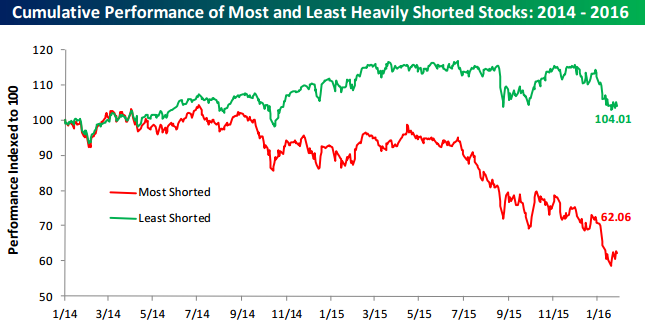

During bull markets one of the best places to look for new long ideas is the list of stocks with highest short interest. However, during bear market cycles heavily shorted stocks tend to underperform and sometimes by a wide margin – case in point, the gap in performance between the most and least heavily shorted stocks since May 2014:

Via Bespoke

A 42% gap in performance since the beginning of 2014 between the most and least heavily shorted stocks in the S&P 1500.

Short sellers are usually very smart and generate intelligent bearish cases on stocks that typically have poor earnings quality, high debt loads, or unsustainable business models. The problem is that the long term trend of the market is very much against selling stocks short.

In addition, another challenge of short selling is one of timing; A short thesis can be completely correct but still lose money in practice because the timing of the position isn’t right. The trading floor is littered with carcasses of short sellers who bet too much and/or bet too early that a stock had rallied too far, too fast. As John Maynard Keynes once famously said “The market can stay irrational longer than you can remain solvent.”

The fact that the most heavily shorted stocks in the market continue to perform so poorly adds credence to the view that we are in the midst of a bear market cycle in U.S. equities. Shrewd market observers will want to keep an eye on the most heavily shorted market sectors (energy:12% short interest and retail:11.44% short interest) for clues as to whether we are experiencing a normal market correction or a much deeper bear market cycle; those with a keen eye will notice that after a big drop to begin the year the most heavily shorted stocks have bounced more aggressively than the rest of the market.