From RBC:

“The reason for the recent poor performance of commodities as an asset class is two-fold: 1) fundamentals are bearish across most of the complex (which we will leave outside the scope of this particular analysis); and 2) there is a dreary cloud hanging over commodities, one that is a headwind at best, or a sort of “macro lid” on performance at worst. Broadly speaking, almost none of the classic reasons to hold commodities are present in any measure of strength at the moment. Firstly, we are in a commodity-negative environment with a strong dollar and low inflation expectations. In fact, the specific forms of inflation that commodities are meant to hedge against have been largely nonexistent recently. Additionally, commodities’ appeal as a diversifier has been significantly eroded by a pickup in correlations with other assets. Finally, intra-commodity correlations between major assets have picked up as well, compounding the poor performance of commodity beta. Each of these factors is at play, presenting quite a hurdle for the asset as a whole.“

Why don’t you tell us how you really feel? RBC makes a convincing case as to why commodities have been such a dreadful asset class for the last few years. However, all of this is backward looking. Commodity correlations with other asset classes have increased in recent months, in addition to a pick-up in intra-commodity correlations. A broad increase in correlations among asset classes is a typical phenomenon during market correction phases and has little bearing on what the future holds.

In terms of inflation RBC makes a good point that consumer/producer price inflation has been quite muted. However, yet again this is backward looking and does not indicate what the future may hold. Commodity prices are driven by supply and demand, meanwhile a growing global population is sure to require larger quantities of agricultural and industrial commodities to accommodate the tireless demand for higher quality of life.

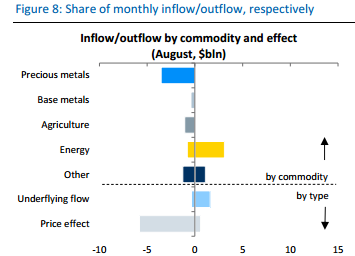

Precious metals have been one of the hardest hit commodity sectors both in terms of price and AUM (assets under management). The following diagram illustrates how a relatively normal monthly outflow caused an inordinate price move in precious metals during August:

This can be explained by a couple of factors (China fears, low investor participation during August historically, etc.), however, we are already seeing money flow back into the precious metals space and it appears that much of August’s outflows have been reversed in the past couple of weeks.

While RBC makes some valid points, this sort of backward looking dour analysis doesn’t tell us much other than that market participants and analysts alike are very negative on commodities right now. It doesn’t tell us what the future may have in store except for that if inflation does pick up and demand for commodities surprises to the upside there is a tremendous amount of pent up potentially energy available out there ready to bid up commodities anew.

It will be interesting to see how we view the timing of RBC’s latest commodities analysis one year from now…