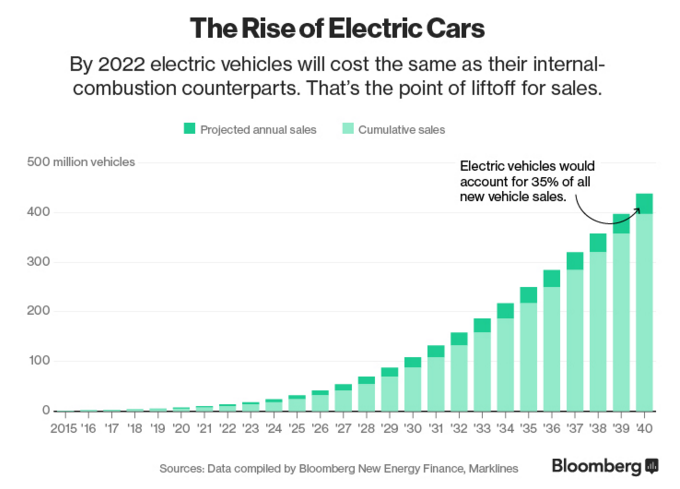

The lithium investment story is clearly one of the main investment stories of the first three months of 2016. With Tesla (TSLA) projecting 500,000 electric vehicle sales by 2020 and huge forecasts for global electric vehicle sales growth in the decades beyond the lithium-ion battery story is one that by all accounts looks to just be getting started:

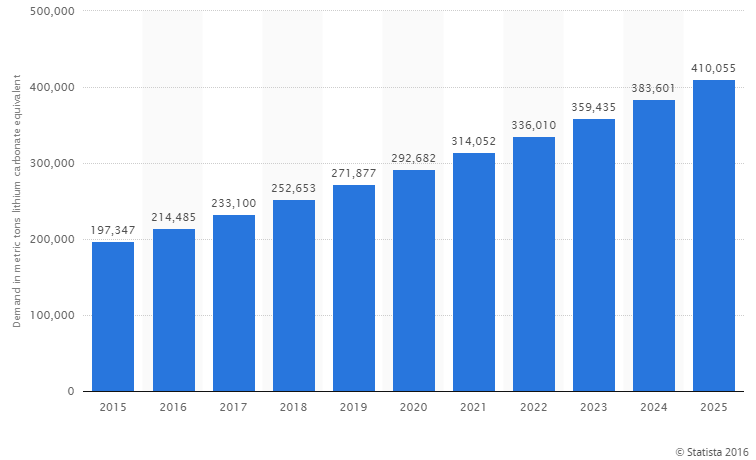

Forecasted lithium demand growth is nothing short of impressive and it this huge increase in demand that is fueling a mad rush to move forward potentially economic lithium resources across the globe:

It is this looming demand and the resulting investment inflows into the lithium space which has led to capital chasing a relatively small number of lithium pure plays. The lithium exchange-traded fund LIT has a large chunk of its net assets in chemical & mining conglomerates such as FMC and Albemarle due to the scarcity of lithium pure plays.

The net result we have witnessed thus far in 2016 are a number of small lithium explorers exploding higher with a handful of names enjoying 300%+ gains in the span of a few months:

Galaxy Resources (OTC-BB: GALXF)

Lithium X Energy (LIX.V)

Nemaska Lithium (NMX.V)

A large pile of available capital looking for the next big investment theme combined with a relative scarcity of investment vehicles with which to play the lithium story makes for an especially explosive situation in the lithium space.

The analogous investment theme I keep returning to is uranium between 2002 and 2007. Cameco (CCJ) was literally the only uranium pure play that institutional investors could access to play the nuclear energy theme in the early 2000s. Even Cameco had its limitations due to a large number of uranium supply contracts that extended out for many years which made it challenging for the company to fully benefit from the uranium bull market of the mid 2000s. However, this didn’t stop investors from bidding a multi-billion dollar market cap stock up 1500%+ between 2002 and 2007:

CCJ (2002-2007)

This is the power of a long term macro theme that has a limited number of investment vehicles with which investors can express a bullish view. P/E ratios, gross margins, and PEG ratios suddenly become much less important when portfolio managers absolutely HAVE TO get exposure to a sector because the FOMO (fear of missing out) is simply too great.

The most interesting part of the lithium story is that hedge funds are not in this trade at all, yet. While it’s hard to pinpoint with much certainty, it’s not too difficult to imagine valuations lifting ten-fold with even a modest amount of hedge fund capital flowing into the space. Lithium is quickly becoming the story of 2016 and it looks like it could just be getting started.

The article is for informational purposes only and is neither a solicitation for the purchase of securities nor an offer of securities. Readers of the article are expressly cautioned to seek the advice of a registered investment advisor and other professional advisors, as applicable, regarding the appropriateness of investing in any securities or any investment strategies, including those discussed above. Do your own due diligence and consult a licensed investment advisor prior to making investment decisions.

This article contains certain forward-looking information and forward-looking statements within the meaning of applicable securities legislation (collectively “forward-looking statements”). Certain information contained herein constitutes “forward-looking information” under Canadian securities legislation. Generally, forward-looking information can be identified by the use of forward-looking terminology such as “expects”, “believes”, “aims to”, “plans to” or “intends to” or variations of such words and phrases or statements that certain actions, events or results “will” occur. Forward-looking statements are based on the opinions and estimates of management as of the date such statements are made and they are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed by such forward-looking statements or forward-looking information, standard transaction risks; impact of the transaction on the parties; and risks relating to financings; regulatory approvals; foreign country operations and volatile share prices. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements and forward looking information. The Company does not undertake to update any forward-looking statements or forward-looking information that are incorporated by reference herein, except as required by applicable securities laws.