In a relatively dour year for the junior mining sector, South32’s (LSE:S32) recent acquisition of Arizona Mining (TSX:AZ) stands out as a major bright spot. The C$2.1 billion acquisition (total equity value), which took place at a 50% premium to the market price (1 x NAV), clearly demonstrates South 32’s bullish long term outlook on the zinc market. Not only is South 32 paying a large takeover premium, but they are also now on the hook for roughly C$650 million of pre-production capex and a total of C$1.25 billion of life-of-mine capex. By any measure, this is a big bet by South 32, not only a bet on the quality of the Taylor Project, but also on the long term trajectory of zinc prices.

Moreover, production at Taylor isn’t set to begin on the project’s patented lands until 2021 (nearly three years from now), and only then will the company begin the federal permitting process on the remainder of its property package. The federal permitting process is expected to take a minimum of eight years, and more than likely as much as ten years.

To sum it all up, South 32 is making a multi-billion dollar long term bet on the zinc market. This is simply because regardless of how special the Taylor Project might be, without a strong zinc price over a lengthy period of time (decades), South32’s bet on Taylor won’t be a profitable one.

With Arizona now off the market, investors will begin looking for another Arizona-esque zinc play that will be next in line if we get a formidable wave of base metals M&A. Major mining companies are looking for large projects with the longest mine lives in order to justify sizable capex outlays and extended permitting timelines. This puts one zinc junior’s project at the top of the list:

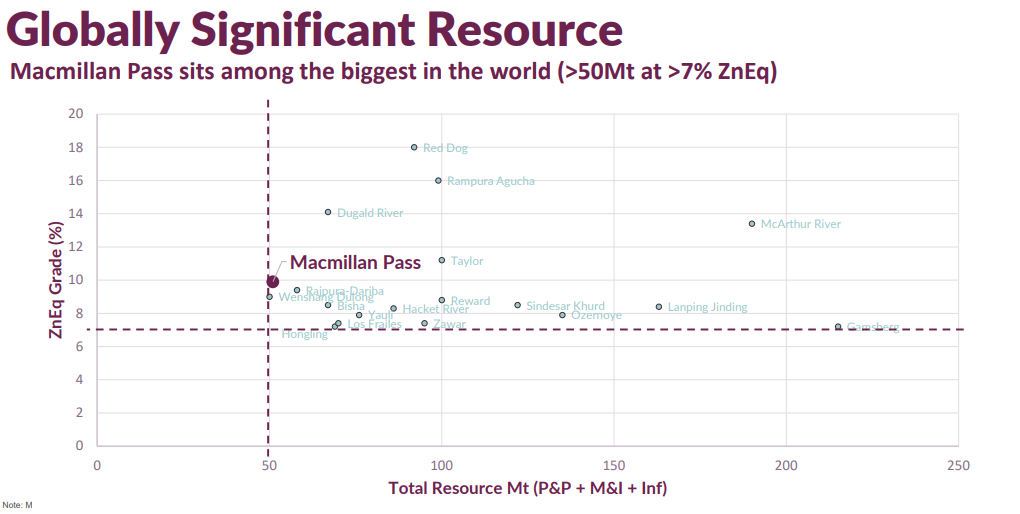

Based upon Fireweed Zinc‘s maiden PEA (released in May 2018), the Macmillan Pass Project offers an 18 year mine life and excellent economics including an after-tax NPV(8%) of C$448 million. After a nearly 40% decline since reaching an all-time high of C$2.12 in May, FWZ shares are trading at less than 10% of its after-tax NPV – A significant discount considering that Macmillan Pass is a world class project in an excellent jurisdiction.

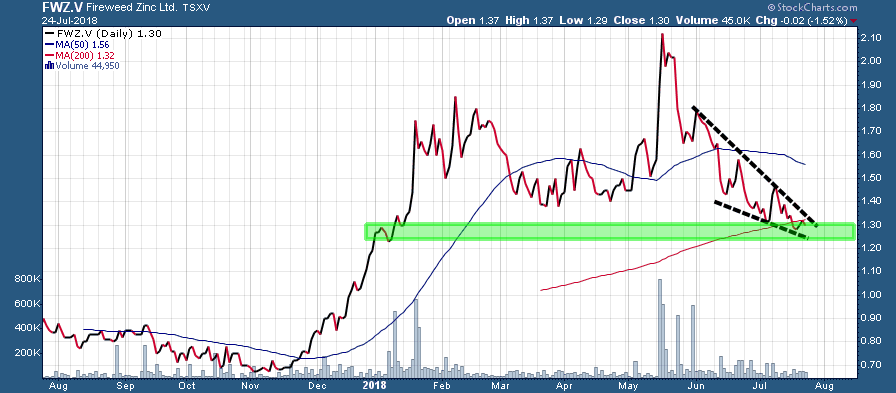

FWZ.V (Daily – 1 Year)

FWZ shares have returned to their February private placement share price of C$1.32 which also happens to be in the middle of a key support/resistance zone. A decisive move back above C$1.40 would be very constructive and offer a strong indication that the downtrend which began in May has reached its conclusion.

FWZ shares have returned to their February private placement share price of C$1.32 which also happens to be in the middle of a key support/resistance zone. A decisive move back above C$1.40 would be very constructive and offer a strong indication that the downtrend which began in May has reached its conclusion.

