net length since December 2013 (when yields put in a major top and just before Treasury Bonds had one of their best years ever in 2014).

In addition, we have also been seeing large buyers of call options in the Treasury Bond proxy exchange-traded fund TLT in the last week. The buying has occurred in multi-million dollar chunks and has been focused on the February & March expirations at the $123 strike price (~2% above current levels).

While the knee-jerk reaction is to sell bonds at the first sign of the Fed hiking rates, the smart money seems to have other ideas – a Fed tightening of policy could actually be bullish for bonds for a number of reasons including putting a cap on long-term potential economic growth.