The recent sell-off (largely due to trade war fears impacting the base metals sector, and the fact that the February private placement came free trading during the last week of June) comes just as Fireweed is beginning three months of work at its Macmillan Pass Project in the Yukon. This summer’s work programs include 3 primary objectives, which could all significantly upgrade the project’s value and help to narrow the current huge discount to the project’s NPV:

-

Upgrade priority zones to M&I to de-risk project

-

Expand known zones through step-outs

-

Drill new targets and prove up entirely new deposits

This undervaluation represents a highly attractive investment opportunity, particularly because Fireweed is almost certain to increase the size and mine life at Macmillan pass, which will improve project economics. Moreover, FWZ’s maiden PEA included ~C$100 million for road upgrades needed to handle heavy trucks filled with ore for the portion of road from Mac Pass to Ross River (about 25% of the distance to the port at Skagway, Alaska). However, there is a very good chance that the territorial and federal governments will pay for these road upgrades. If this turns out to be the case, FWZ’s project capex will drop to roughly C$300 million and project economics will be significantly improved (basically the entire C$100 million for road upgrades flows into project NPV).

The real key for Fireweed this summer will be to continue to grow the size of Mac Pass and extend mine life. Speaking with Eric Coffin of HRA Advisory last week he noted that “By the time they’re done drilling this thing out it’s probably going to have a 25-30 year mine life and there’s simply not many things like that around.” and regarding this summer’s infill and exploration drilling he added “I really like what they’re drilling this summer and I expect some really good results out of Fireweed during the next 3-4 months. Where they’re positioning the drills right now I think we should see some really nice high grade intercepts.”

In a recent conversation, Fireweed CEO Brandon Macdonald emphasized that they aren’t just trying to blindly add size to the project, Fireweed wants to add higher value tonnes that can more significantly impact project economics; grade and location of additional tonnes matter tremendously for economics.

“We’re trying to target tonnes that are high enough grade that they really move the economics. If you take a look at the 18-year mine life laid out in the PEA and the grade kind of falls off after year twelve. So what we’d like to do instead of adding a year nineteen at the end is to insert a new year twelve and push the other years out to years 13 to 19. We’re not trying to slap years on the end of the mine life, we’re trying to wedge years in the middle which will more significantly impact economics.” ~ Fireweed Zinc CEO Brandon Macdonald

The key catalysts that could lead to an upward revaluation in Fireweed shares over the next 6-9 months are as follows:

-

Infill/step-out drilling adding size, grade, and potential new discoveries to the Macmillan Pass Project (steady news flow from summer exploration over the next 3-4 months).

-

Greater market appreciation of the value of Mac Pass now that South32 has acquired Arizona Mining’s Taylor Project.

-

Resumption of the base metals bull market after recent volatility largely caused by trade war fears.

Fireweed Zinc’s plan is to continue to improve all aspects of the Macmillan Pass Project while advancing the project to the point that it becomes a world class North American zinc/lead asset that becomes highly sought after by potential acquirers. At that point, macro variables such as the base metals cycle and federal government support with road improvements will become the icing on top of an already sweet cake.

Fireweed Zinc (TSX-V:FWZ, OTC: FWEDF)

Shares outstanding: 30.17 million

Fully diluted share count: 37.27 million

Current share price: $1.30

Current market cap: C$39 million

52-week range: $.67-$2.14

Disclaimer:

The article is for informational purposes only and is neither a solicitation for the purchase of securities nor an offer of securities. Readers of the article are expressly cautioned to seek the advice of a registered investment advisor and other professional advisors, as applicable, regarding the appropriateness of investing in any securities or any investment strategies, including those discussed above. Fireweed Zinc Ltd. is a high-risk venture stock and not suitable for most investors. Consult Fireweed Zinc Ltd.’s SEDAR profile for important risk disclosures.

EnergyandGold has been compensated for marketing & promotional services by Fireweed Zinc Ltd. so some of EnergyandGold.com’s coverage could be biased. EnergyandGold.com, EnergyandGold Publishing LTD, its writers and principals are not registered investment advisors and advice you to do your own due diligence with a licensed investment advisor prior to making any investment decisions.

This article contains certain forward-looking information and forward-looking statements within the meaning of applicable securities legislation (collectively “forward-looking statements”). Certain information contained herein constitutes “forward-looking information” under Canadian securities legislation. Generally, forward-looking information can be identified by the use of forward-looking terminology such as “expects”, “believes”, “aims to”, “plans to” or “intends to” or variations of such words and phrases or statements that certain actions, events or results “will” occur. Forward-looking statements are based on the opinions and estimates of management as of the date such statements are made and they are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed by such forward-looking statements or forward-looking information, standard transaction risks; impact of the transaction on the parties; and risks relating to financings; regulatory approvals; foreign country operations and volatile share prices. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Actual results may differ materially from those currently anticipated in such statements. The views expressed in this publication and on the EnergyandGold website do not necessarily reflect the views of Energy and Gold Publishing LTD, publisher of EnergyandGold.com. Accordingly, readers should not place undue reliance on forward-looking statements and forward looking information. The Company does not undertake to update any forward-looking statements or forward-looking information that are incorporated by reference herein, except as required by applicable securities laws. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SEDAR.com for important risk disclosures. It’s your money and your responsibility.